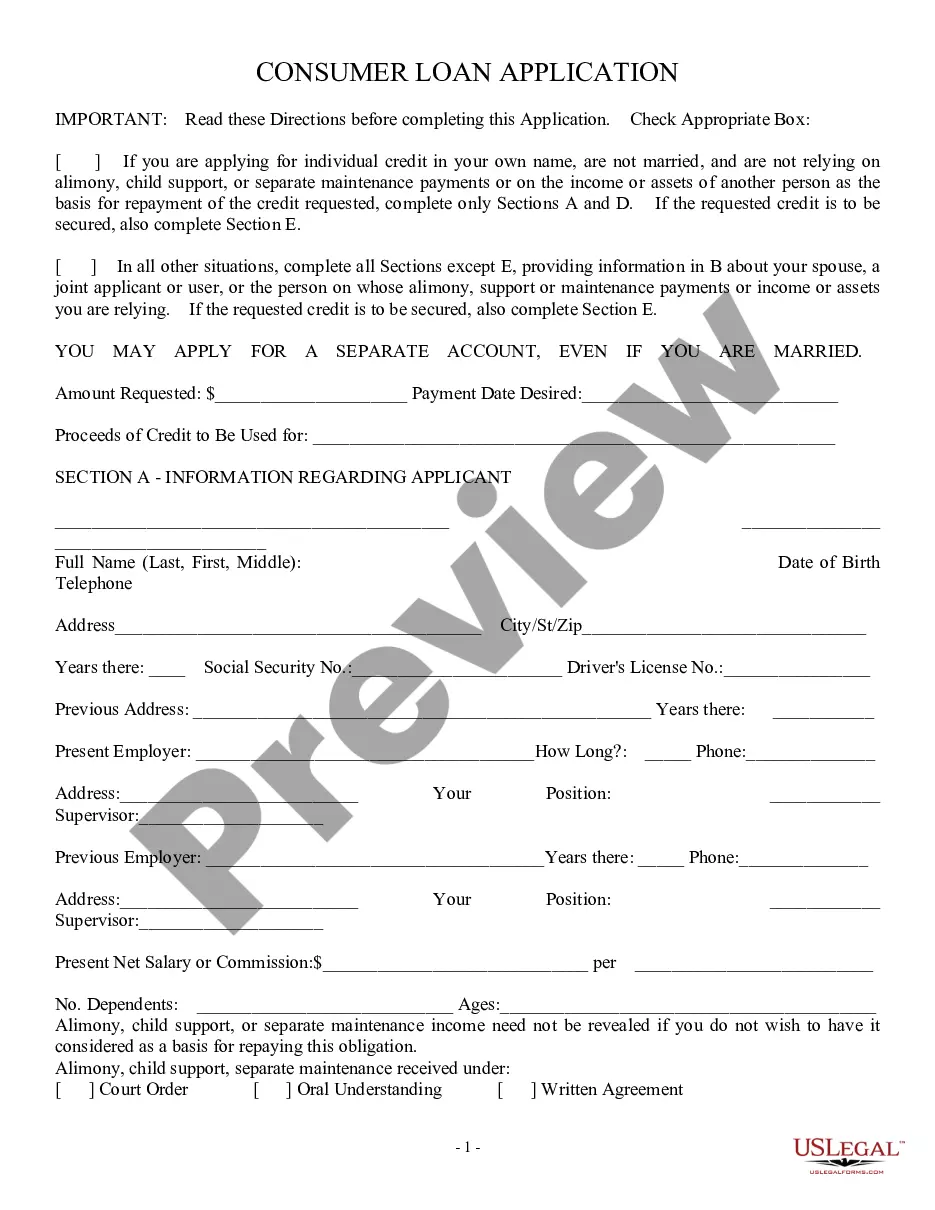

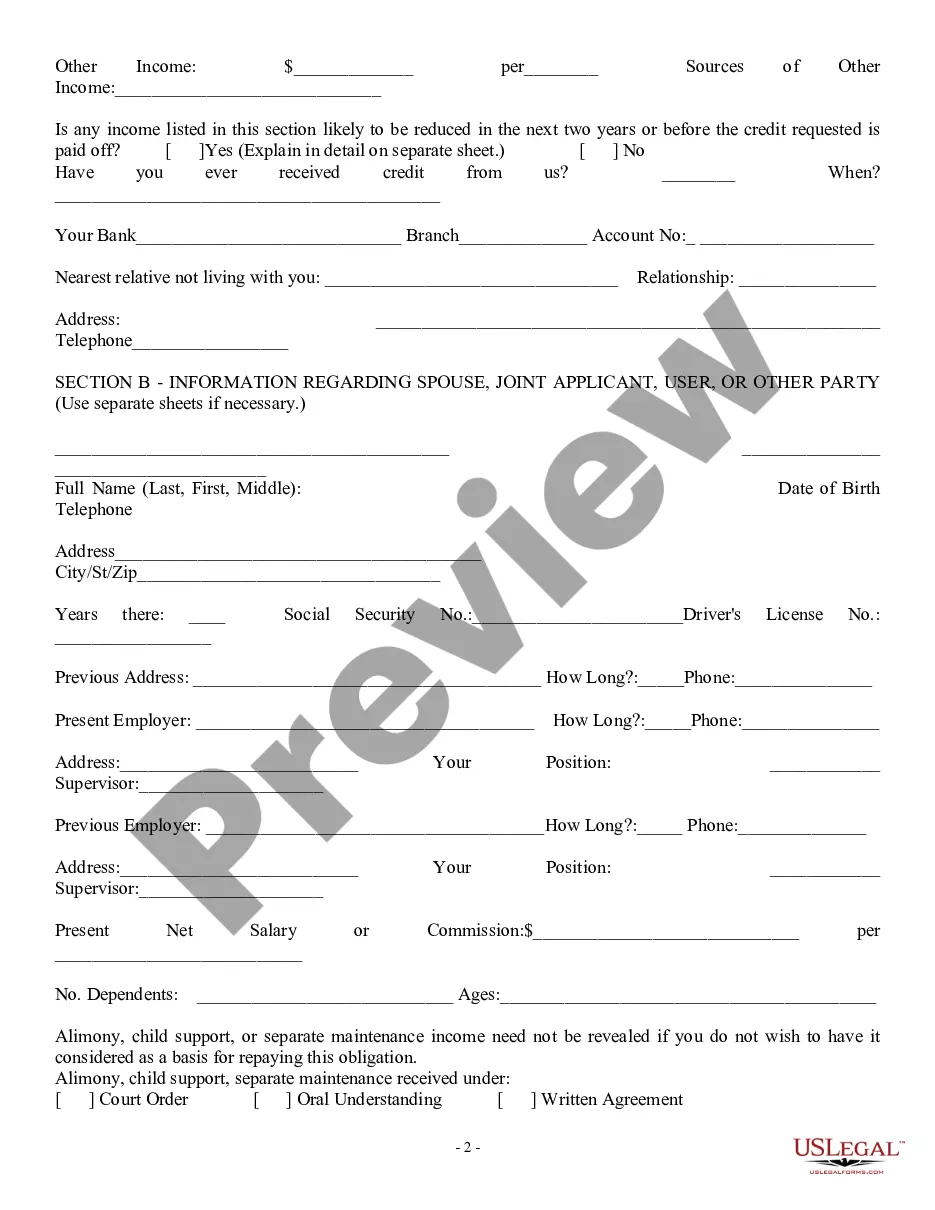

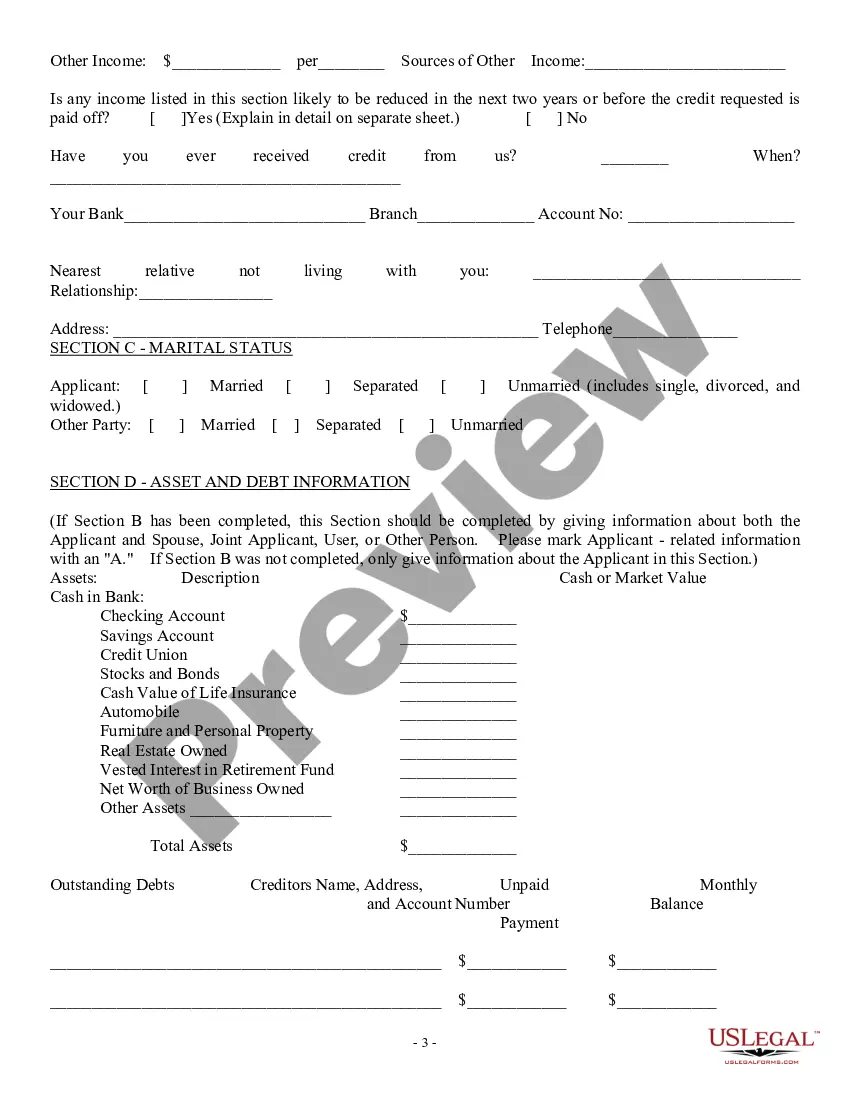

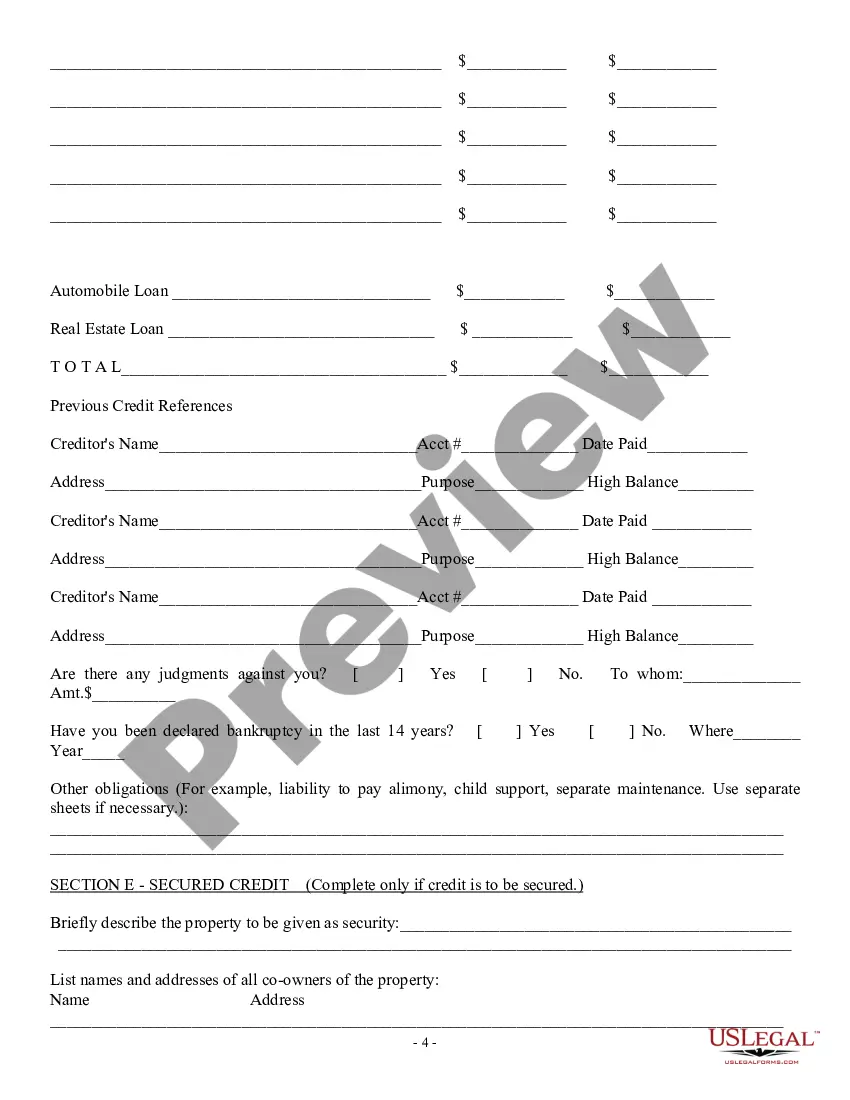

A Hillsborough Florida Consumer Loan Application — Personal Loan Agreement is a legal document that outlines the terms and conditions of borrowing money from a financial institution or lender in Hillsborough, Florida. This agreement serves as a formal contract between the borrower and the lender, ensuring transparency and protection for both parties involved. Keywords: Hillsborough Florida, consumer loan application, personal loan agreement, borrowing money, financial institution, lender, terms and conditions, formal contract, transparency, protection. Types of Hillsborough Florida Consumer Loan Application — Personal Loan Agreements: 1. Secured Personal Loan Agreement: This type of loan agreement requires the borrower to provide collateral, such as a car or property, to secure the loan. In case the borrower fails to repay the loan, the lender can seize the collateral to recover their funds. 2. Unsecured Personal Loan Agreement: Unlike a secured loan, an unsecured personal loan agreement does not require collateral. The borrower's creditworthiness and ability to repay the loan are the primary factors considered by the lender when granting the loan. This may result in a higher interest rate to compensate for the increased risk for the lender. 3. Fixed-Rate Personal Loan Agreement: In this type of loan agreement, the interest rate remains fixed throughout the loan term. This offers stability and allows the borrower to plan their budget accordingly, as the monthly payments will not change. 4. Variable-Rate Personal Loan Agreement: A variable-rate loan agreement features an interest rate that fluctuates based on an index, such as the prime rate or the LIBOR (London Interbank Offered Rate). This means that the borrower's monthly payments may vary, depending on the interest rate changes. 5. Payday Loan Agreement: This is a short-term loan agreement, typically requiring repayment by the borrower's next payday. Payday loans often have high-interest rates and fees, making them a more expensive borrowing option. 6. Installment Loan Agreement: An installment loan agreement involves borrowing a fixed amount of money, which is paid back in equal installments over a specific period. Each installment consists of a portion of the principal amount borrowed, plus interest. 7. Line of Credit Loan Agreement: A line of credit loan agreement provides the borrower with a predetermined credit limit, which they can borrow from whenever needed. Interest is charged only on the amount borrowed, not the entire credit limit. It is crucial for borrowers in Hillsborough, Florida, to carefully read and understand the terms and conditions outlined in the specific type of personal loan agreement they are entering into. It is advisable to consult with a legal professional or financial advisor before signing any loan agreement to ensure full comprehension and avoid any potential issues in the future.

Hillsborough Florida Consumer Loan Application - Personal Loan Agreement

Description

How to fill out Hillsborough Florida Consumer Loan Application - Personal Loan Agreement?

Laws and regulations in every sphere differ from state to state. If you're not an attorney, it's easy to get lost in various norms when it comes to drafting legal documentation. To avoid pricey legal assistance when preparing the Hillsborough Consumer Loan Application - Personal Loan Agreement, you need a verified template valid for your county. That's when using the US Legal Forms platform is so helpful.

US Legal Forms is a trusted by millions web library of more than 85,000 state-specific legal forms. It's a great solution for specialists and individuals searching for do-it-yourself templates for different life and business situations. All the forms can be used many times: once you pick a sample, it remains available in your profile for subsequent use. Therefore, when you have an account with a valid subscription, you can just log in and re-download the Hillsborough Consumer Loan Application - Personal Loan Agreement from the My Forms tab.

For new users, it's necessary to make a couple of more steps to get the Hillsborough Consumer Loan Application - Personal Loan Agreement:

- Analyze the page content to ensure you found the appropriate sample.

- Take advantage of the Preview option or read the form description if available.

- Look for another doc if there are inconsistencies with any of your criteria.

- Use the Buy Now button to get the template once you find the right one.

- Choose one of the subscription plans and log in or sign up for an account.

- Decide how you prefer to pay for your subscription (with a credit card or PayPal).

- Pick the format you want to save the document in and click Download.

- Complete and sign the template on paper after printing it or do it all electronically.

That's the simplest and most economical way to get up-to-date templates for any legal scenarios. Locate them all in clicks and keep your paperwork in order with the US Legal Forms!