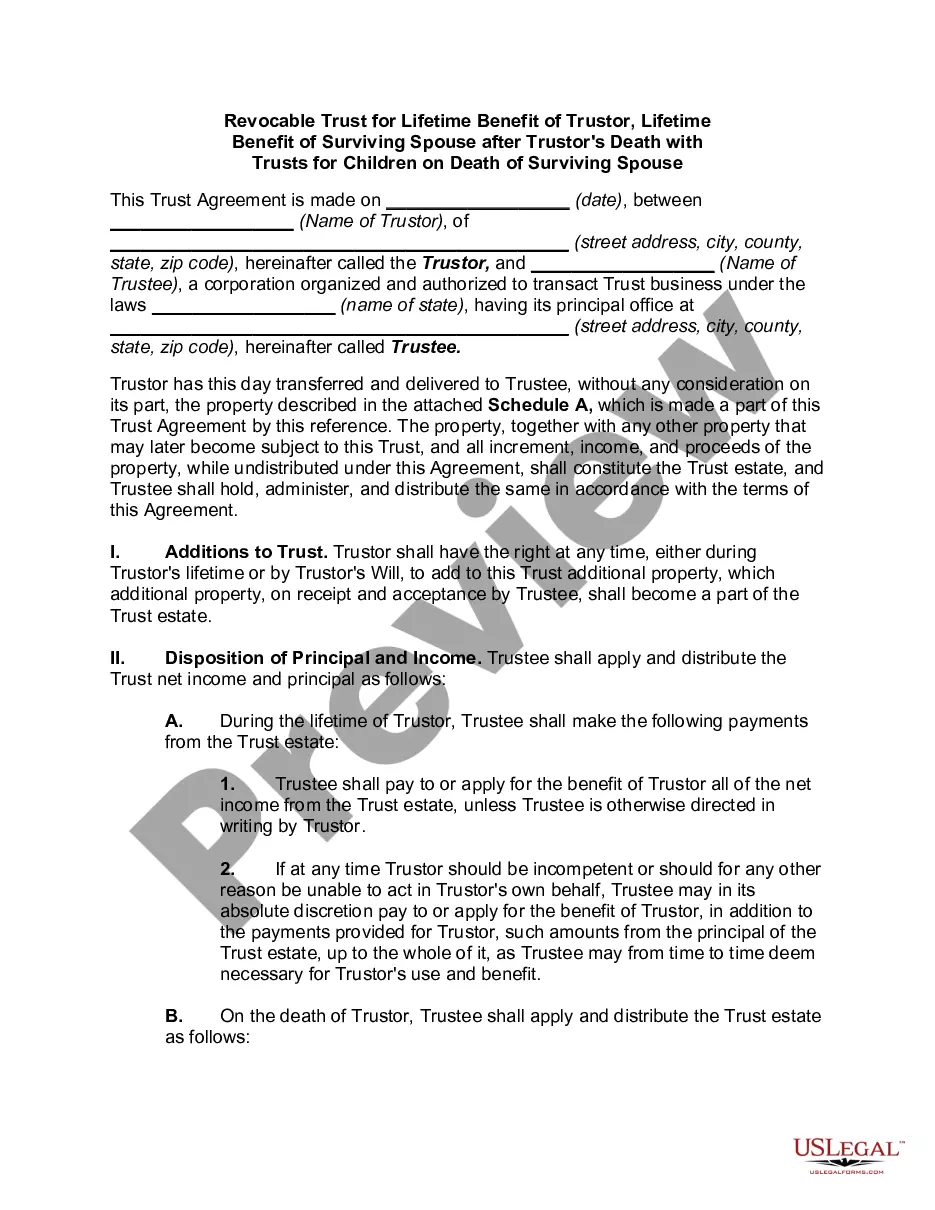

Contra Costa California Revocable Trust for Grandchildren

Description

How to fill out Revocable Trust For Grandchildren?

How long does it usually take you to create a legal document.

Since every state has its own statutes and regulations for various life circumstances, finding a Contra Costa Revocable Trust for Grandchildren that meets all local criteria can be overwhelming, and obtaining it from a licensed attorney is often costly.

Numerous online services provide the most sought-after state-specific templates for download, but utilizing the US Legal Forms library is the most beneficial.

Regardless of how often you need to use the acquired document, you can find all the files you have ever stored in your account by accessing the My documents tab. Give it a try!

- US Legal Forms boasts the largest online collection of templates, categorized by states and purposes of use.

- Alongside the Contra Costa Revocable Trust for Grandchildren, here you can discover any particular form needed to conduct your business or personal transactions, adhering to your local stipulations.

- Professionals verify all templates for their relevance, ensuring you can prepare your documentation accurately.

- Employing the service is quite straightforward.

- If you already possess an account on the platform and your subscription is active, you merely need to Log In, choose the desired template, and download it.

- You can store the file in your account at any point in the future.

- On the other hand, if you're new to the site, there will be a few additional steps to undertake before you acquire your Contra Costa Revocable Trust for Grandchildren.

- Review the details on the page you are visiting.

- Examine the description of the template or Preview it (if available).

- Search for other forms using the related option in the header.

- Press Buy Now once you are confident in the chosen file.

- Choose the subscription plan that fits you best.

- Register for an account on the platform or Log In to continue to payment methods.

- Complete the payment through PayPal or with your credit card.

- Alter the file format if necessary.

- Click Download to save the Contra Costa Revocable Trust for Grandchildren.

- Print the document or utilize any preferred online editor to finalize it electronically.

Form popularity

FAQ

From your house to your financial accounts, there are many assets you'll likely want to include in your living trust: Bank accounts.Real estate property.Insurance policies.Stocks, bonds, and other investment assets.Tangible personal property.Limited liability company (LLCs)Cryptocurrency.

The downside to irrevocable trusts is that you can't change them. And you can't act as your own trustee either. Once the trust is set up and the assets are transferred, you no longer have control over them.

There are a variety of assets that you cannot or should not place in a living trust. These include: Retirement Accounts: Accounts such as a 401(k), IRA, 403(b) and certain qualified annuities should not be transferred into your living trust. Doing so would require a withdrawal and likely trigger income tax.

The only three times you might want to consider creating an irrevocable trust is when you want to (1) minimize estate taxes, (2) become eligible for government programs, or (3) protect your assets from your creditors. If none of these situations applies, you should not have an irrevocable trust.

Once it's set up, you begin by placing your assets?including investments, bank accounts, and real estate?into the trust. At this point you no longer own those assets; they belong to the trust. And because your assets belong to the trust, they do not have to go through the probate process upon your death.

How to Create a Living Trust in the State of California Take an inventory of your assets. Select your trustee. Designate your Beneficiaries. Write up your Declaration of Trust. Sign your Trust in front of a Notary Public (optional). Transfer assets and property to the Trust.

An Irrevocable Trust means you can protect yourself, your loved ones and your estate against future legal action. It also means you can protect the financial future of your estate by avoiding substantial estate taxes.

With an irrevocable trust, the transfer of assets is permanent. So once the trust is created and assets are transferred, they generally can't be taken out again. You can still act as the trustee but you'd be limited to withdrawing money only on an as-needed basis to cover necessary expenses.

From your house to your financial accounts, there are many assets you'll likely want to include in your living trust: Bank accounts.Real estate property.Insurance policies.Stocks, bonds, and other investment assets.Tangible personal property.Limited liability company (LLCs)Cryptocurrency.

The main downside of an irrevocable trust is that once you set it up, you no longer have control over your assets. You can't designate yourself as the trustee to get around this, either. This means that once you set it up, you can't change anything.