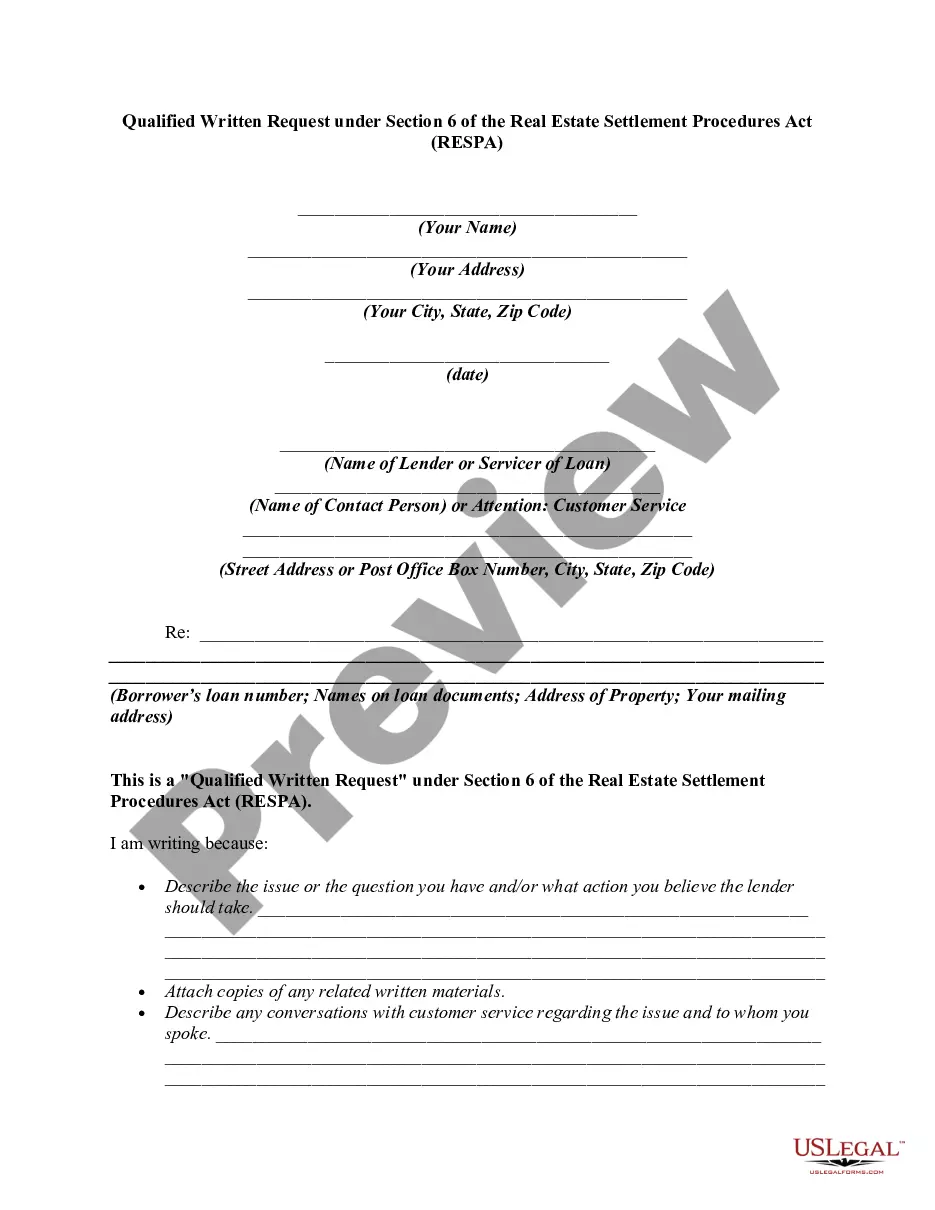

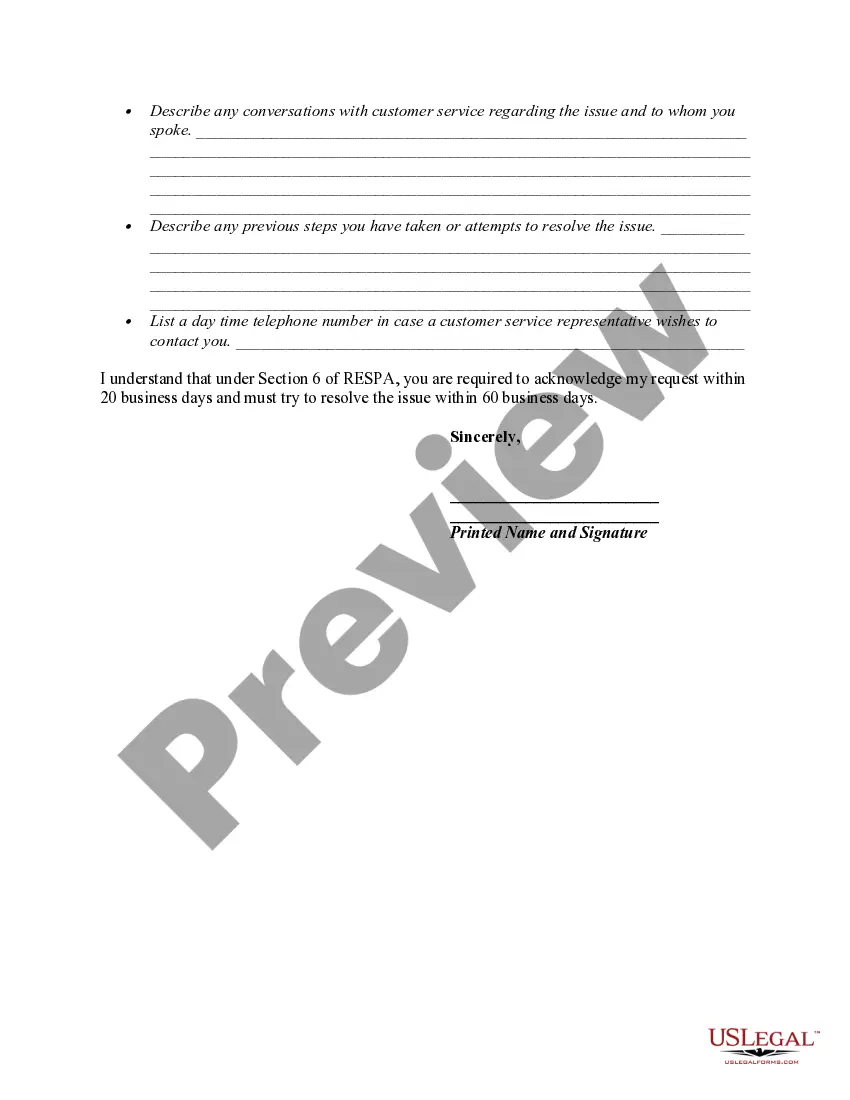

12 USC 2605(e) creates a duty of a loan servicer to respond to the inquiries of borrowers regarding loans covered by RESPA. If the borrower believes there is an error in the mortgage account, he or she can make a "qualified written request" to the loan servicer. The request must be in writing, identify the borrower by name and account, and include a statement of reasons why the borrower believes the account is in error. The request should include the words "qualified written request". It cannot be written on the payment coupon, but must be on a separate piece of paper. The Department of Housing and Urban Development provides a sample letter.

The servicer must acknowledge receipt of the request within 20 days. The servicer then has 60 days (from the request) to take action on the request. The servicer has to either provide a written notification that the error has been corrected, or provide a written explanation as to why the servicer believes the account is correct. Either way, the servicer has to provide the name and telephone number of a person with whom the borrower can discuss the matter.

A Hennepin Minnesota Qualified Written Request (BWR) under Section 6 of the Real Estate Settlement Procedures Act (RESP) is a formal letter sent by a borrower to their mortgage service, typically a financial institution or loan service, to obtain specific information or resolve issues related to their mortgage loan. A Hennepin Minnesota BWR is a legally binding document that helps borrowers exercise their rights and protections under RESP, ensuring transparency and accountability in the mortgage servicing process. By sending a BWR, borrowers can request information about their loan, clarify discrepancies, dispute errors, and address concerns regarding loan modification, loan payment, escrow accounts, and other relevant matters. Some key components of a Hennepin Minnesota BWR include: 1. Contact Information: The borrower's full name, address, phone number, and loan account number should be clearly stated in the BWR. 2. Description of Requests: The BWR should clearly state the specific information or actions requested from the mortgage service. This may include details about the loan terms, payment history, escrow analysis, fees, charges, and any other relevant documentation. 3. Explanation of Discrepancies or Errors: If the borrower has identified discrepancies or errors in the mortgage servicing, the BWR should provide a detailed explanation along with supporting evidence, such as payment records, statements, or other relevant documents. 4. Timelines and Deadlines: The borrower may set a reasonable timeline for the mortgage service to respond to the BWR to ensure prompt resolution of the issues. This deadline should comply with RESP guidelines and state laws. 5. Legal References: The BWR may include references to relevant RESP sections, regulations, and other applicable laws to strengthen the borrower's request and ensure compliance by the mortgage service. It is important to note that while a Hennepin Minnesota BWR serves as a powerful tool for borrowers, there are no specific "types" of Was under RESP. The structure and content of a BWR generally remain the same; however, the specific details and requests may vary depending on the borrower's unique circumstances and concerns. In conclusion, a Hennepin Minnesota BWR under Section 6 of RESP provides borrowers with a formal mechanism to request information, resolve disputes, and seek redress related to their mortgage loans. By issuing a well-crafted BWR, borrowers can safeguard their rights and navigate the mortgage servicing process effectively.A Hennepin Minnesota Qualified Written Request (BWR) under Section 6 of the Real Estate Settlement Procedures Act (RESP) is a formal letter sent by a borrower to their mortgage service, typically a financial institution or loan service, to obtain specific information or resolve issues related to their mortgage loan. A Hennepin Minnesota BWR is a legally binding document that helps borrowers exercise their rights and protections under RESP, ensuring transparency and accountability in the mortgage servicing process. By sending a BWR, borrowers can request information about their loan, clarify discrepancies, dispute errors, and address concerns regarding loan modification, loan payment, escrow accounts, and other relevant matters. Some key components of a Hennepin Minnesota BWR include: 1. Contact Information: The borrower's full name, address, phone number, and loan account number should be clearly stated in the BWR. 2. Description of Requests: The BWR should clearly state the specific information or actions requested from the mortgage service. This may include details about the loan terms, payment history, escrow analysis, fees, charges, and any other relevant documentation. 3. Explanation of Discrepancies or Errors: If the borrower has identified discrepancies or errors in the mortgage servicing, the BWR should provide a detailed explanation along with supporting evidence, such as payment records, statements, or other relevant documents. 4. Timelines and Deadlines: The borrower may set a reasonable timeline for the mortgage service to respond to the BWR to ensure prompt resolution of the issues. This deadline should comply with RESP guidelines and state laws. 5. Legal References: The BWR may include references to relevant RESP sections, regulations, and other applicable laws to strengthen the borrower's request and ensure compliance by the mortgage service. It is important to note that while a Hennepin Minnesota BWR serves as a powerful tool for borrowers, there are no specific "types" of Was under RESP. The structure and content of a BWR generally remain the same; however, the specific details and requests may vary depending on the borrower's unique circumstances and concerns. In conclusion, a Hennepin Minnesota BWR under Section 6 of RESP provides borrowers with a formal mechanism to request information, resolve disputes, and seek redress related to their mortgage loans. By issuing a well-crafted BWR, borrowers can safeguard their rights and navigate the mortgage servicing process effectively.