A secured transaction is created when a buyer or borrower (debtor) grants a seller or lender (creditor or secured party) a security interest in personal property (collateral). A security interest allows a creditor to repossess and sell the collateral if a debtor fails to pay a secured debt.

The Truth-in-Lending Act (TILA) is part of the Federal Consumer Credit Protection Act. The purpose of the TILA is to make full disclosure to debtors of what they are being charged for the credit they are receiving. The Act merely asks lenders to be honest to the debtors and not cover up what they are paying for the credit. Regulation Z is a federal regulation prepared by the Federal Reserve Board to carry out the details of the Act. TILA applies to consumer credit transactions. Consumer credit is credit for personal or household use and not commercial use or business purposes.

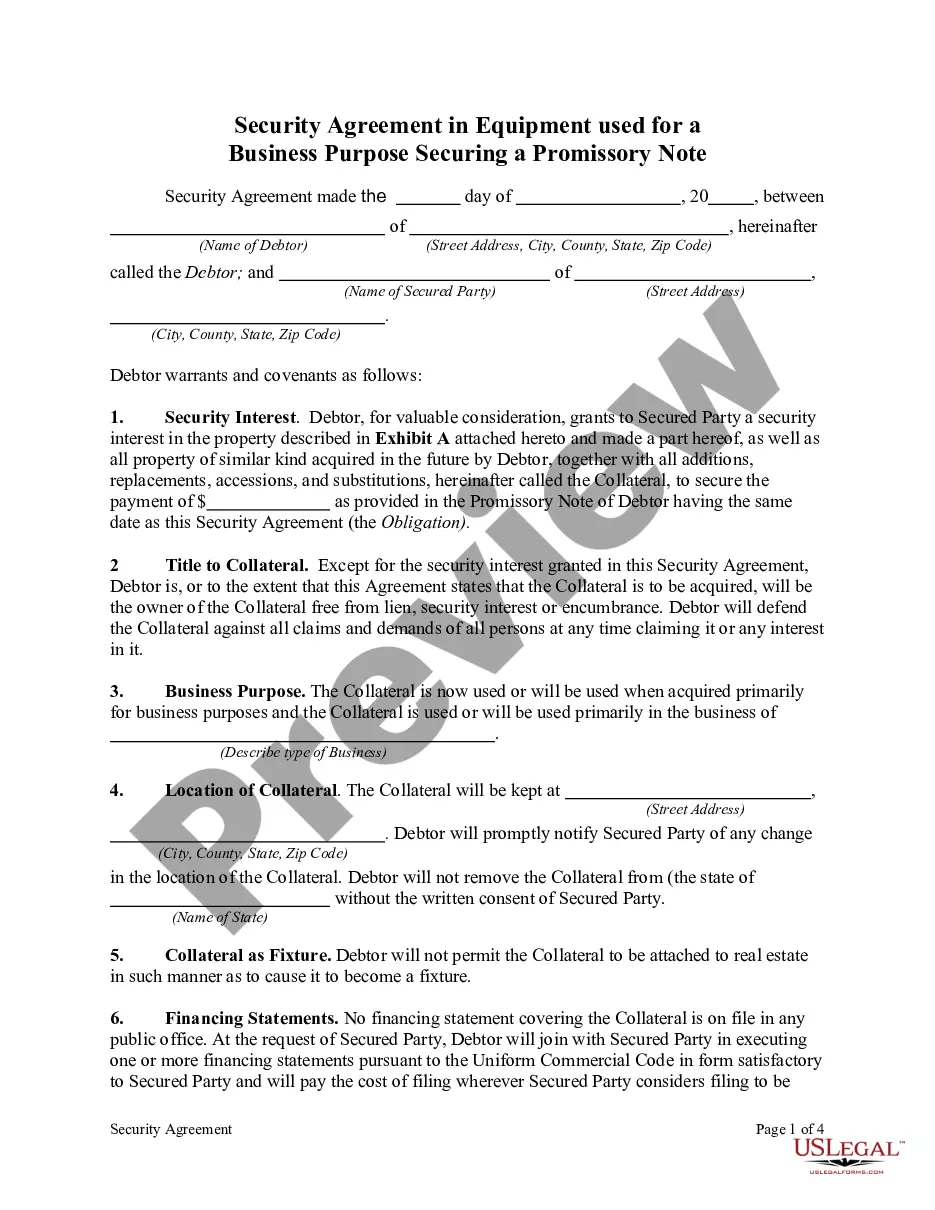

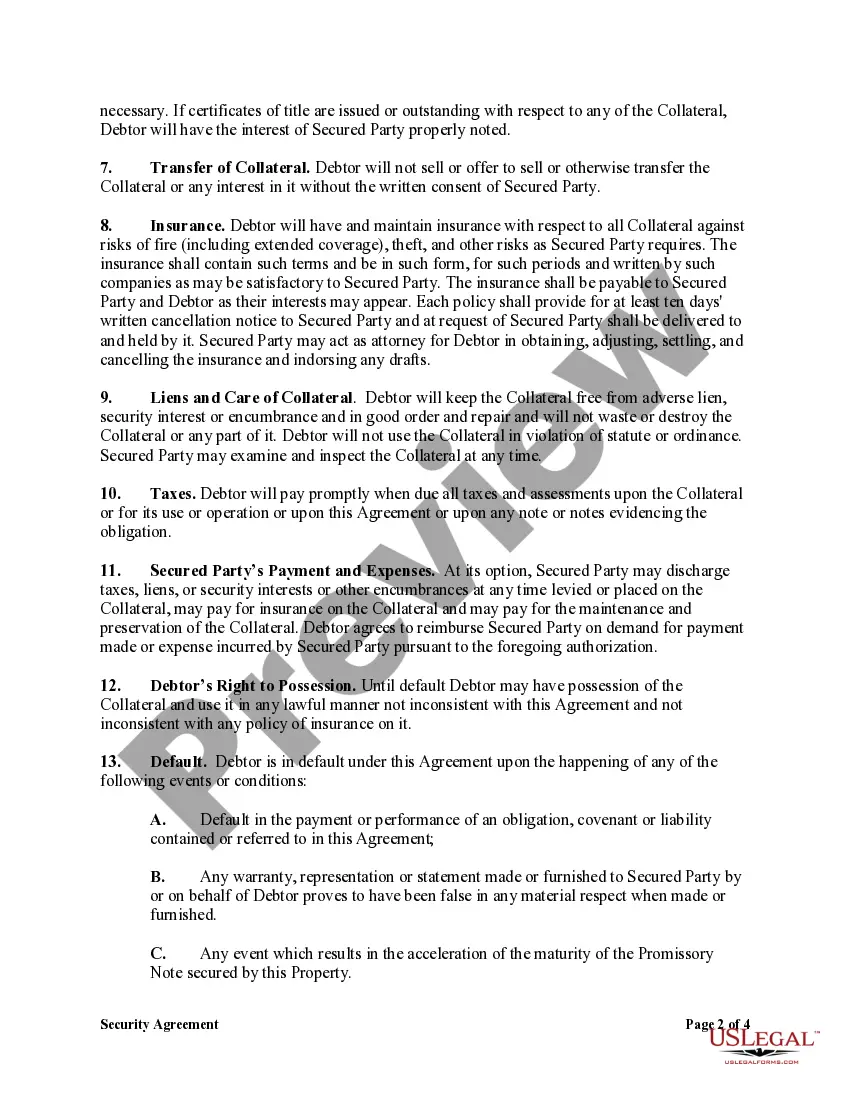

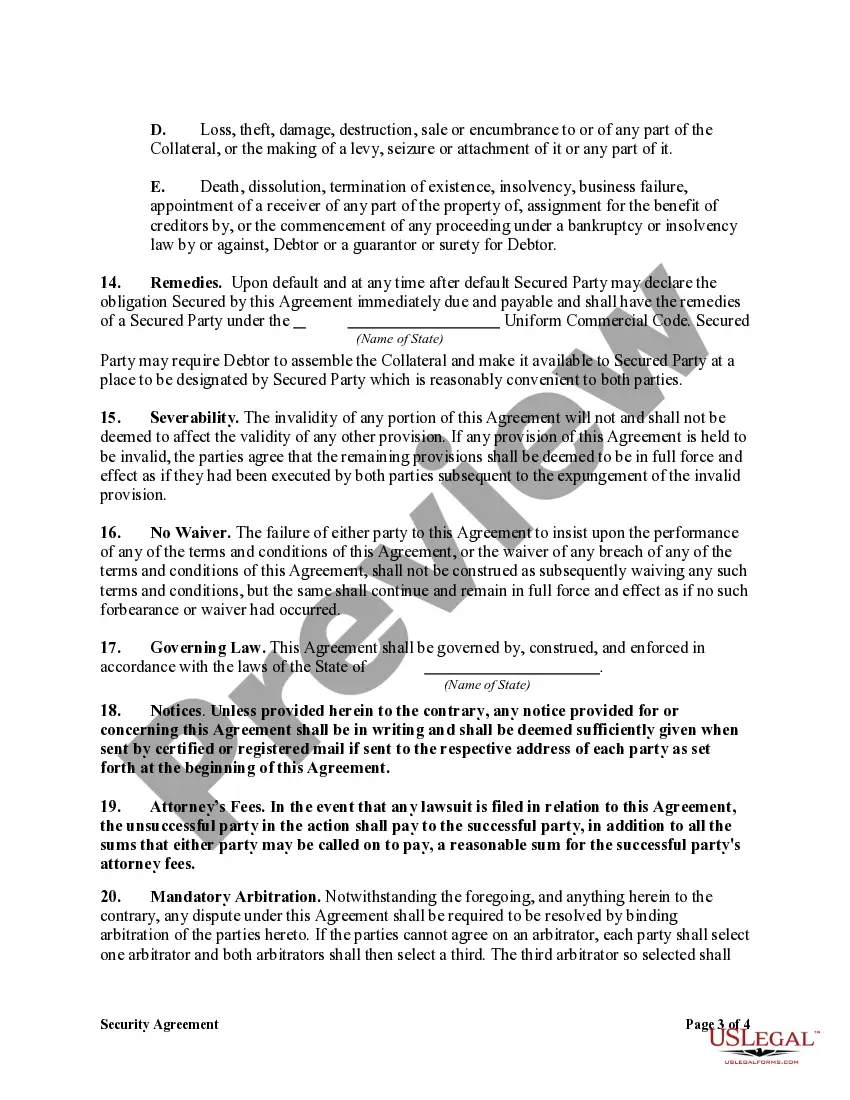

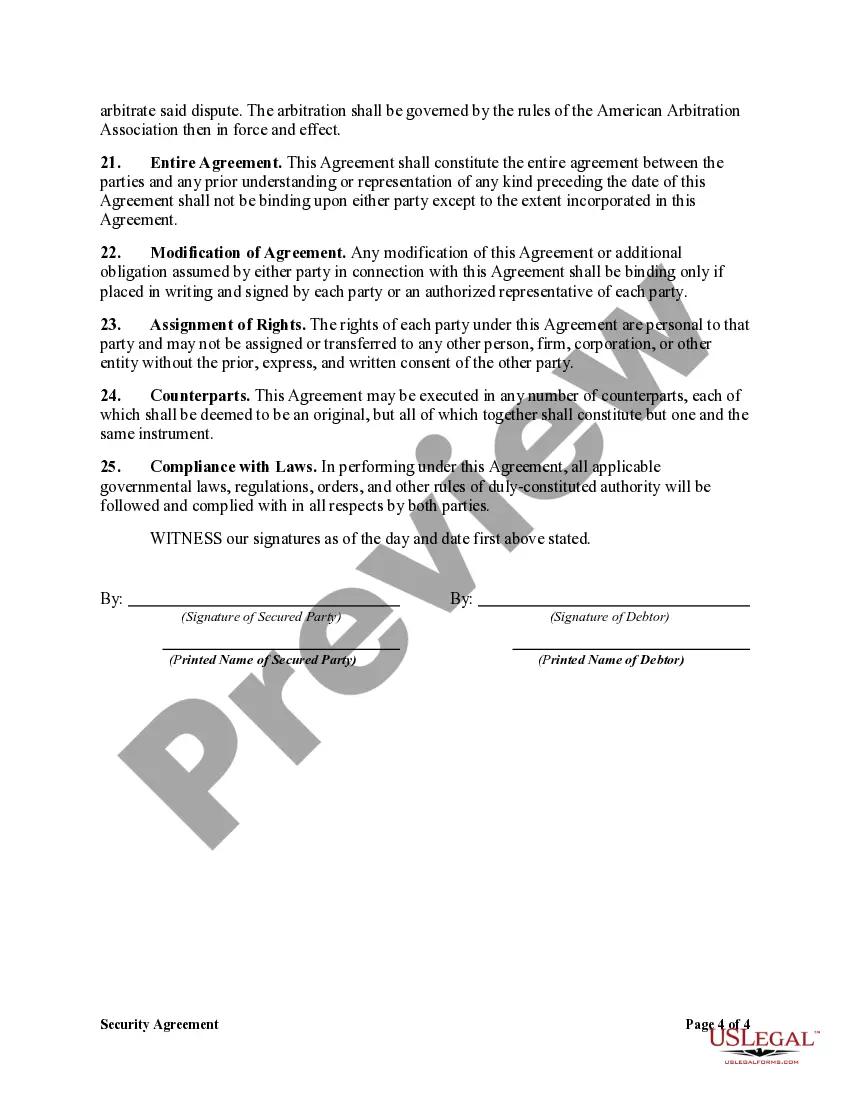

The Cook Illinois Security Agreement in Equipment for Business Purposes — Securing Promissory Note is a legal document that outlines the terms and conditions related to securing a promissory note with specific equipment for business purposes. This agreement serves as a protection mechanism for lenders, ensuring that they have a legal claim on the equipment in case the borrower defaults on the promissory note. The agreement typically includes detailed information about the parties involved, such as the borrower and the lender, and specifies the equipment that will be used as collateral. It outlines the rights and responsibilities of both parties regarding the use, maintenance, and insurance of the secured equipment. Different types of Cook Illinois Security Agreement in Equipment for Business Purposes — Securing Promissory Note may include: 1. Equipment Financing Security Agreement: This type of agreement is used when a borrower seeks financing to acquire specific equipment for their business. The lender will require the borrower to sign a security agreement, which grants them a security interest in the equipment until the promissory note is fully repaid. 2. Secured Promissory Note with Equipment Collateral: In this type of agreement, the borrower pledges specific equipment as collateral to secure a promissory note. If the borrower fails to make the required payments on time, the lender can legally seize and sell the equipment to recover their losses. 3. Installment Purchase Agreement with Equipment Security: This agreement is commonly used in cases where a borrower wants to purchase equipment from a seller but cannot afford to make the full payment upfront. The borrower signs a promissory note and a security agreement, allowing the seller to retain a security interest in the equipment until the full purchase price is paid. The Cook Illinois Security Agreement in Equipment for Business Purposes — Securing Promissory Note is crucial for both borrowers and lenders as it provides a legal framework to protect the interests of all parties involved. By clearly defining the agreement terms and conditions, it helps minimize the risk of default and ensures that the equipment is used for its intended purpose during the repayment period.The Cook Illinois Security Agreement in Equipment for Business Purposes — Securing Promissory Note is a legal document that outlines the terms and conditions related to securing a promissory note with specific equipment for business purposes. This agreement serves as a protection mechanism for lenders, ensuring that they have a legal claim on the equipment in case the borrower defaults on the promissory note. The agreement typically includes detailed information about the parties involved, such as the borrower and the lender, and specifies the equipment that will be used as collateral. It outlines the rights and responsibilities of both parties regarding the use, maintenance, and insurance of the secured equipment. Different types of Cook Illinois Security Agreement in Equipment for Business Purposes — Securing Promissory Note may include: 1. Equipment Financing Security Agreement: This type of agreement is used when a borrower seeks financing to acquire specific equipment for their business. The lender will require the borrower to sign a security agreement, which grants them a security interest in the equipment until the promissory note is fully repaid. 2. Secured Promissory Note with Equipment Collateral: In this type of agreement, the borrower pledges specific equipment as collateral to secure a promissory note. If the borrower fails to make the required payments on time, the lender can legally seize and sell the equipment to recover their losses. 3. Installment Purchase Agreement with Equipment Security: This agreement is commonly used in cases where a borrower wants to purchase equipment from a seller but cannot afford to make the full payment upfront. The borrower signs a promissory note and a security agreement, allowing the seller to retain a security interest in the equipment until the full purchase price is paid. The Cook Illinois Security Agreement in Equipment for Business Purposes — Securing Promissory Note is crucial for both borrowers and lenders as it provides a legal framework to protect the interests of all parties involved. By clearly defining the agreement terms and conditions, it helps minimize the risk of default and ensures that the equipment is used for its intended purpose during the repayment period.