A secured transaction is created when a buyer or borrower (debtor) grants a seller or lender (creditor or secured party) a security interest in personal property (collateral). A security interest allows a creditor to repossess and sell the collateral if a debtor fails to pay a secured debt.

The Truth-in-Lending Act (TILA) is part of the Federal Consumer Credit Protection Act. The purpose of the TILA is to make full disclosure to debtors of what they are being charged for the credit they are receiving. The Act merely asks lenders to be honest to the debtors and not cover up what they are paying for the credit. Regulation Z is a federal regulation prepared by the Federal Reserve Board to carry out the details of the Act. TILA applies to consumer credit transactions. Consumer credit is credit for personal or household use and not commercial use or business purposes.

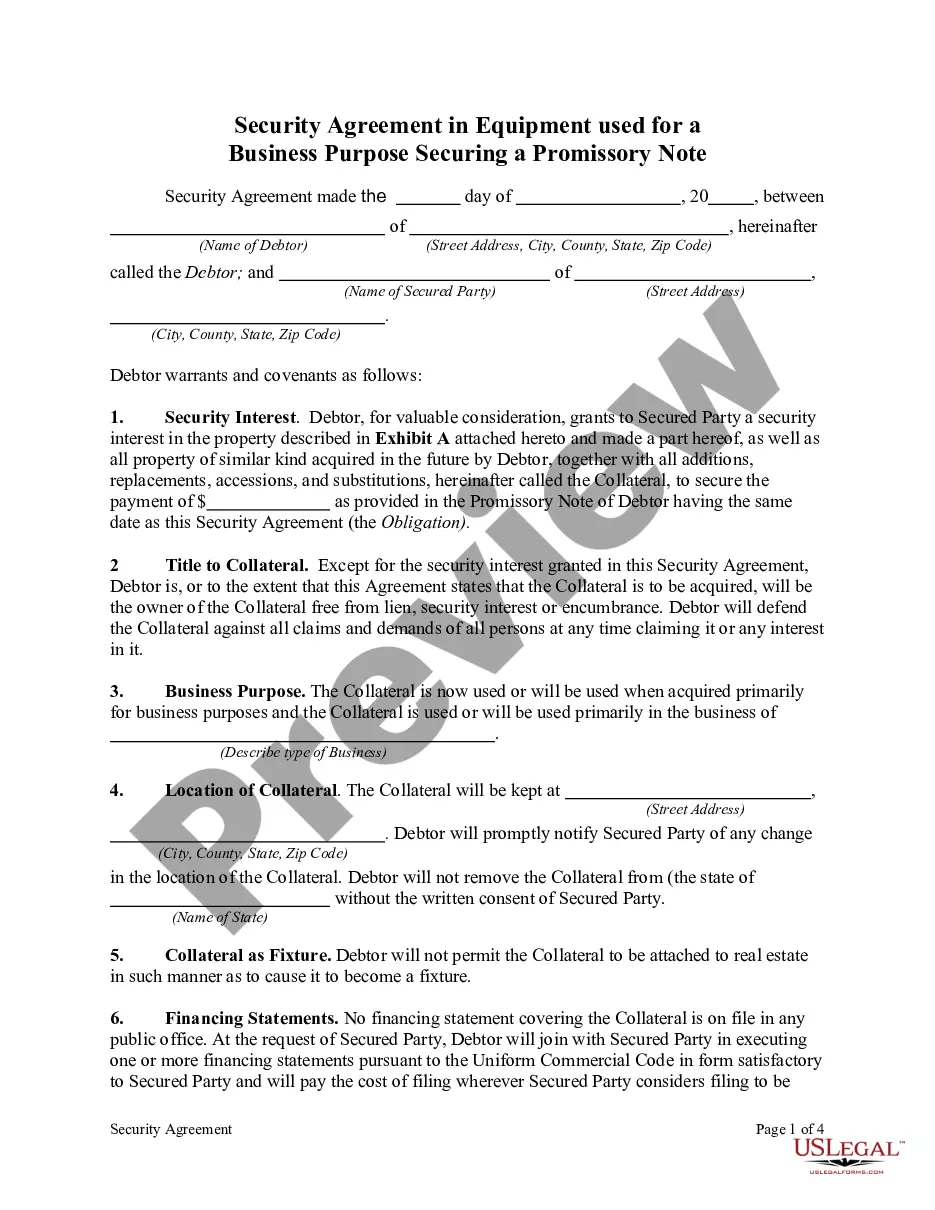

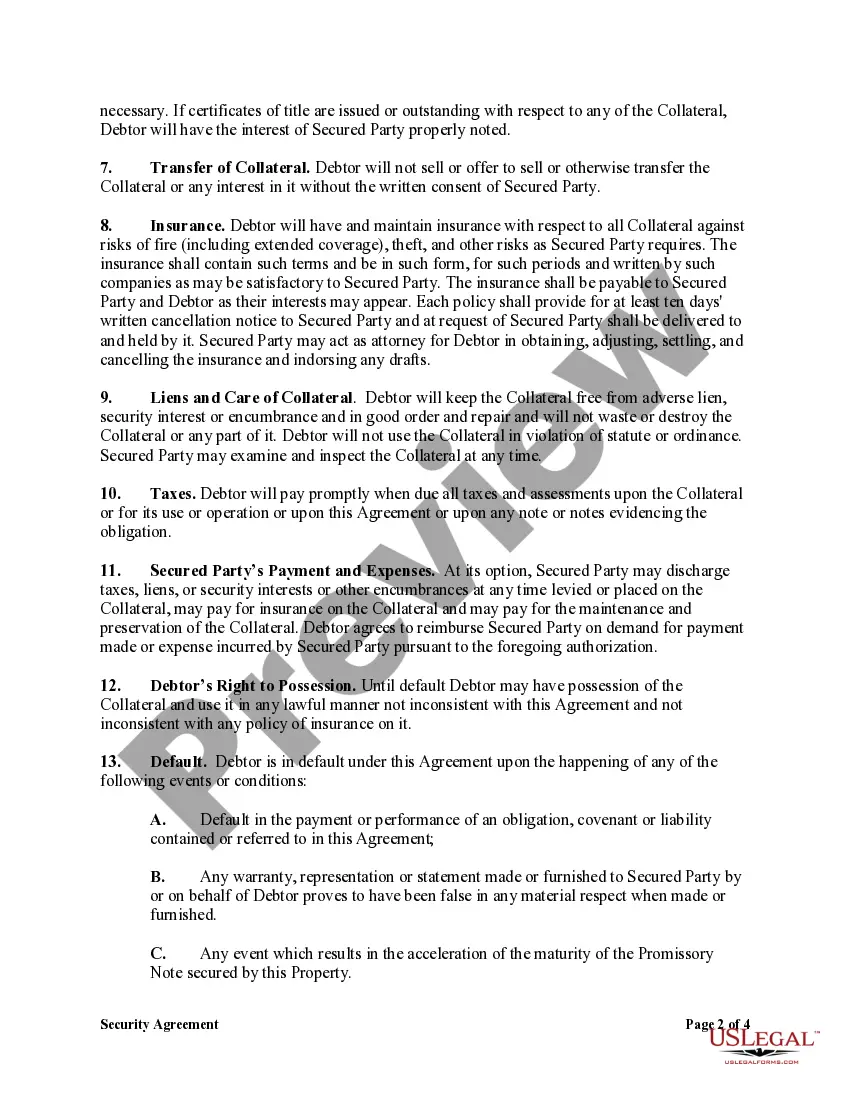

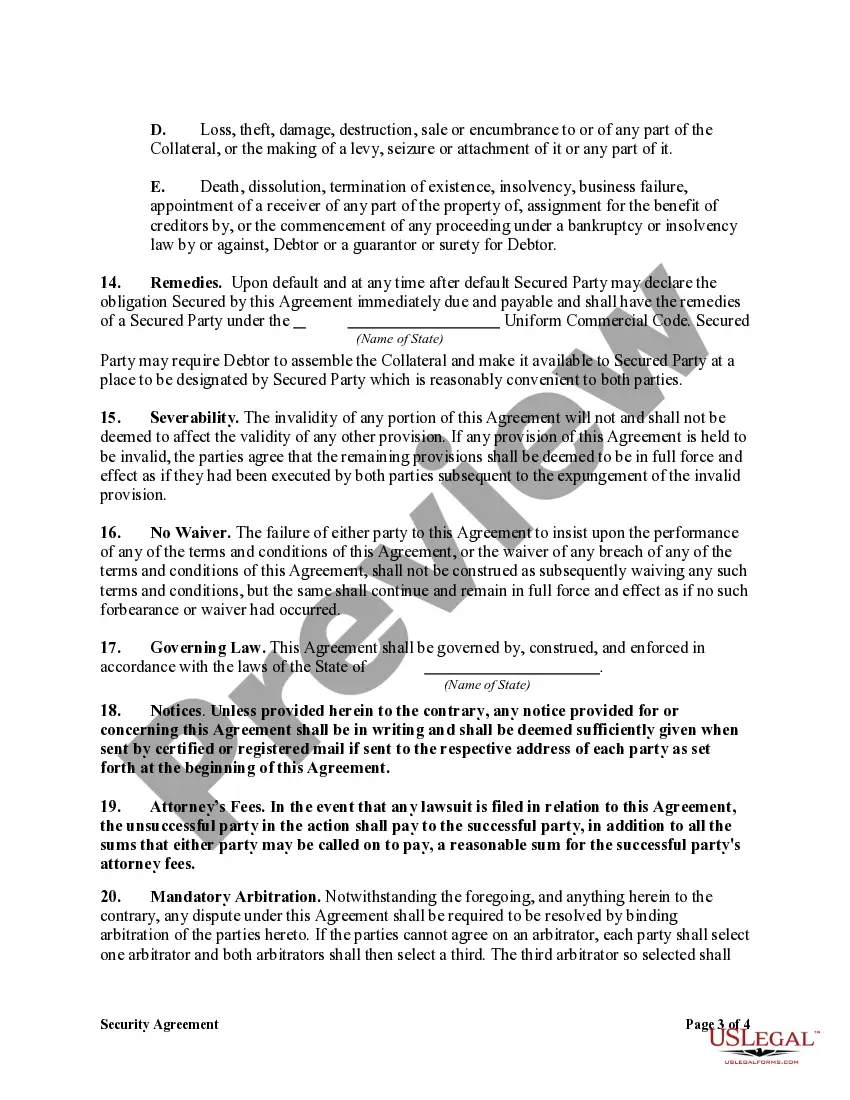

A Clark Nevada Security Agreement in Equipment for Business Purposes is a legal document that helps secure a promissory note for businesses when they borrow money to purchase equipment or assets. This agreement acts as collateral for the lender, giving them a right to the equipment or assets should the borrower default on their loan repayment. It establishes a legal relationship between the lender and borrower, outlining the terms and conditions of the loan and the associated security. The Clark Nevada Security Agreement in Equipment for Business Purposes typically includes details such as the names and addresses of both the lender and the borrower, the date of the agreement, and a description of the equipment or assets being used as collateral. It also specifies the amount of the loan, the interest rate, and the repayment terms, including the due date and installment schedule. The agreement outlines the rights and responsibilities of both parties. It clarifies that the borrower retains ownership of the equipment or assets until the loan is fully repaid, but allows the lender to take possession of and sell the collateral to recover the outstanding amount if necessary. The agreement may also include clauses regarding insurance requirements, maintenance of the equipment, and potential penalties for default or breach of the agreement. In Clark Nevada, there may be variations of the Security Agreement in Equipment for Business Purposes. Some of these variations may include: 1. Installment Security Agreement: This type of agreement allows the borrower to repay the loan in installments over a specified period. It provides a structured repayment plan, detailing the number of installments, amount due, and due dates. 2. Balloon Security Agreement: Unlike an installment agreement, a balloon agreement allows the borrower to make smaller periodic payments throughout the loan term, with a larger final payment known as a "balloon payment" at the end. This structure helps businesses with cash flow by providing flexibility in repayment options. 3. Cross-Collateralization Security Agreement: This agreement involves using multiple pieces of equipment or assets to secure the loan. If the borrower defaults, the lender has the right to seize any of the collateral to recover the outstanding amount. 4. Subordination Agreement: In some cases, when a business already has existing loans or liens on its equipment, a subordination agreement may be necessary. This agreement allows the lender to obtain a secondary or subordinate position in terms of repayment priority, ensuring that the new lender is protected even though there are existing creditors. It is important to consult with a legal professional to ensure the Security Agreement in Equipment for Business Purposes adheres to the specific regulations and requirements of Clark Nevada and meets the needs of both the borrower and the lender.A Clark Nevada Security Agreement in Equipment for Business Purposes is a legal document that helps secure a promissory note for businesses when they borrow money to purchase equipment or assets. This agreement acts as collateral for the lender, giving them a right to the equipment or assets should the borrower default on their loan repayment. It establishes a legal relationship between the lender and borrower, outlining the terms and conditions of the loan and the associated security. The Clark Nevada Security Agreement in Equipment for Business Purposes typically includes details such as the names and addresses of both the lender and the borrower, the date of the agreement, and a description of the equipment or assets being used as collateral. It also specifies the amount of the loan, the interest rate, and the repayment terms, including the due date and installment schedule. The agreement outlines the rights and responsibilities of both parties. It clarifies that the borrower retains ownership of the equipment or assets until the loan is fully repaid, but allows the lender to take possession of and sell the collateral to recover the outstanding amount if necessary. The agreement may also include clauses regarding insurance requirements, maintenance of the equipment, and potential penalties for default or breach of the agreement. In Clark Nevada, there may be variations of the Security Agreement in Equipment for Business Purposes. Some of these variations may include: 1. Installment Security Agreement: This type of agreement allows the borrower to repay the loan in installments over a specified period. It provides a structured repayment plan, detailing the number of installments, amount due, and due dates. 2. Balloon Security Agreement: Unlike an installment agreement, a balloon agreement allows the borrower to make smaller periodic payments throughout the loan term, with a larger final payment known as a "balloon payment" at the end. This structure helps businesses with cash flow by providing flexibility in repayment options. 3. Cross-Collateralization Security Agreement: This agreement involves using multiple pieces of equipment or assets to secure the loan. If the borrower defaults, the lender has the right to seize any of the collateral to recover the outstanding amount. 4. Subordination Agreement: In some cases, when a business already has existing loans or liens on its equipment, a subordination agreement may be necessary. This agreement allows the lender to obtain a secondary or subordinate position in terms of repayment priority, ensuring that the new lender is protected even though there are existing creditors. It is important to consult with a legal professional to ensure the Security Agreement in Equipment for Business Purposes adheres to the specific regulations and requirements of Clark Nevada and meets the needs of both the borrower and the lender.