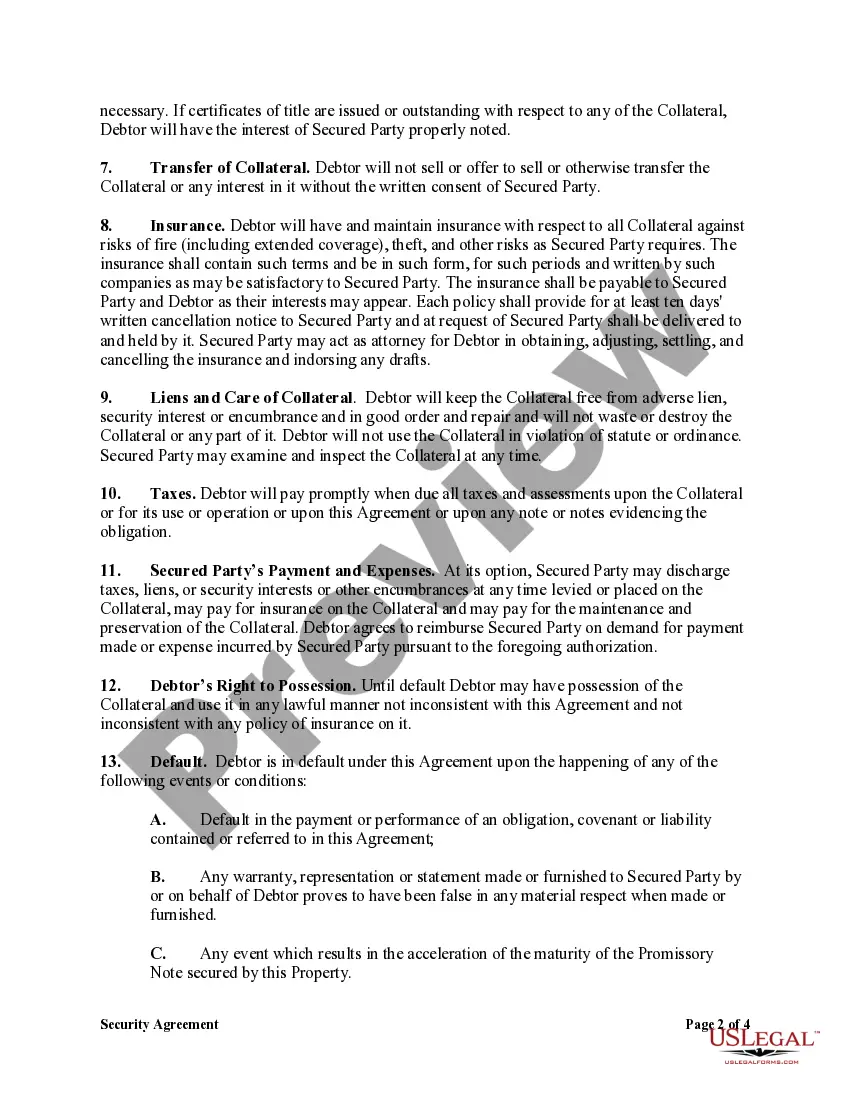

A secured transaction is created when a buyer or borrower (debtor) grants a seller or lender (creditor or secured party) a security interest in personal property (collateral). A security interest allows a creditor to repossess and sell the collateral if a debtor fails to pay a secured debt.

The Truth-in-Lending Act (TILA) is part of the Federal Consumer Credit Protection Act. The purpose of the TILA is to make full disclosure to debtors of what they are being charged for the credit they are receiving. The Act merely asks lenders to be honest to the debtors and not cover up what they are paying for the credit. Regulation Z is a federal regulation prepared by the Federal Reserve Board to carry out the details of the Act. TILA applies to consumer credit transactions. Consumer credit is credit for personal or household use and not commercial use or business purposes.

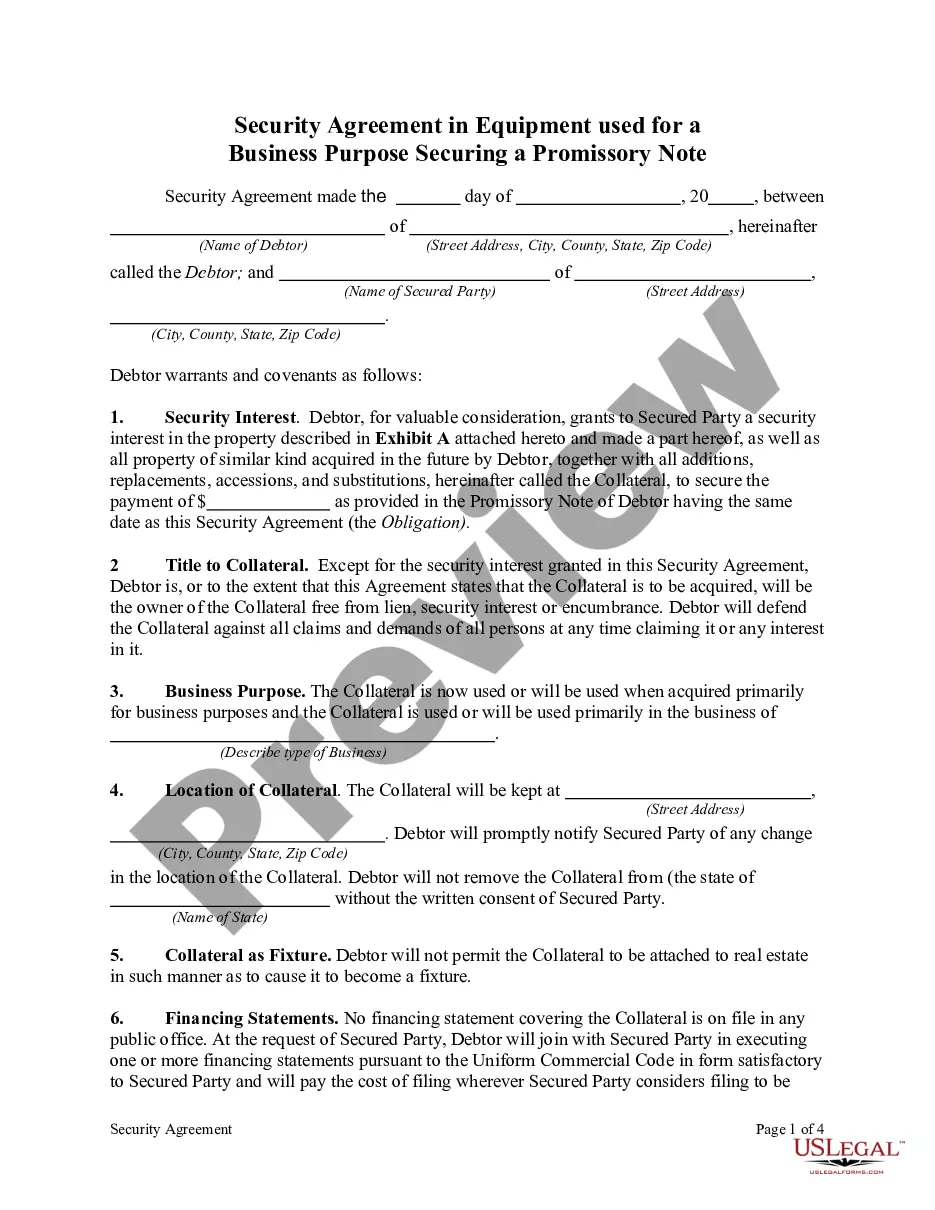

Orange California Security Agreement in Equipment for Business Purposes — Securing Promissory Note is a legal document used in Orange County, California, to provide security when lending equipment to a business for a specified period in exchange for a promissory note. This agreement ensures that the lender has a right to reclaim the equipment if the borrower defaults on the repayment terms. Keywords: Orange California, Security Agreement, Equipment, Business Purposes, Promissory Note, Legal document, Orange County, Lending, Borrower, Repayment terms. There are multiple types of Orange California Security Agreements in Equipment for Business Purposes — Securing Promissory Note, including: 1. Basic Security Agreement: This type of agreement outlines the terms and conditions of lending equipment, securing the promissory note, and clarifying the rights and obligations of both parties involved. 2. Specific Equipment Security Agreement: This agreement focuses on a specific piece or type of equipment being lent to the borrower, such as machinery, vehicles, or technology. It outlines the equipment's details, value, and condition. 3. Financial Security Agreement: This type of agreement includes additional clauses related to financial aspects, such as interest rates, payment schedules, and penalties for late payments or defaults. It ensures proper financial accountability and safeguarding of the lender's investment. 4. Conditional Sale Security Agreement: This agreement allows the lender to retain ownership rights over the equipment until the borrower entirely fulfills the promissory note's repayment obligations. It grants the lender the ability to repossess the equipment if necessary. 5. Chattel Mortgage Security Agreement: Chattel mortgages are commonly used when a business borrows equipment for a specific period but wants to retain ownership rights over the equipment. This agreement establishes a lien on the equipment, securing the promissory note. 6. Lease Agreement with Security Provisions: In some cases, a business might prefer to lease equipment instead of purchasing it outright. This type of agreement combines the terms of a lease agreement with the security provisions of a security agreement, ensuring repayment and restoration of the equipment upon termination. Overall, an Orange California Security Agreement in Equipment for Business Purposes — Securing Promissory Note helps protect both the lender and borrower's interests by clearly defining the terms and conditions of the equipment loan and ensuring the return or value compensation in case of non-compliance.Orange California Security Agreement in Equipment for Business Purposes — Securing Promissory Note is a legal document used in Orange County, California, to provide security when lending equipment to a business for a specified period in exchange for a promissory note. This agreement ensures that the lender has a right to reclaim the equipment if the borrower defaults on the repayment terms. Keywords: Orange California, Security Agreement, Equipment, Business Purposes, Promissory Note, Legal document, Orange County, Lending, Borrower, Repayment terms. There are multiple types of Orange California Security Agreements in Equipment for Business Purposes — Securing Promissory Note, including: 1. Basic Security Agreement: This type of agreement outlines the terms and conditions of lending equipment, securing the promissory note, and clarifying the rights and obligations of both parties involved. 2. Specific Equipment Security Agreement: This agreement focuses on a specific piece or type of equipment being lent to the borrower, such as machinery, vehicles, or technology. It outlines the equipment's details, value, and condition. 3. Financial Security Agreement: This type of agreement includes additional clauses related to financial aspects, such as interest rates, payment schedules, and penalties for late payments or defaults. It ensures proper financial accountability and safeguarding of the lender's investment. 4. Conditional Sale Security Agreement: This agreement allows the lender to retain ownership rights over the equipment until the borrower entirely fulfills the promissory note's repayment obligations. It grants the lender the ability to repossess the equipment if necessary. 5. Chattel Mortgage Security Agreement: Chattel mortgages are commonly used when a business borrows equipment for a specific period but wants to retain ownership rights over the equipment. This agreement establishes a lien on the equipment, securing the promissory note. 6. Lease Agreement with Security Provisions: In some cases, a business might prefer to lease equipment instead of purchasing it outright. This type of agreement combines the terms of a lease agreement with the security provisions of a security agreement, ensuring repayment and restoration of the equipment upon termination. Overall, an Orange California Security Agreement in Equipment for Business Purposes — Securing Promissory Note helps protect both the lender and borrower's interests by clearly defining the terms and conditions of the equipment loan and ensuring the return or value compensation in case of non-compliance.