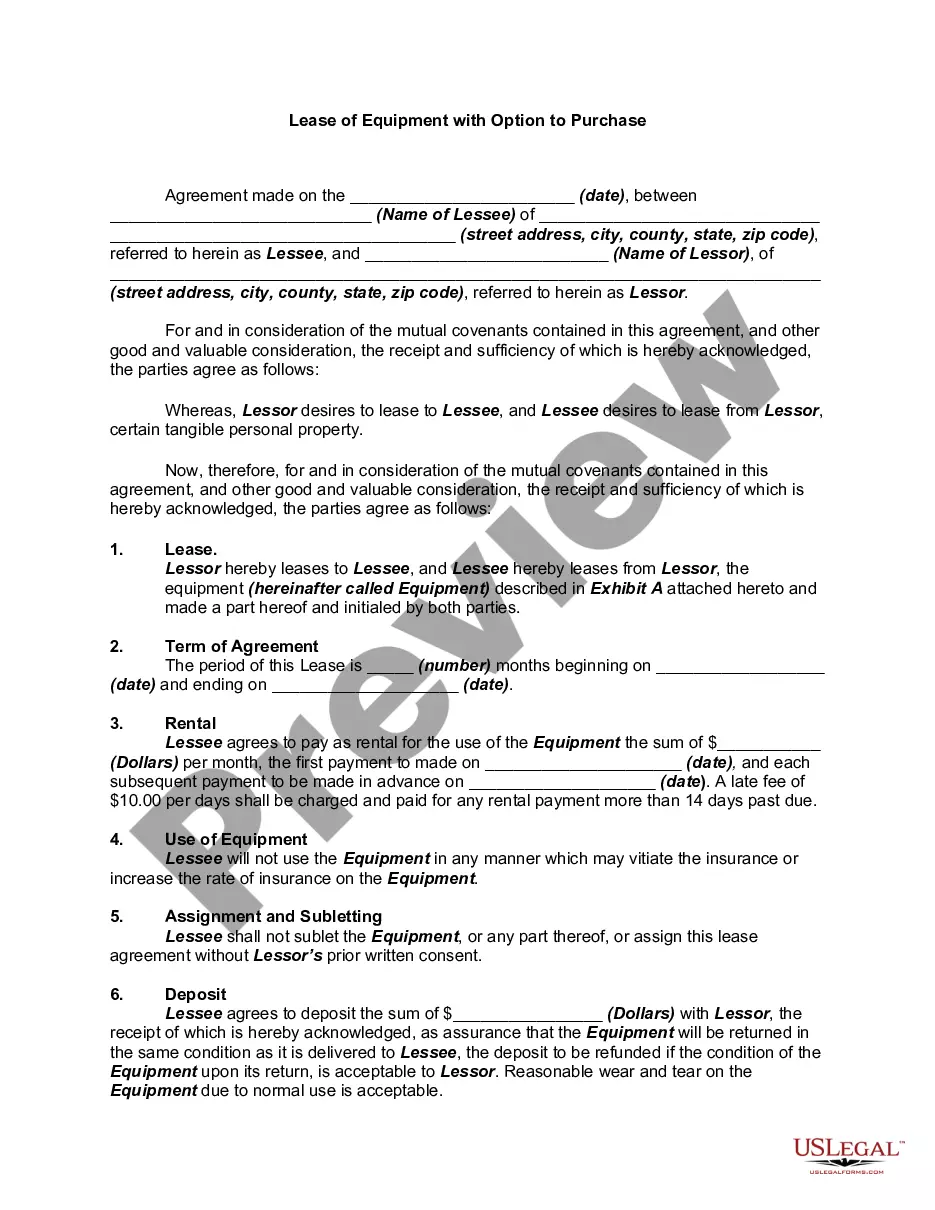

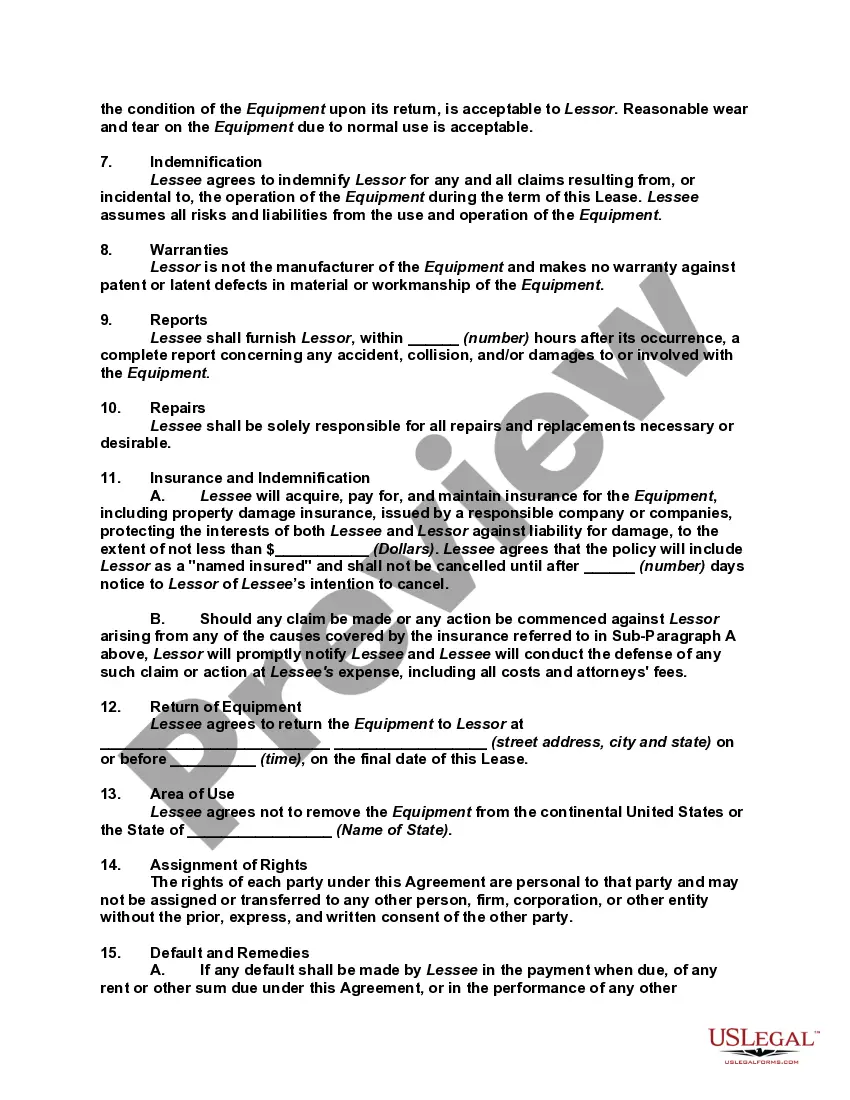

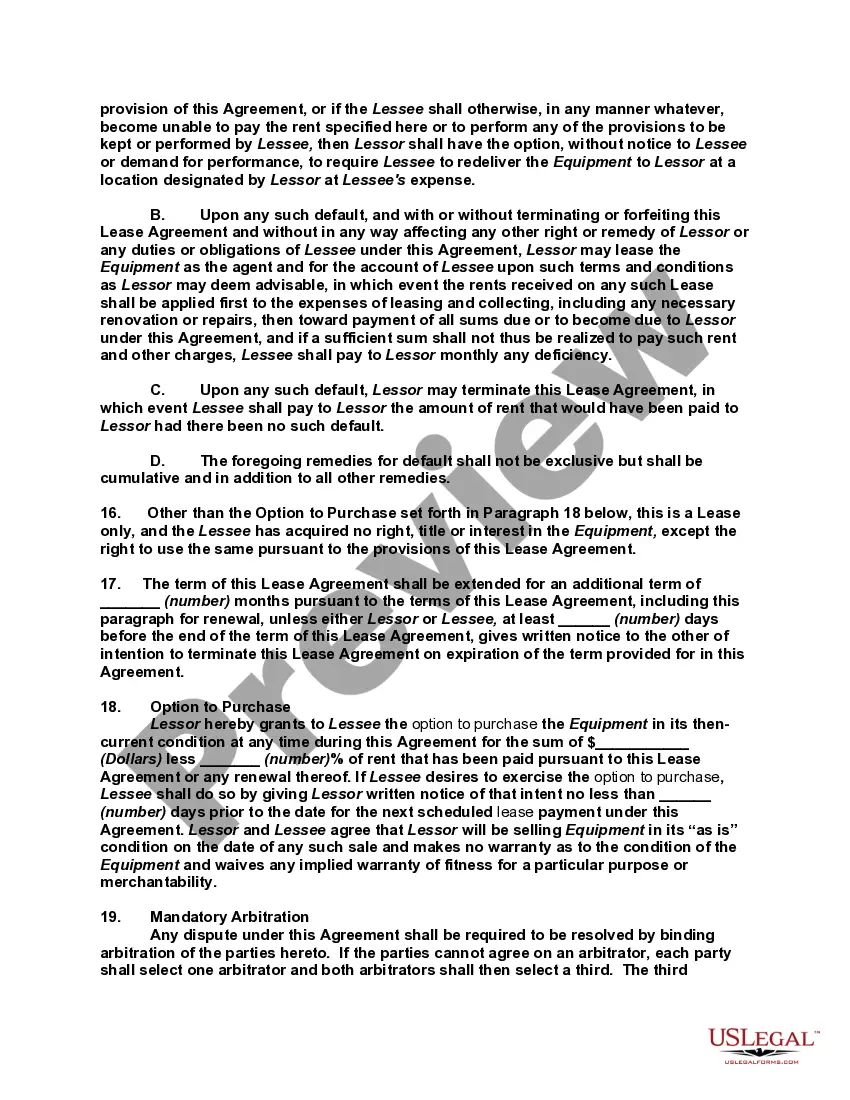

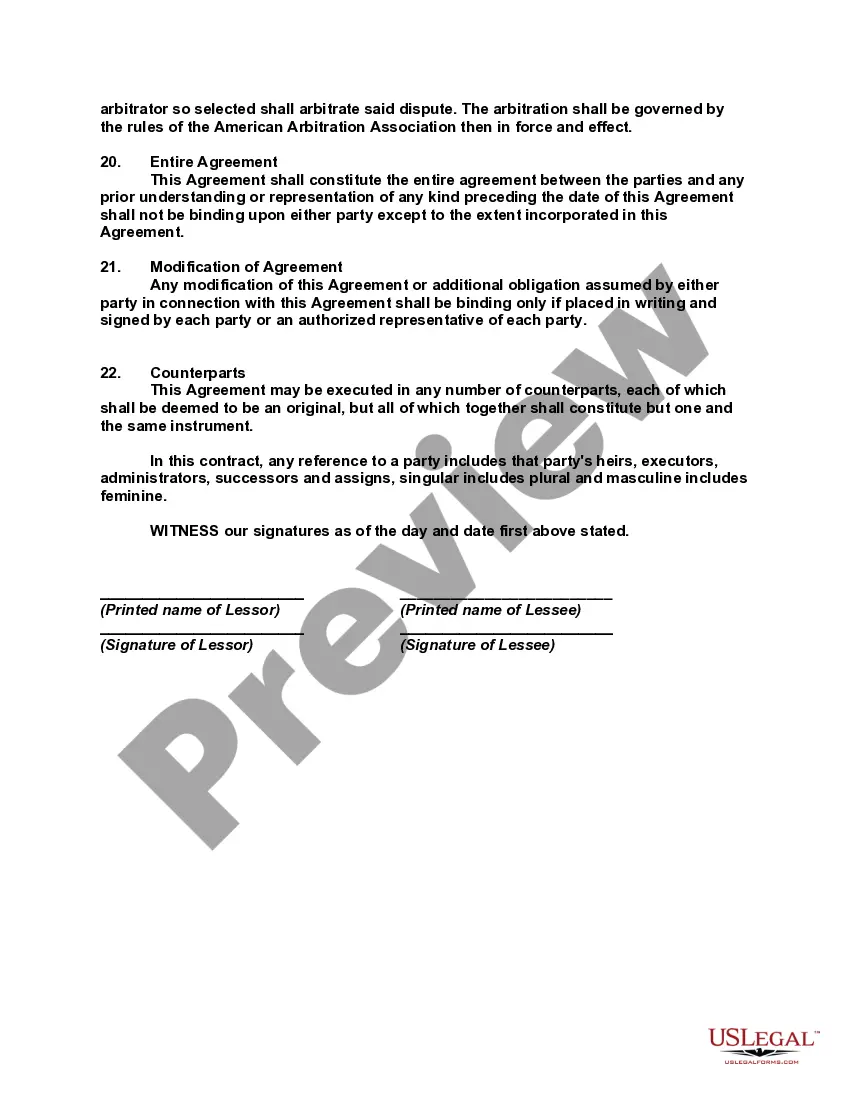

A Nassau New York Lease Purchase Agreement for Equipment is a legally binding contract that allows individuals or businesses in Nassau County, New York, to lease and eventually purchase equipment. This agreement provides flexibility and convenience for those who need equipment but may not have the immediate funds to purchase it outright. Under this agreement, the lessee is granted the right to use the equipment for a specified period, typically ranging from one to five years. During this time, the lessee makes regular rental payments to the lessor, which can be applied towards the final purchase price. Once the lease term is fulfilled and all payments are made, the lessee obtains ownership of the equipment. One type of Nassau New York Lease Purchase Agreement for Equipment is the Capital Lease Agreement. In this case, the lessee fully intends to purchase the equipment by the end of the lease term. The agreement may include a predetermined purchase option for a nominal amount, such as $1, or a fair market value at the time of purchase. Another type is the Finance Lease Agreement, which operates similarly to a loan. The lessee pays a fixed monthly amount, but the total payment tends to be higher than the actual equipment value. Finance lease agreements are often used when the equipment being leased has a more extended lifespan. This Lease Purchase Agreement provides numerous advantages to businesses in Nassau New York. First and foremost, it enables companies to acquire the necessary equipment without a significant upfront investment, preserving their capital for other essential business operations. Additionally, it allows for an easy upgrading and replacement process, ensuring that the lessee always has access to the latest technology without additional costs. Throughout the agreement, both parties have specific responsibilities. The lessor is responsible for maintaining the equipment in good working order, providing necessary repairs, and ensuring compliance with applicable laws and regulations. The lessee, on the other hand, must cover insurance costs and utilize the equipment in a manner consistent with its intended purpose. To summarize, the Nassau New York Lease Purchase Agreement for Equipment is a flexible and beneficial arrangement that allows individuals and businesses to acquire much-needed equipment without an immediate purchase. The Capital Lease and Finance Lease are two common types of agreements that suit different circumstances. By utilizing this agreement, lessees in Nassau County, New York, can secure access to essential equipment while preserving their financial resources.

Nassau New York Lease Purchase Agreement for Equipment

Description

How to fill out Nassau New York Lease Purchase Agreement For Equipment?

Drafting documents for the business or individual demands is always a huge responsibility. When creating a contract, a public service request, or a power of attorney, it's essential to take into account all federal and state laws of the specific area. However, small counties and even cities also have legislative provisions that you need to consider. All these aspects make it burdensome and time-consuming to generate Nassau Lease Purchase Agreement for Equipment without expert help.

It's possible to avoid spending money on lawyers drafting your paperwork and create a legally valid Nassau Lease Purchase Agreement for Equipment on your own, using the US Legal Forms web library. It is the most extensive online catalog of state-specific legal documents that are professionally cheched, so you can be certain of their validity when selecting a sample for your county. Earlier subscribed users only need to log in to their accounts to save the necessary document.

If you still don't have a subscription, follow the step-by-step instruction below to obtain the Nassau Lease Purchase Agreement for Equipment:

- Examine the page you've opened and check if it has the sample you require.

- To accomplish this, use the form description and preview if these options are presented.

- To locate the one that fits your needs, utilize the search tab in the page header.

- Double-check that the template complies with juridical criteria and click Buy Now.

- Opt for the subscription plan, then log in or create an account with the US Legal Forms.

- Utilize your credit card or PayPal account to pay for your subscription.

- Download the chosen document in the preferred format, print it, or complete it electronically.

The exceptional thing about the US Legal Forms library is that all the paperwork you've ever purchased never gets lost - you can get it in your profile within the My Forms tab at any moment. Join the platform and quickly get verified legal forms for any scenario with just a couple of clicks!