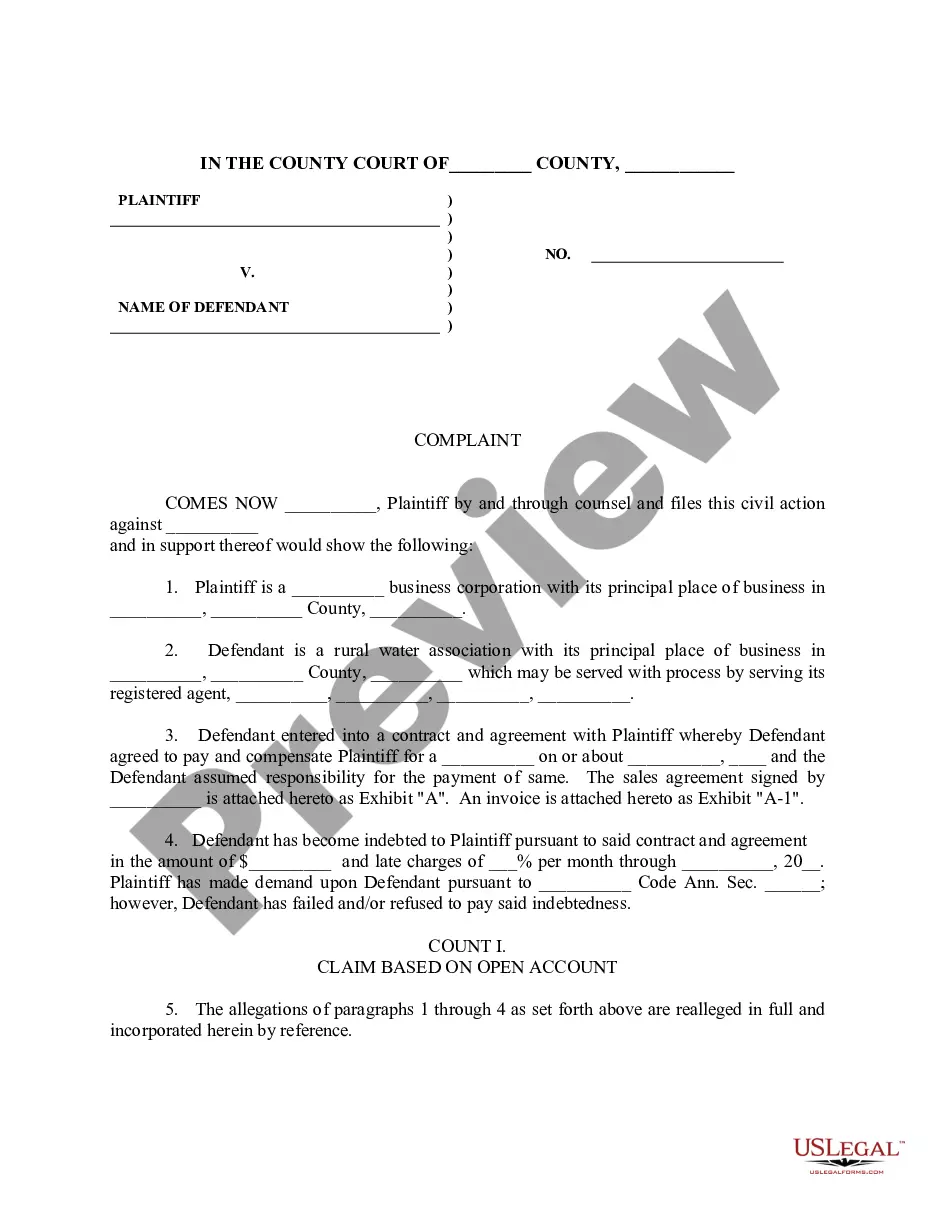

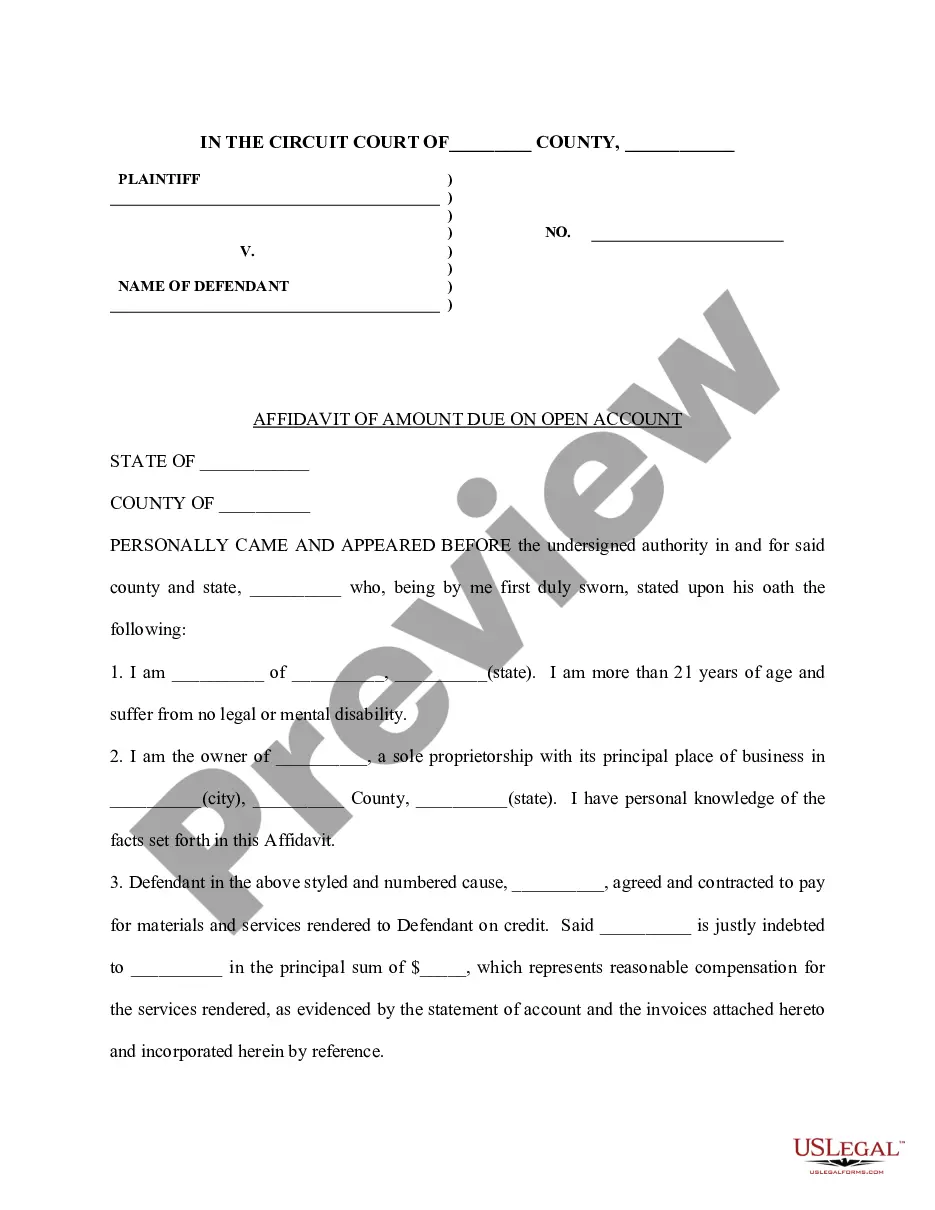

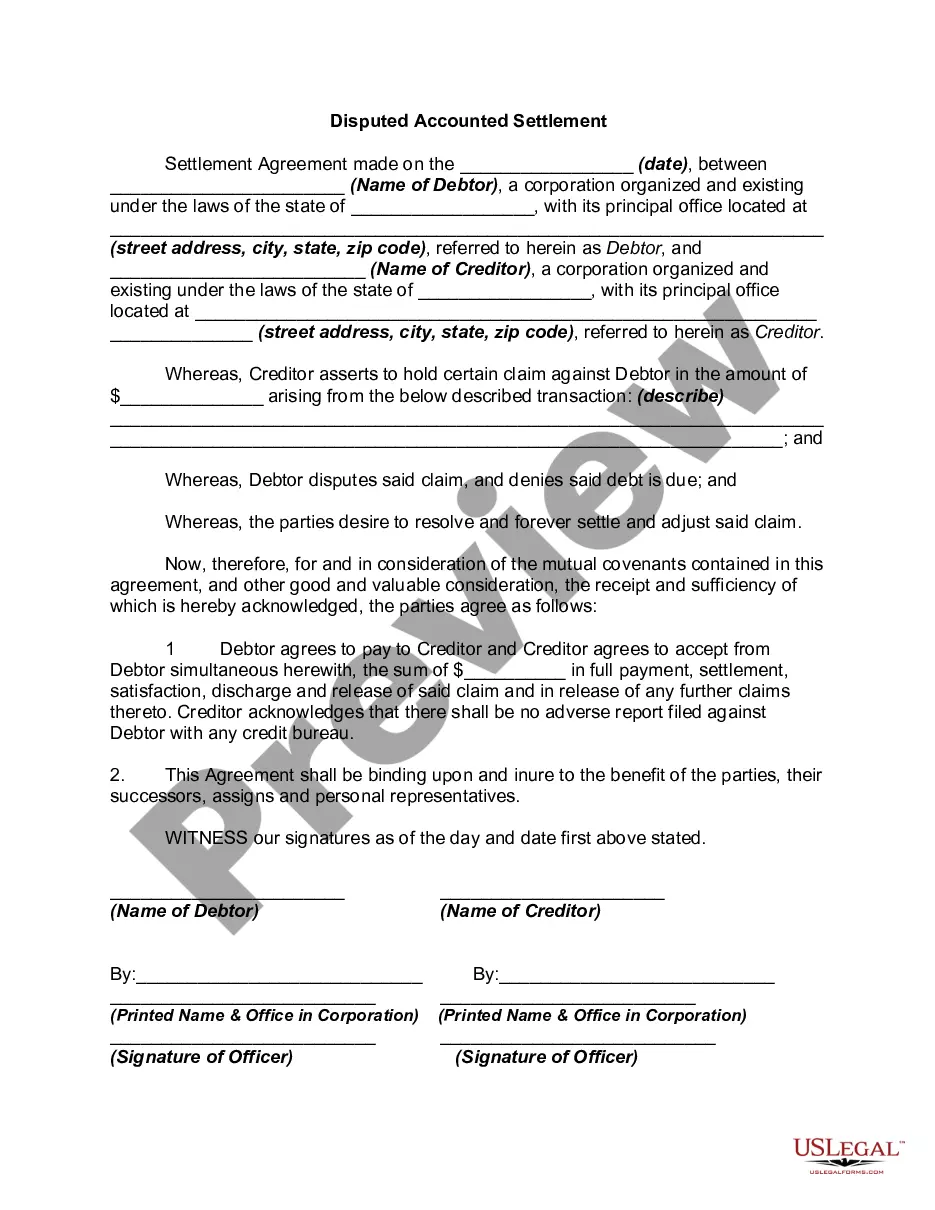

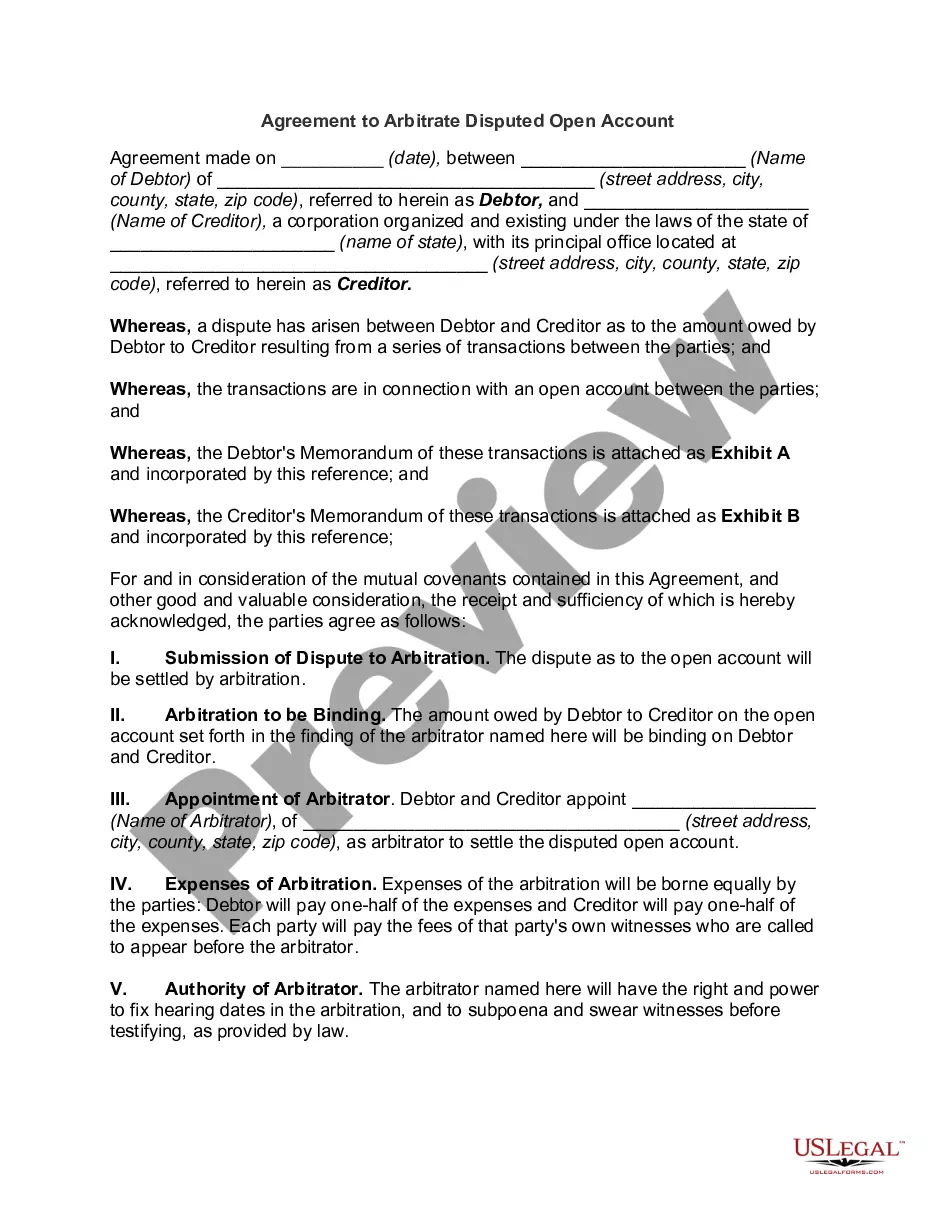

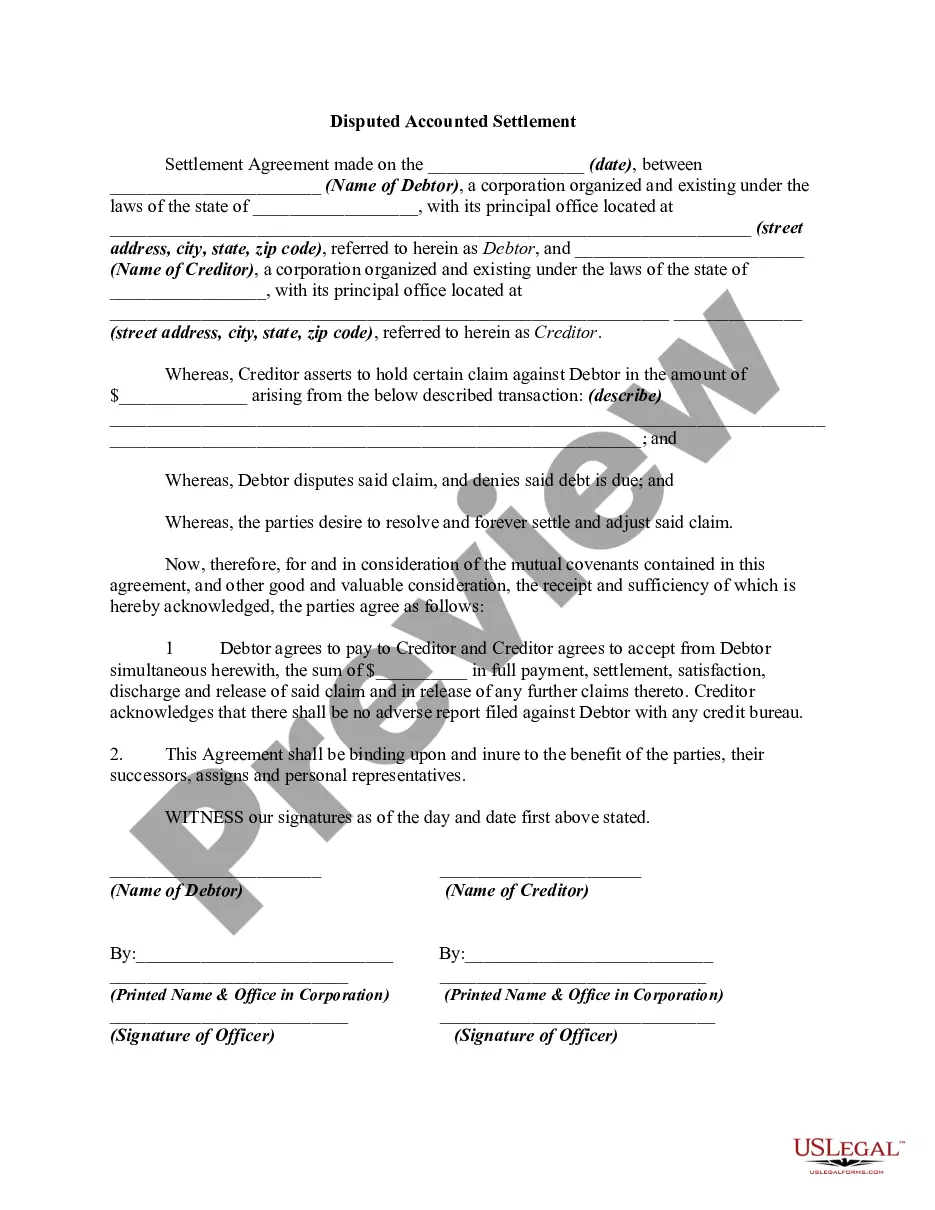

Oakland Michigan Disputed Open Account Settlement

Description

How to fill out Disputed Open Account Settlement?

Creating documents, such as the Oakland Contested Open Account Settlement, to oversee your legal matters is a challenging and lengthy endeavor.

Numerous scenarios necessitate an attorney's assistance, which further escalates the costs associated with this task.

Nevertheless, you can take control of your legal concerns and handle them independently.

The registration process for new users is equally uncomplicated! Here’s what you need to do prior to obtaining the Oakland Contested Open Account Settlement: Ensure that your document is tailored to your state/county since the requirements for drafting legal paperwork might differ from state to state.

- US Legal Forms is here to assist you.

- Our site offers over 85,000 legal documents designed for different situations and life events.

- We ensure that each form complies with the laws of every state, relieving you of concerns about legal compliance.

- If you're familiar with our offerings and possess a subscription with US, retrieving the Oakland Contested Open Account Settlement template is a breeze.

- Simply Log In to your account, download the document, and customize it to your needs.

- Misplaced your document? No problem. You can access it in the My documents section of your account - whether on desktop or mobile.

Form popularity

FAQ

It can be beneficial to pay off derogatory credit items that remain on your credit report. Your credit score may not go up right away after paying off a negative item. However, most lenders won't approve a mortgage application if you have unpaid derogatory items on your credit report.

You can remove closed accounts from your credit report in three main ways: dispute any inaccuracies, write a formal goodwill letter requesting removal or simply wait for the closed accounts to be removed over time.

"The 609 loophole is a section of the Fair Credit Reporting Act that says that if something is incorrect on your credit report, you have the right to write a letter disputing it," said Robin Saks Frankel, a personal finance expert with Forbes Advisor.

Yes, you can remove a settled account from your credit report. A settled account means you paid your outstanding balance in full or less than the amount owed. Otherwise, a settled account will appear on your credit report for up to 7.5 years from the date it was fully paid or closed.

A credit dispute letter doesn't automatically fix this issue or repair your credit. And there are no guarantees the credit reporting agency will remove an itemespecially if you don't have strong documentation that it's an error. But writing a credit dispute letter costs little more than a bit of time.

Send your 609 letter to each of the credit reporting agencies that are listing the account you need verified: Experian. P.O. Box 4500. Allen, TX 75013. TransUnion Consumer Solutions. P.O. Box 2000. Chester, PA 19016-2000. Equifax. P.O. Box 740256. Atlanta, GA 30374-0256.

Your letter should identify each item you dispute, state the facts, explain why you dispute the information, and ask that the business that supplied the information take action to have it removed or corrected.

There's no evidence to suggest a 609 letter is more or less effective than the usual process of disputing an error on your credit reportit's just another method of gathering information and seeking verification of the accuracy of the report. If disputes are successful, the credit bureaus may remove the negative item.

A 609 dispute letter is a letter sent to the bureaus requesting this information is actually not a dispute but is simply a way of requesting that the credit bureaus provide you with certain documentation that substantiates the authenticity of the bureaus' reporting.

A 609 letter is a credit repair method that requests credit bureaus to remove erroneous negative entries from your credit report. It's named after section 609 of the Fair Credit Reporting Act (FCRA), a federal law that protects consumers from unfair credit and collection practices. Written by Natasha Wiebusch, J.D..