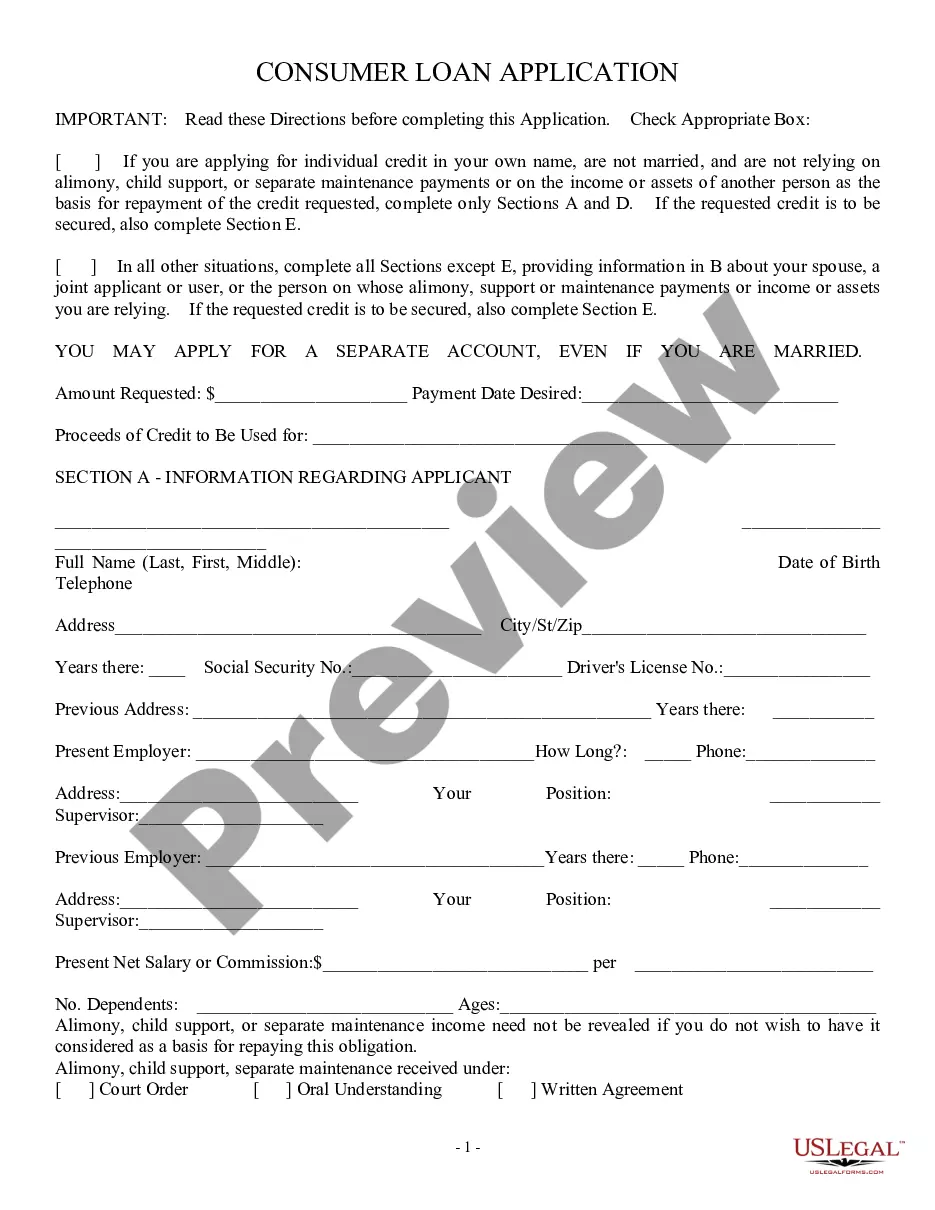

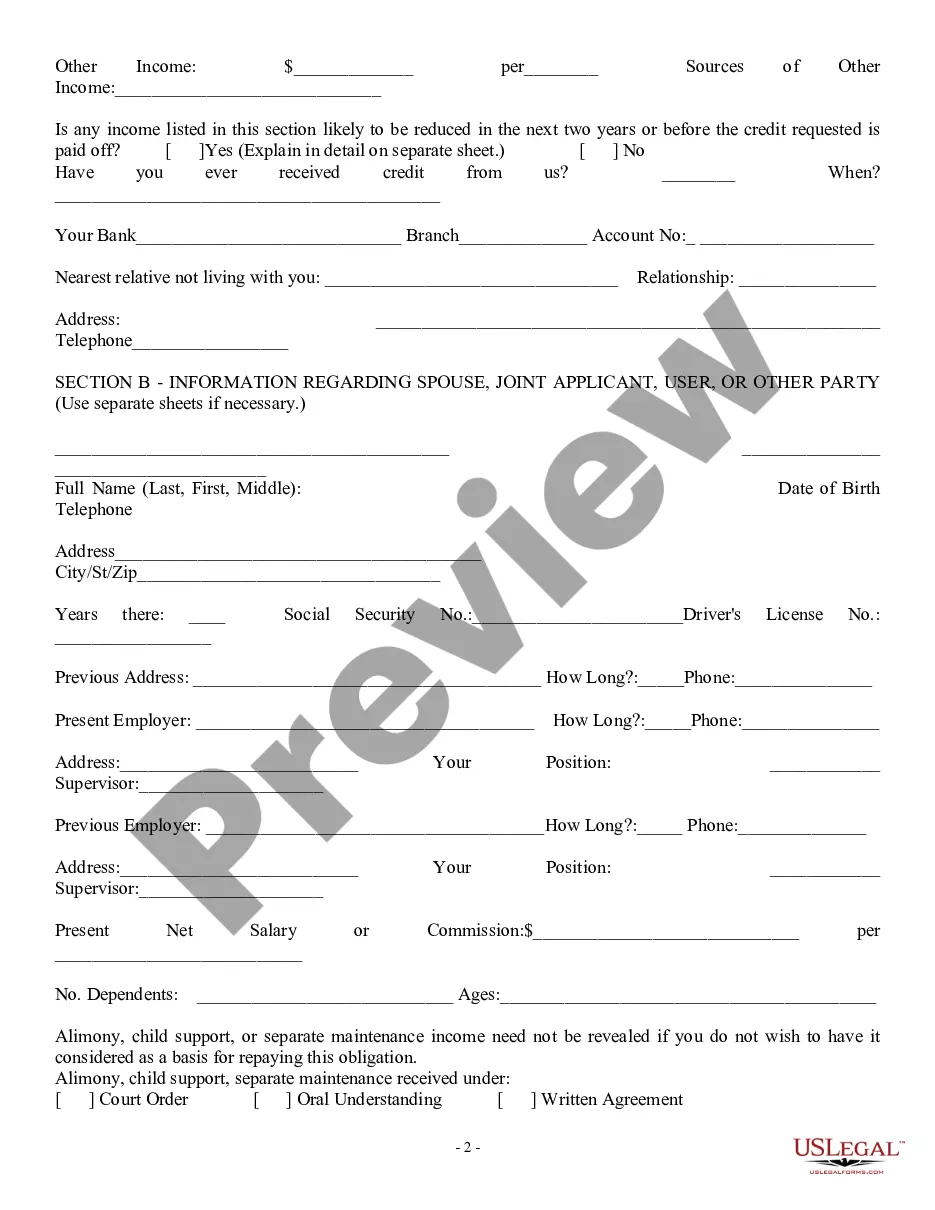

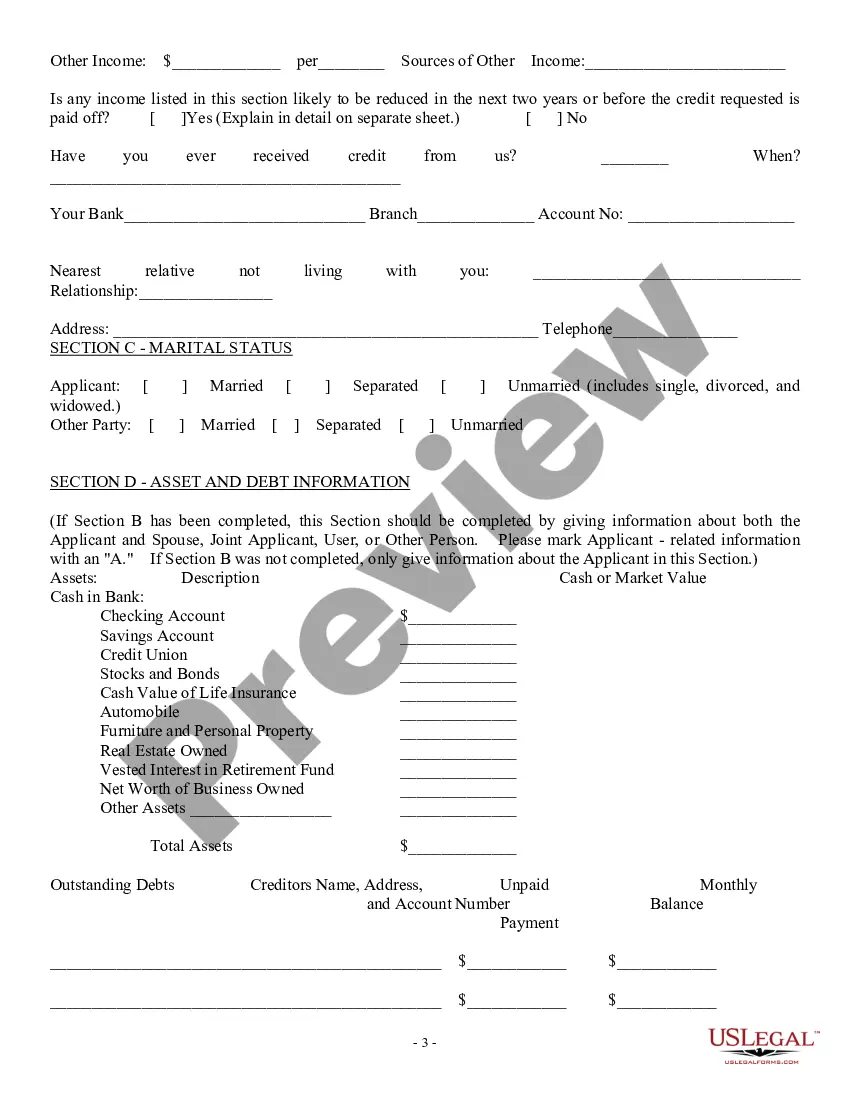

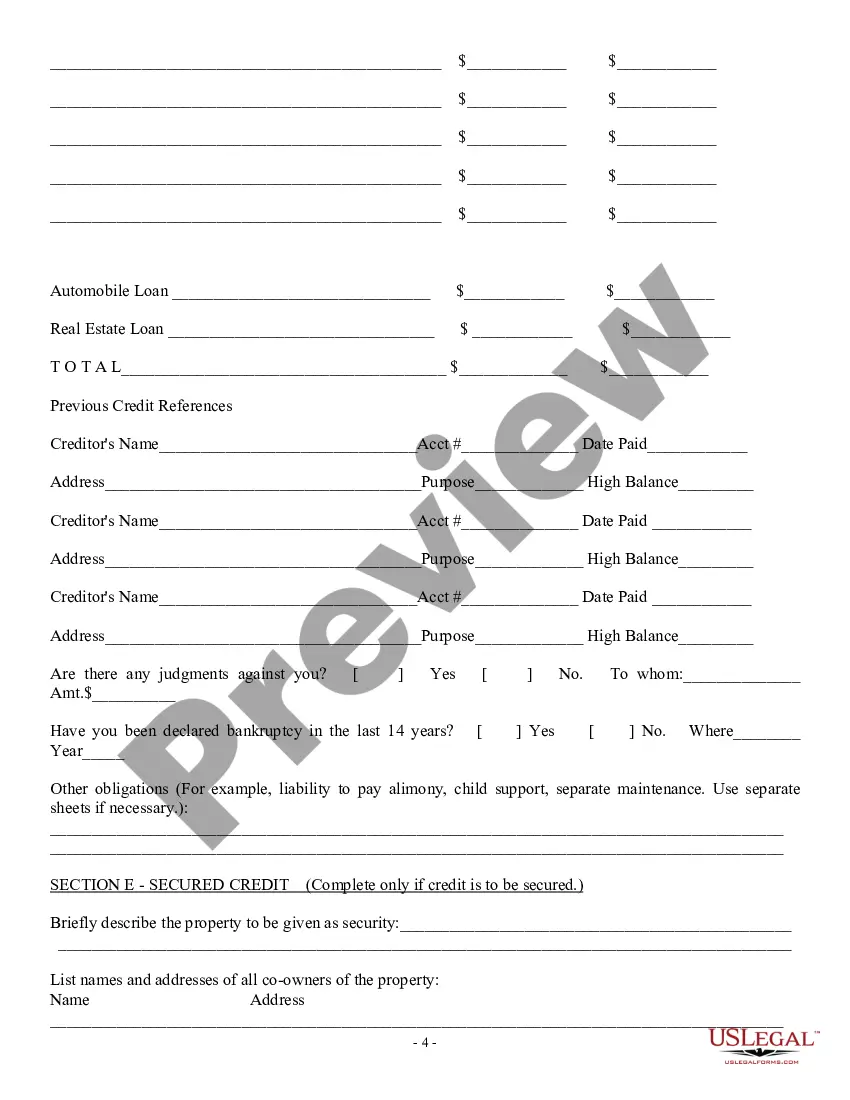

Nassau New York Consumer Loan Application — Personal Loan Agreement is a legal document that outlines the terms and conditions associated with borrowing money from a lender in Nassau, New York. The agreement serves as a binding contract between the borrower and the lender, ensuring that both parties understand their rights and responsibilities throughout the loan process. Keywords: Nassau New York, consumer loan application, personal loan agreement, terms and conditions, borrowing money, lender, binding contract, borrower, loan process. This loan agreement typically covers various aspects such as the loan amount, interest rate, repayment schedule, late payment fees, and any other relevant terms agreed upon by the borrower and the lender. It ensures transparency and mutual understanding between the parties involved, reducing the chances of disputes or misunderstandings. There may be different types of Nassau New York Consumer Loan Application — Personal Loan Agreements, depending on the specific requirements or circumstances of the borrower. Some common variations include: 1. Secured Personal Loan Agreement: This type of agreement requires the borrower to provide collateral, such as their home or vehicle, as security against the loan. If the borrower fails to repay the loan, the lender has the right to seize the collateral to recover the outstanding balance. 2. Unsecured Personal Loan Agreement: In contrast to a secured loan agreement, an unsecured loan does not require any collateral. Lenders typically assess the borrower's creditworthiness and financial stability to determine if they qualify for an unsecured loan. As there is no collateral involved, the interest rates for unsecured loans may be higher. 3. Fixed-Rate Personal Loan Agreement: This agreement establishes a fixed interest rate for the entire loan term, resulting in consistent monthly payments. Borrowers benefit from knowing exactly how much they need to repay each month, making it easier to budget and plan their finances. 4. Variable-Rate Personal Loan Agreement: With this type of agreement, the interest rate on the loan may vary over time based on certain market factors or economic conditions. This flexibility can be advantageous if interest rates are expected to decrease, but it also poses the risk of higher payments if the rates increase. 5. Payday Loan Agreement: Payday loans are typically short-term loans that are intended to be repaid by the borrower's next paycheck. These loans often come with high-interest rates and hefty finance charges. It's important for borrowers to carefully review and understand the terms of payday loan agreements before proceeding. Overall, the Nassau New York Consumer Loan Application — Personal Loan Agreement ensures a clear understanding of the loan arrangement, protects the rights of both parties, and provides a legal framework for resolving any disputes.

Nassau New York Consumer Loan Application - Personal Loan Agreement

Description

How to fill out Nassau New York Consumer Loan Application - Personal Loan Agreement?

Preparing legal paperwork can be cumbersome. In addition, if you decide to ask a legal professional to draft a commercial agreement, documents for ownership transfer, pre-marital agreement, divorce paperwork, or the Nassau Consumer Loan Application - Personal Loan Agreement, it may cost you a fortune. So what is the best way to save time and money and create legitimate forms in total compliance with your state and local regulations? US Legal Forms is a perfect solution, whether you're searching for templates for your personal or business needs.

US Legal Forms is the most extensive online catalog of state-specific legal documents, providing users with the up-to-date and professionally verified forms for any scenario gathered all in one place. Consequently, if you need the recent version of the Nassau Consumer Loan Application - Personal Loan Agreement, you can easily locate it on our platform. Obtaining the papers requires a minimum of time. Those who already have an account should check their subscription to be valid, log in, and select the sample by clicking on the Download button. If you haven't subscribed yet, here's how you can get the Nassau Consumer Loan Application - Personal Loan Agreement:

- Glance through the page and verify there is a sample for your region.

- Examine the form description and use the Preview option, if available, to make sure it's the template you need.

- Don't worry if the form doesn't suit your requirements - look for the right one in the header.

- Click Buy Now when you find the required sample and select the best suitable subscription.

- Log in or register for an account to pay for your subscription.

- Make a transaction with a credit card or through PayPal.

- Choose the document format for your Nassau Consumer Loan Application - Personal Loan Agreement and download it.

When done, you can print it out and complete it on paper or import the template to an online editor for a faster and more practical fill-out. US Legal Forms allows you to use all the paperwork ever acquired many times - you can find your templates in the My Forms tab in your profile. Give it a try now!