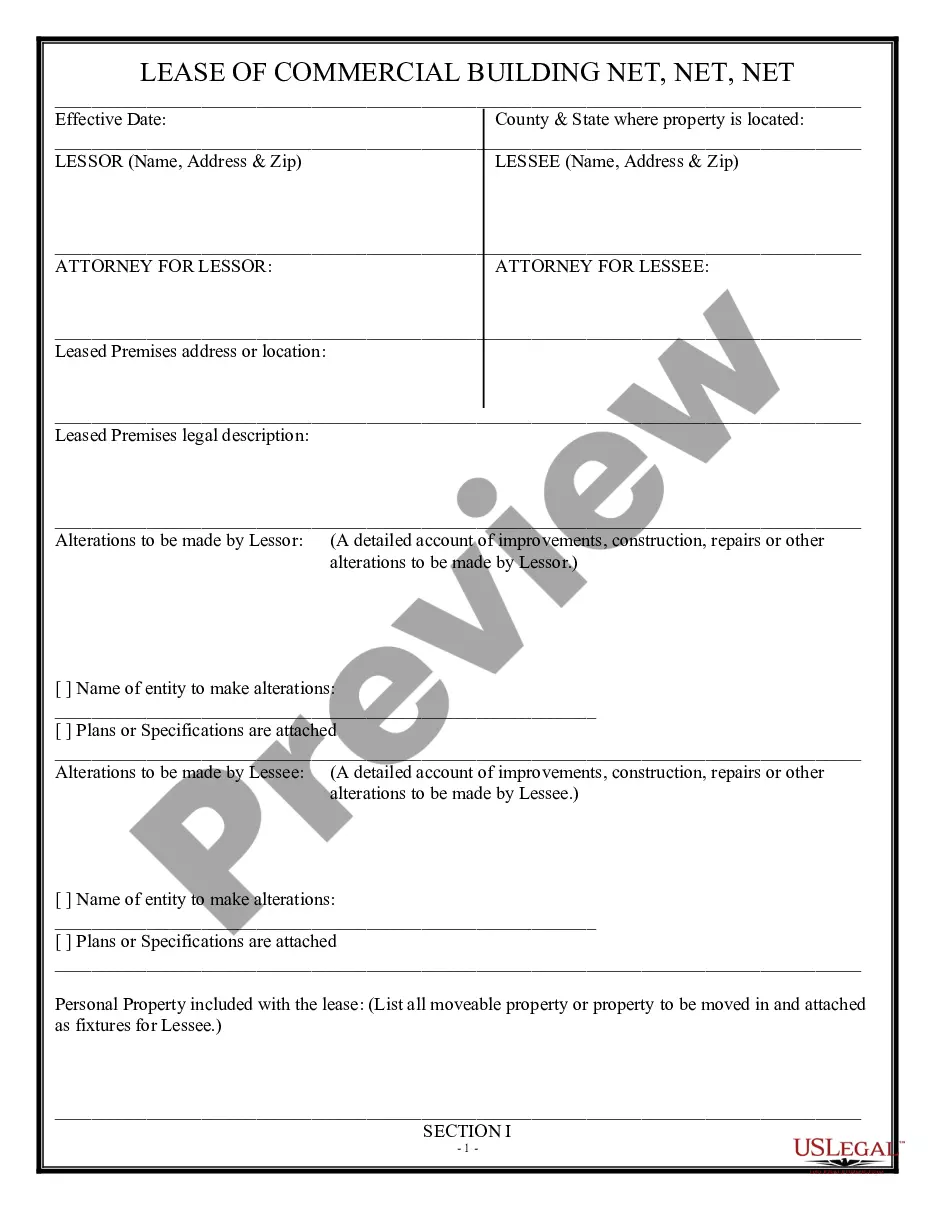

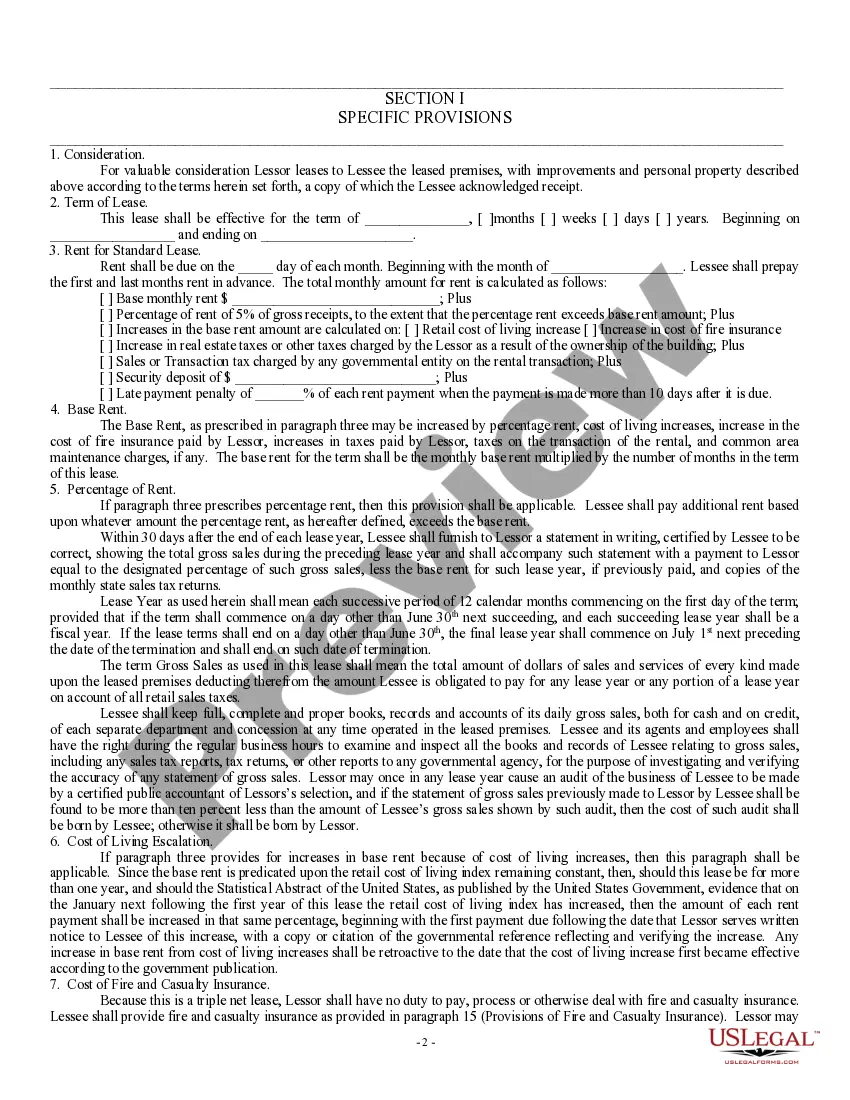

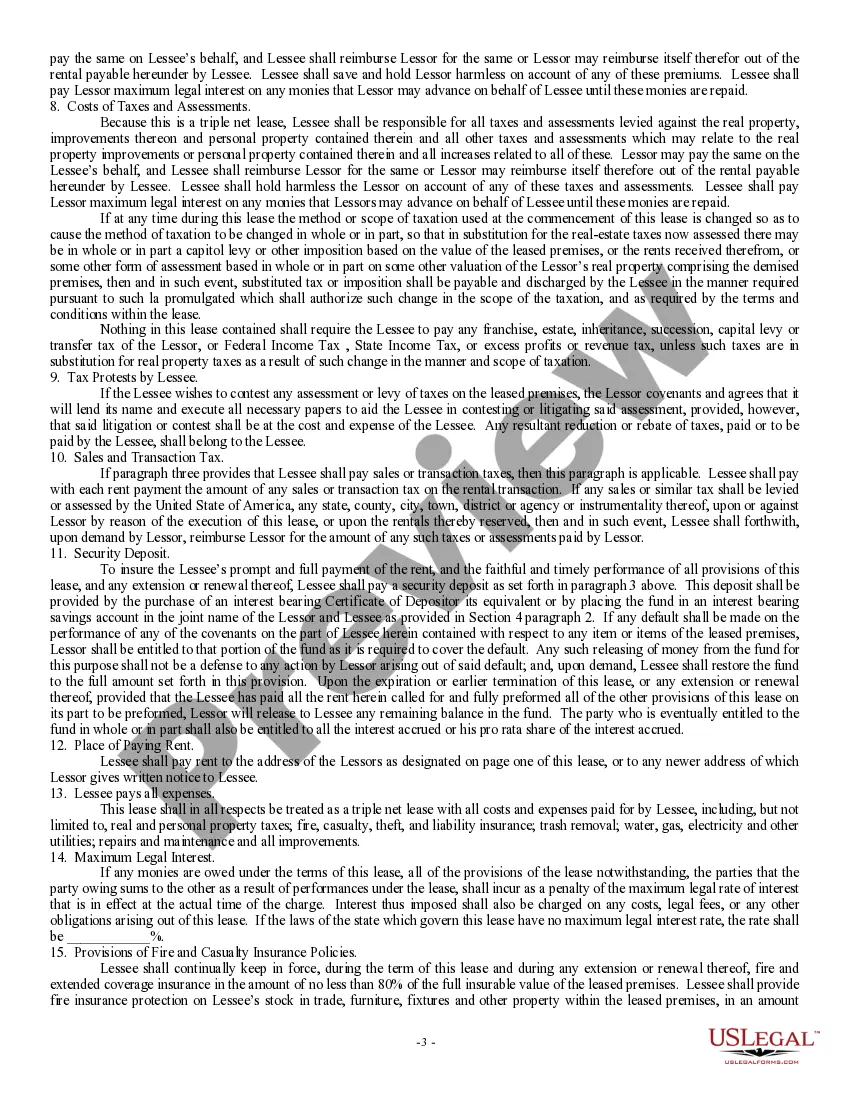

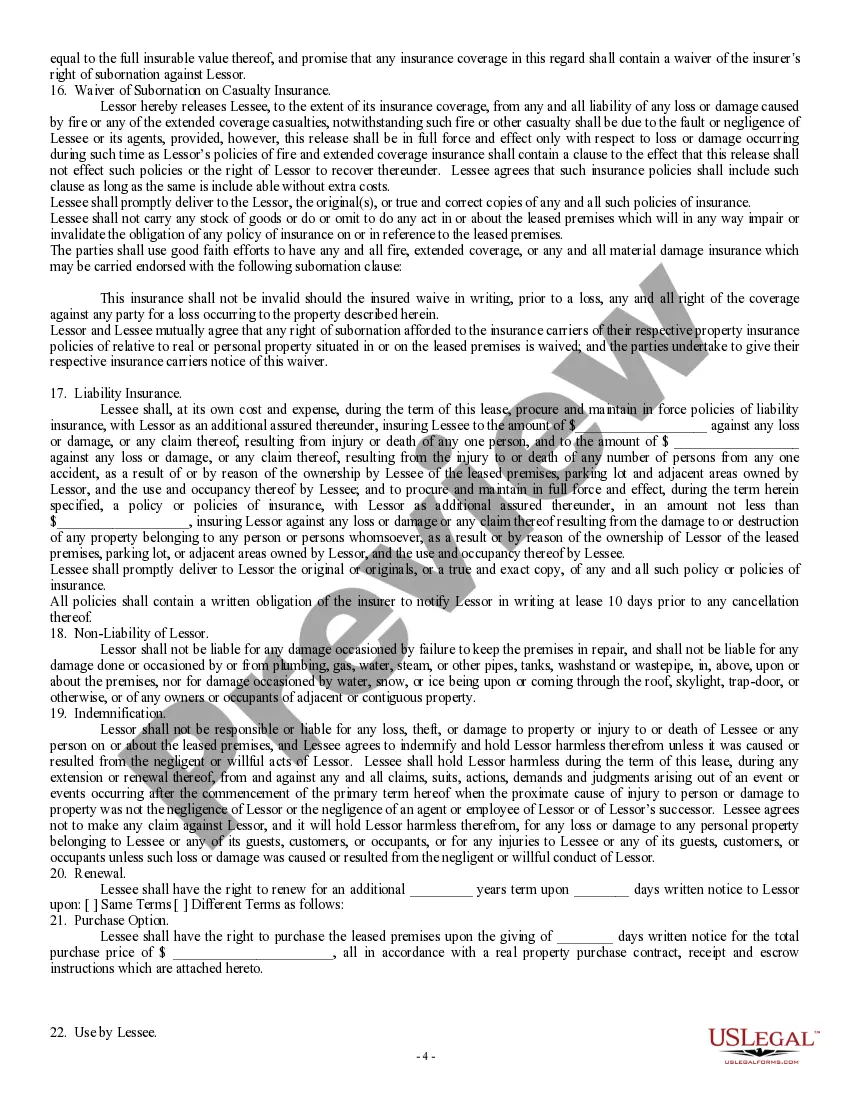

Orange California Triple Net Lease for Industrial Property is a type of lease agreement commonly used in the commercial real estate industry. It specifically refers to a lease arrangement where the tenant is responsible for paying all additional expenses related to the property, including property taxes, insurance, and maintenance costs, in addition to the base rent. In an Orange California Triple Net Lease for Industrial Property, the tenant agrees to bear the financial burden of various property-related expenses, ensuring the property owner, also known as the landlord, is relieved of these obligations. Typically, these leases are long-term agreements, spanning periods of five to twenty years, with occasional options for renewal. This type of lease is highly favored by both tenants and landlords due to the clear allocation of financial responsibilities. For tenants, it provides an additional layer of control over their own space and enables them to manage costs efficiently. On the other hand, property owners benefit from a steady rental income stream without having to worry about the maintenance, insurance, or tax expenses associated with the property. Different types of Orange California Triple Net Lease for Industrial Property may vary in terms of the specific responsibilities assigned to the tenant. While the standard triple net lease requires the tenant to solely bear operational costs, there are variations called double net leases or absolute net leases. In a double net lease, the tenant assumes responsibility for property taxes and insurance, while the landlord retains responsibility for structural maintenance. An absolute net lease goes a step further, requiring the tenant to cover all costs, including structural repairs and improvements. It is crucial for both parties involved in an Orange California Triple Net Lease for Industrial Property to carefully review and negotiate the terms of the lease agreement. The terms should address any potential disputes or gray areas, such as the procedure for managing unexpected repair costs or insurance claims. Additionally, it is essential to consider local regulations and laws pertaining to industrial properties in Orange California before finalizing the lease agreement. In conclusion, Orange California Triple Net Lease for Industrial Property is a lease agreement where the tenant assumes the financial responsibility for property taxes, insurance, and maintenance costs, in addition to the base rent. It provides a clear allocation of financial obligations, benefiting both the tenant and landlord. Different variations of triple net leases include double net leases and absolute net leases, each transferring a different degree of financial responsibility to the tenant. Careful consideration and negotiation of the lease terms are essential for both parties to ensure a smooth and mutually beneficial arrangement.

Orange California Triple Net Lease for Industrial Property

Description

How to fill out Orange California Triple Net Lease For Industrial Property?

If you need to find a reliable legal paperwork supplier to get the Orange Triple Net Lease for Industrial Property, consider US Legal Forms. No matter if you need to launch your LLC business or manage your asset distribution, we got you covered. You don't need to be knowledgeable about in law to locate and download the appropriate form.

- You can search from over 85,000 forms arranged by state/county and situation.

- The self-explanatory interface, number of supporting resources, and dedicated support team make it easy to find and execute various papers.

- US Legal Forms is a trusted service providing legal forms to millions of customers since 1997.

You can simply type to search or browse Orange Triple Net Lease for Industrial Property, either by a keyword or by the state/county the document is intended for. After finding the necessary form, you can log in and download it or save it in the My Forms tab.

Don't have an account? It's easy to get started! Simply find the Orange Triple Net Lease for Industrial Property template and take a look at the form's preview and short introductory information (if available). If you're confident about the template’s legalese, go ahead and hit Buy now. Create an account and choose a subscription option. The template will be immediately available for download as soon as the payment is completed. Now you can execute the form.

Handling your law-related affairs doesn’t have to be pricey or time-consuming. US Legal Forms is here to prove it. Our comprehensive collection of legal forms makes this experience less pricey and more reasonably priced. Set up your first business, organize your advance care planning, create a real estate contract, or complete the Orange Triple Net Lease for Industrial Property - all from the comfort of your sofa.

Join US Legal Forms now!