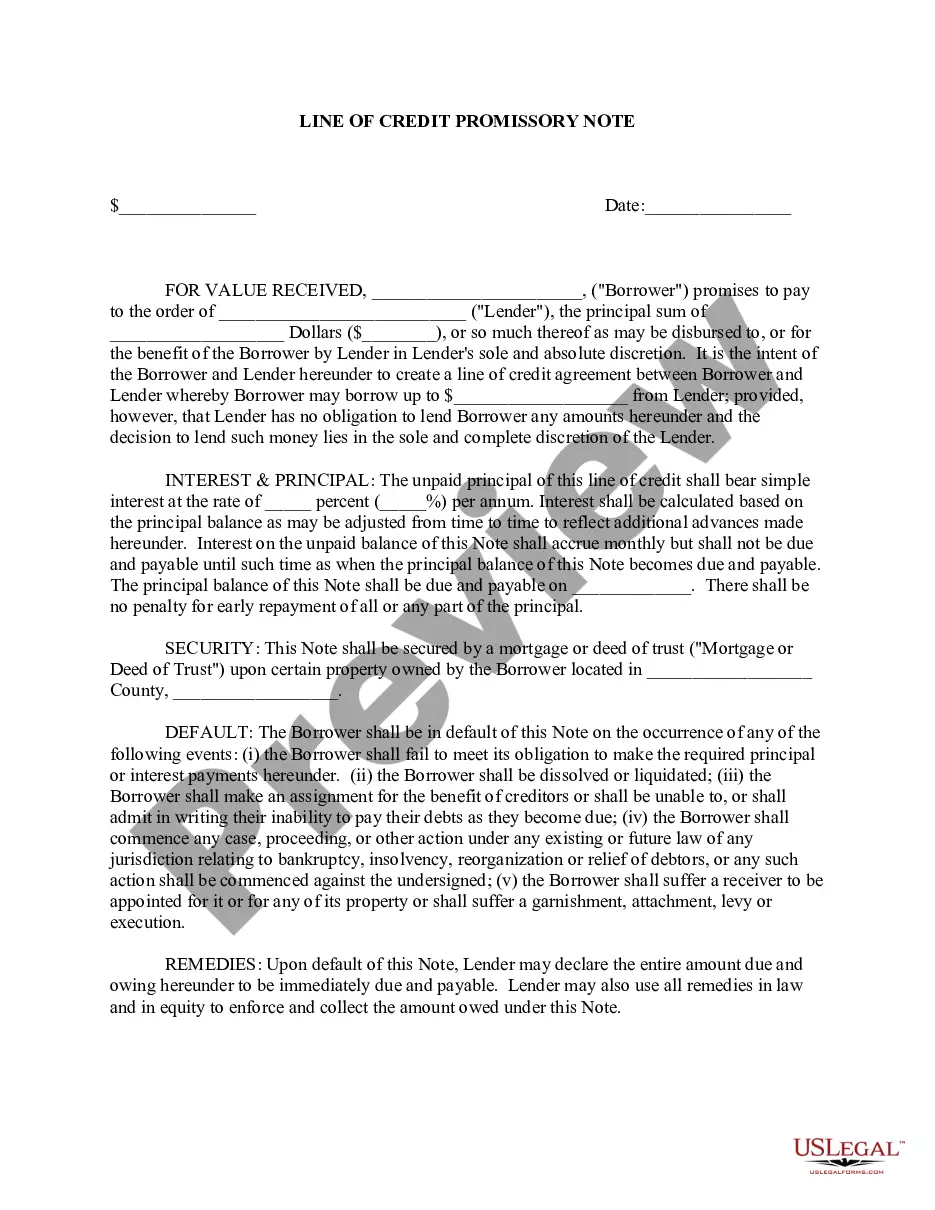

The Wake North Carolina Line of Credit Promissory Note is a legal document that outlines the terms and conditions under which a borrower obtains a line of credit from a financial institution located in the state of North Carolina. It is an agreement between the borrower and the lender, and it serves as a binding contract that ensures the borrower's repayment obligations. The Wake North Carolina Line of Credit Promissory Note typically contains key information such as the names and contact details of the borrower and lender, the principal amount of the line of credit, the interest rate applicable, the repayment terms, and any additional fees or charges involved. It also specifies the repayment schedule, the frequency of payments, and any grace periods or late payment penalties. This type of promissory note is commonly used by individuals, businesses, or organizations seeking a flexible form of financing. It allows borrowers to borrow funds as needed up to a predetermined credit limit, similar to a credit card. The line of credit can be drawn upon multiple times without the need for additional loan applications, providing convenience and quick access to funds. There may be different types of Wake North Carolina Line of Credit Promissory Note depending on the specific terms and conditions set by the lender. Some variations include: 1. Secured Line of Credit Promissory Note: This type of promissory note requires the borrower to provide collateral as security for the line of credit. Collateral can be in the form of real estate, a vehicle, or other valuable assets. In the event of default, the lender has the right to seize the collateral to satisfy the outstanding debt. 2. Unsecured Line of Credit Promissory Note: Unlike a secured line of credit, an unsecured line of credit does not require collateral. Instead, the lender evaluates the borrower's creditworthiness based on their credit history, income, and other factors. Since it carries higher risk for the lender, an unsecured line of credit may have a higher interest rate. 3. Personal Line of Credit Promissory Note: This type of promissory note is designed for individual borrowers who need access to funds for personal reasons. It can be used for various purposes, such as unexpected expenses, home renovations, or educational costs. 4. Business Line of Credit Promissory Note: A business line of credit is specifically tailored for small businesses or entrepreneurs who require ongoing funding for their operations. It offers flexibility and convenience, allowing business owners to maintain a consistent cash flow, cover short-term expenses, or invest in growth opportunities. In summary, the Wake North Carolina Line of Credit Promissory Note is a legal contract that governs the terms and conditions for obtaining a line of credit in North Carolina. Various types of this promissory note exist, depending on factors such as collateral requirements, creditworthiness evaluation, and the purpose of the line of credit.

Wake North Carolina Line of Credit Promissory Note

Description

How to fill out Wake North Carolina Line Of Credit Promissory Note?

Creating legal forms is a must in today's world. However, you don't always need to seek professional help to draft some of them from scratch, including Wake Line of Credit Promissory Note, with a service like US Legal Forms.

US Legal Forms has more than 85,000 templates to pick from in different types ranging from living wills to real estate papers to divorce documents. All forms are arranged according to their valid state, making the searching experience less challenging. You can also find detailed resources and tutorials on the website to make any activities related to document completion simple.

Here's how to purchase and download Wake Line of Credit Promissory Note.

- Go over the document's preview and description (if available) to get a general idea of what you’ll get after downloading the document.

- Ensure that the template of your choice is specific to your state/county/area since state laws can impact the validity of some records.

- Examine the related forms or start the search over to locate the right document.

- Hit Buy now and create your account. If you already have an existing one, choose to log in.

- Choose the option, then a suitable payment gateway, and buy Wake Line of Credit Promissory Note.

- Choose to save the form template in any available file format.

- Go to the My Forms tab to re-download the document.

If you're already subscribed to US Legal Forms, you can locate the appropriate Wake Line of Credit Promissory Note, log in to your account, and download it. Of course, our platform can’t take the place of a legal professional completely. If you have to deal with an extremely challenging situation, we recommend getting an attorney to review your document before signing and filing it.

With more than 25 years on the market, US Legal Forms proved to be a go-to platform for many different legal forms for millions of customers. Become one of them today and get your state-compliant documents effortlessly!