Nassau New York Adjustable Rate Rider - Variable Rate Note

Description

How to fill out Adjustable Rate Rider - Variable Rate Note?

Drafting legal documents can be taxing.

Moreover, if you choose to hire an attorney to create a business contract, papers for title transfer, pre-nuptial agreement, divorce documents, or the Nassau Adjustable Rate Rider - Variable Rate Note, it could be quite expensive.

Browse the page to confirm that there is a sample available for your area.

- What is the most effective method to conserve time and funds while producing valid forms that fully comply with your state and local regulations.

- US Legal Forms serves as an excellent option, whether you're in need of templates for personal or corporate purposes.

- US Legal Forms is the largest online repository of state-specific legal documents, offering users the latest and professionally validated forms for any situation, all consolidated in one location.

- Therefore, if you're seeking the most current version of the Nassau Adjustable Rate Rider - Variable Rate Note, you can effortlessly find it on our platform.

- Securing the documents requires minimal time.

- Users with existing accounts should ensure their subscriptions are active, Log In, and select the sample using the Download button.

- If you haven't subscribed yet, here’s how to obtain the Nassau Adjustable Rate Rider - Variable Rate Note.

Form popularity

FAQ

The term 'adjustable rate rider' refers to a written agreement attached to a mortgage that details how the interest rate can change over time. This is often linked to financial indices, which can lead to fluctuations in your monthly payments. Understanding this term is vital when exploring options like the Nassau New York Adjustable Rate Rider - Variable Rate Note, as it directly impacts your borrowing experience.

In a mortgage context, a rider is an addendum that modifies the terms of the original mortgage agreement, often adding provisions for specific scenarios. Riders can clarify details about adjustable rates, like those found in the Nassau New York Adjustable Rate Rider - Variable Rate Note. Understanding these addendums helps borrowers grasp their responsibilities and options.

The difference between a fixed rate and an adjustable rate mortgage is that, for fixed rates the interest rate is set when you take out the loan and will not change. With an adjustable rate mortgage, the interest rate may go up or down. Many ARMs will start at a lower interest rate than fixed rate mortgages.

An adjustable-rate mortgage (ARM) is a home loan with a variable interest rate. With an ARM, the initial interest rate is fixed for a period of time. After that, the interest rate applied on the outstanding balance resets periodically, at yearly or even monthly intervals.

A variable rate mortgage is one where the interest rates change with the market but the monthly payments are always the same. An adjustable rate mortgage is one where the monthly payments can change when the interest rate changes.

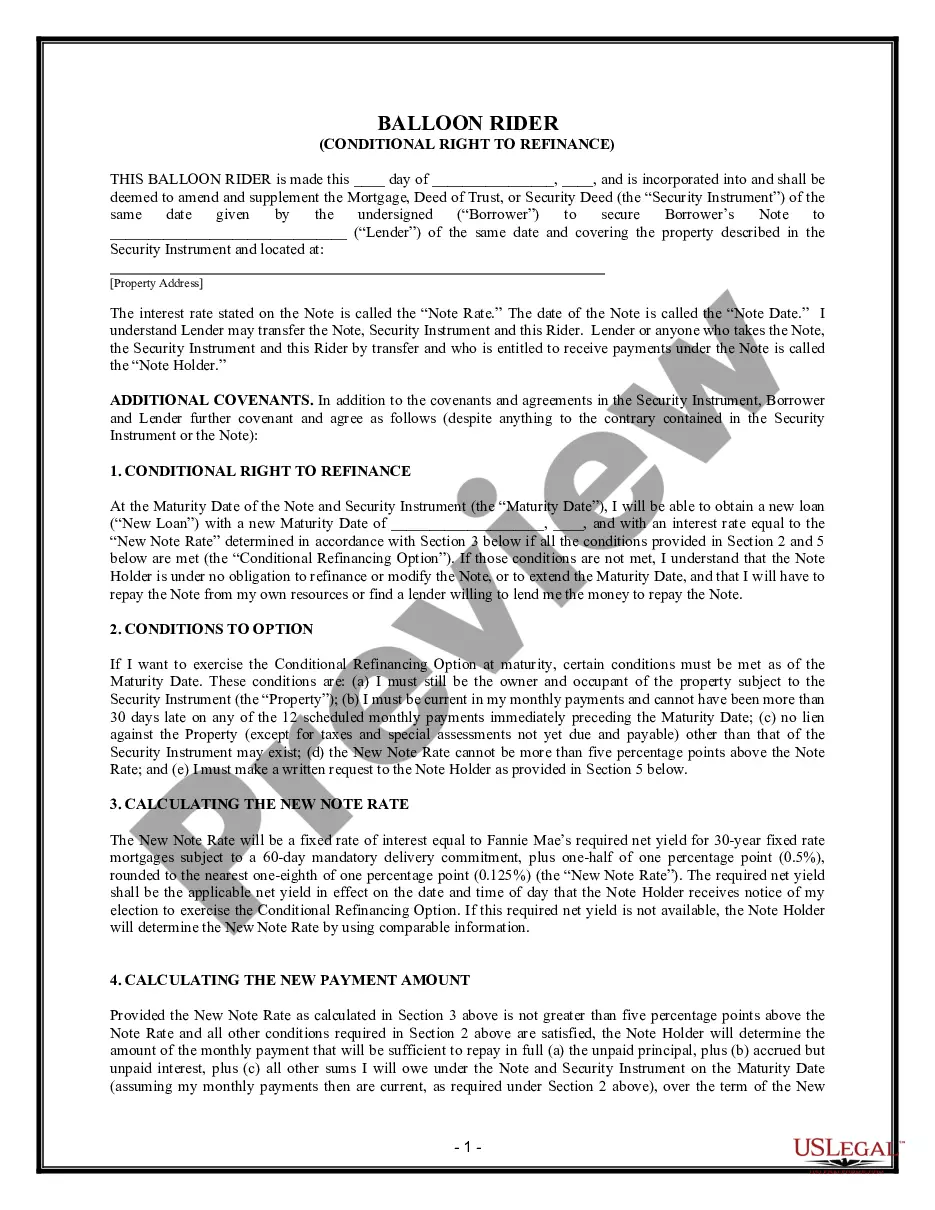

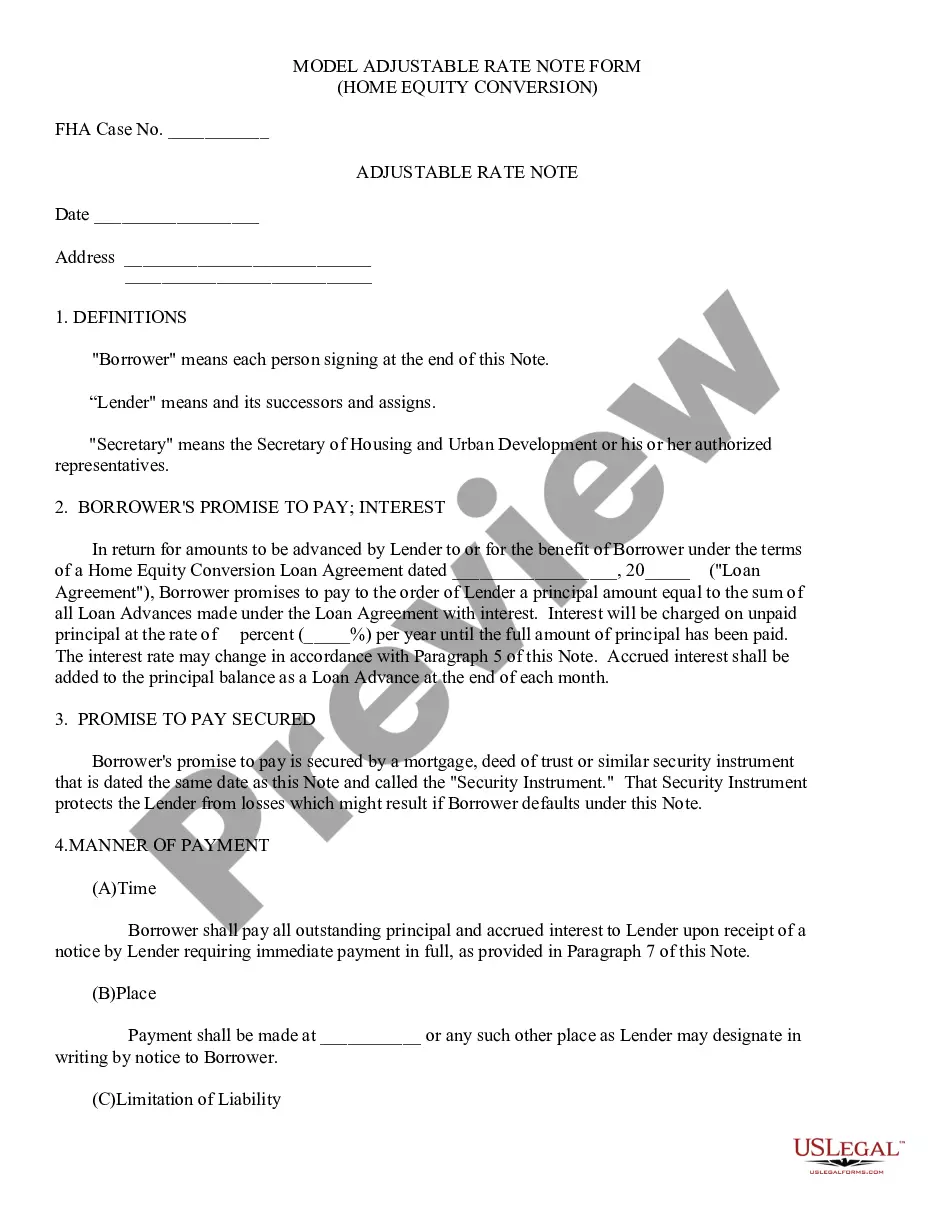

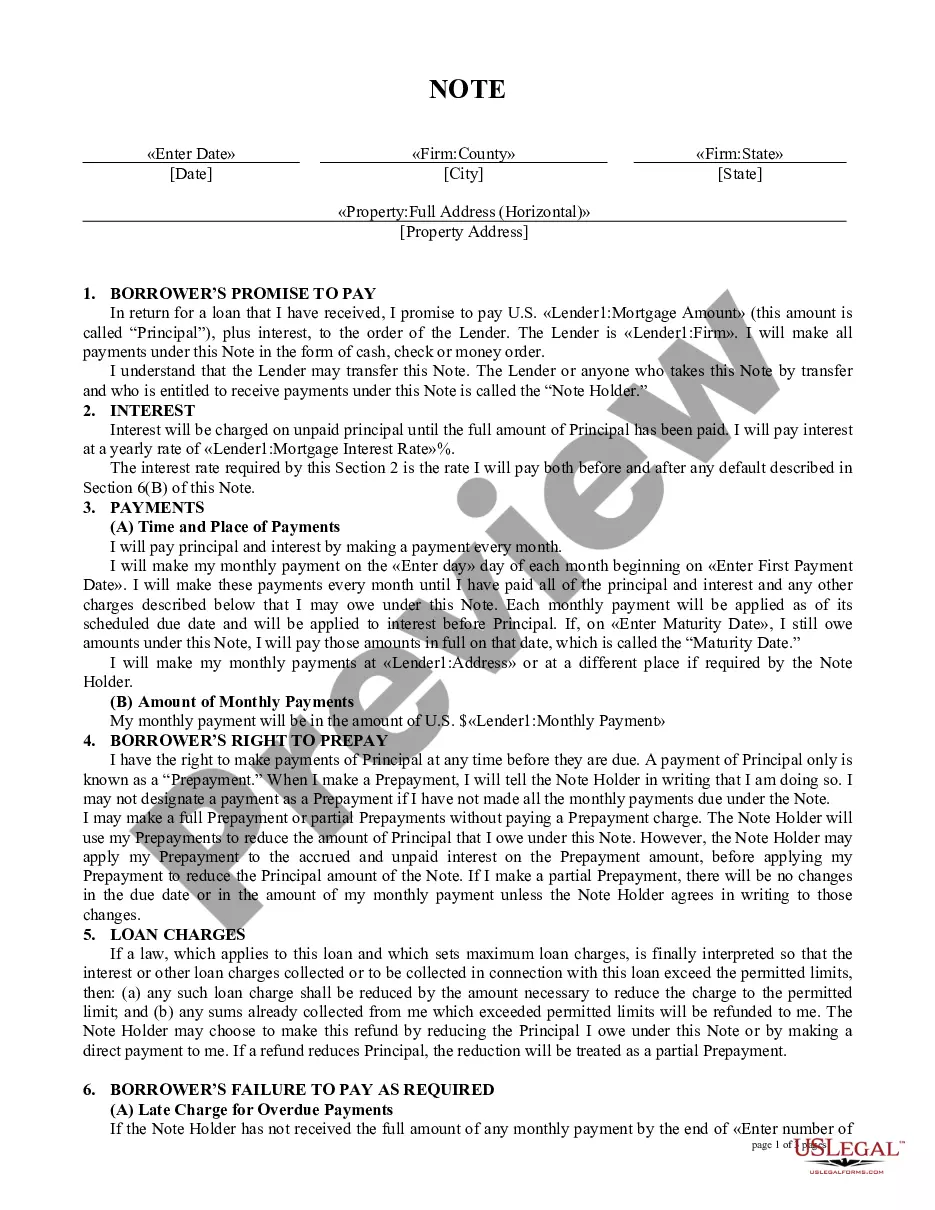

THE NOTE CONTAINS PROVISIONS ALLOWING FOR CHANGES IN THE INTEREST RATE AND THE MONTHLY PAYMENT. THE NOTE LIMITS THE AMOUNT THE BORROWER'S ADJUSTABLE INTEREST RATE CAN CHANGE AT ANY ONE TIME AND THE MINIMUM AND MAXIMUM RATES THE BORROWER MUST PAY.

Adjustable-rate mortgage riders explain that the interest rate on the loan will change on a set date. Condominium riders specify the special terms of condominium ownership, such as the percentage of interest the borrower legally owns in the shared areas, or common elements.

Fixed-rate financing means the interest rate on your loan does not change over the life of your loan. Variable-rate financing is where the interest rate on your loan can change, based on the prime rate or another rate called an index.

An adjustable rate note is a debt instrument with an interest rate that can fluctuate over time. Lenders typically use adjustable rates to compensate for risk and inflation, allowing borrowers to save money on their loan's interest payments.

The margin is the number of percentage points added to the index by the mortgage lender to set your interest rate on an adjustable-rate mortgage (ARM) after the initial rate period ends. The margin is set in your loan agreement and won't change after closing.