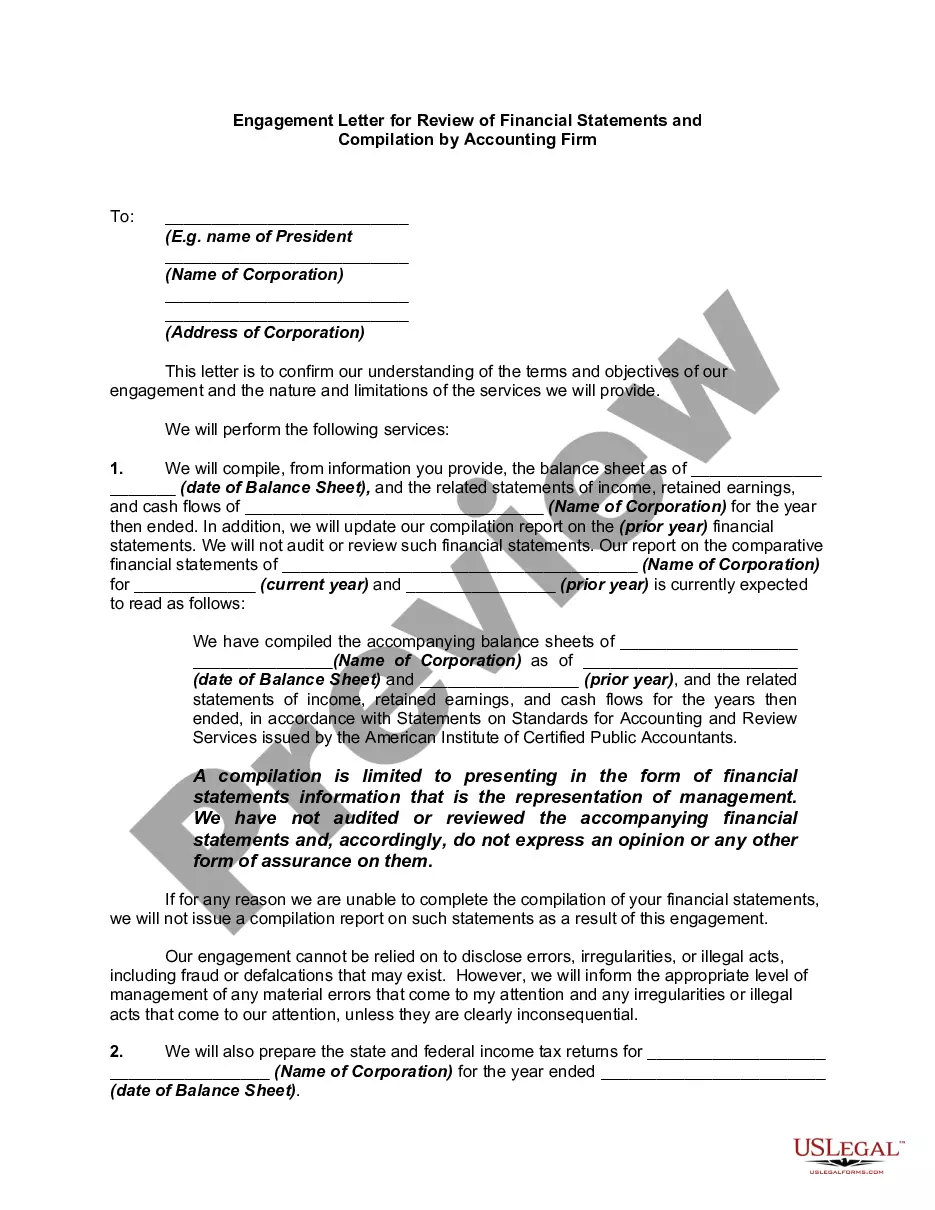

Compiled financial statements represent the most basic level of service that certified public accountants provide with respect to financial statements. In a compilation, the CPA must comply with certain basic requirements of professional standards, such as having a knowledge of the client's industry and applicable accounting principles, having a clear understanding with the client as to the services to be provided, and reading the financial statements to determine whether there are any obvious departures from generally accepted accounting principles (or, in some cases, another comprehensive basis of accounting used by the entity). It may be necessary for the CPA to perform "other accounting services" (such as creating a general ledger for the client, or assisting the client with adjusting entries for the books of the client (before the financial statements can be prepared). Upon completion, a report on the financial statements is issued that states a compilation was performed in accordance with AICPA professional standards, but no assurance is expressed that the statements are in conformity with generally accepted accounting principles. This is known as the expression of "no assurance." Compiled financial statements are often prepared for privately-held entities that do not need a higher level of assurance expressed by the CPA.

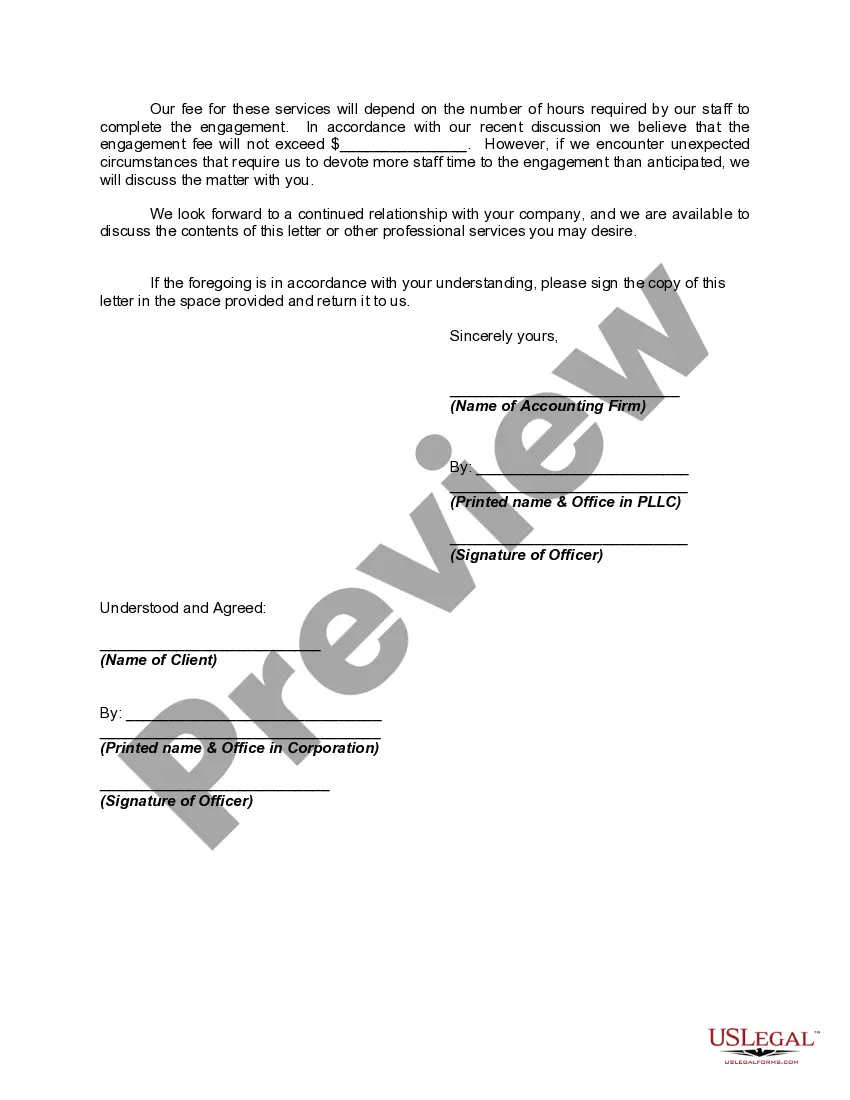

Sacramento California Engagement Letter for Review of Financial Statements and Compilation by Accounting Firm An engagement letter is a formal agreement between a client and an accounting firm that outlines the scope of work, responsibilities, and terms of engagement for a specific financial services task. In Sacramento, California, there are various types of engagement letters related to the review of financial statements and compilation tasks provided by accounting firms. One type of engagement letter is the Engagement Letter for Review of Financial Statements. In this type, the accounting firm agrees to perform a review engagement of the client's financial statements. This involves assessing the statements' presentation and ensuring they conform to Generally Accepted Accounting Principles (GAAP) or other applicable financial reporting frameworks. The accounting firm will perform analytical procedures, make inquiries, and evaluate the evidence obtained during the review process. The engagement letter will outline the timetable, fee structure, and any limitations on liability or involvement in internal business operations. Another type is the Engagement Letter for Compilation of Financial Statements. This engagement letter outlines the accounting firm's agreement to compile, without expressing any assurance or opinion, the financial statements based on information provided by the client. Unlike a review engagement, a compilation engagement does not involve the performance of substantive procedures or independent verification of the data presented. The accounting firm will present the financial statements in an appropriate financial reporting framework and disclose the lack of assurance provided. The Sacramento California Engagement Letter for Review of Financial Statements and Compilation by Accounting Firm typically includes several important elements: 1. Engagement Objective: Clearly states the purpose of engagement, whether it is a review or compilation of financial statements. 2. Responsibilities of the Accounting Firm: Outlines the tasks and procedures the accounting firm will perform to complete the engagement and prepare the financial statements. 3. Responsibilities of the Client: Specifies the client's role, cooperation requirements, and timely provision of accurate and complete financial data and records. 4. Limitations of the Engagement: Describes any limitations on the methodology, scope, or procedures to be followed by the accounting firm. 5. Timetable and Deadlines: Outlines the agreed-upon schedule for completing the engagement, including the submission of financial statements. 6. Fee Structure: States the agreed-upon fee and payment terms for the accounting firm's services. 7. Confidentiality: Specifies the confidentiality obligations of both the accounting firm and the client. 8. Limitations of Liability: Details any limitations of liability on the accounting firm's part, usually addressing instances of negligence or errors. 9. Termination: Outlines the conditions under which either party can terminate the engagement. It is important for both the accounting firm and the client to carefully review and understand the engagement letter before signing it, ensuring mutual compliance with the agreed-upon terms. This helps to establish a clear understanding of expectations, promote effective communication, and mitigate potential conflicts.Sacramento California Engagement Letter for Review of Financial Statements and Compilation by Accounting Firm An engagement letter is a formal agreement between a client and an accounting firm that outlines the scope of work, responsibilities, and terms of engagement for a specific financial services task. In Sacramento, California, there are various types of engagement letters related to the review of financial statements and compilation tasks provided by accounting firms. One type of engagement letter is the Engagement Letter for Review of Financial Statements. In this type, the accounting firm agrees to perform a review engagement of the client's financial statements. This involves assessing the statements' presentation and ensuring they conform to Generally Accepted Accounting Principles (GAAP) or other applicable financial reporting frameworks. The accounting firm will perform analytical procedures, make inquiries, and evaluate the evidence obtained during the review process. The engagement letter will outline the timetable, fee structure, and any limitations on liability or involvement in internal business operations. Another type is the Engagement Letter for Compilation of Financial Statements. This engagement letter outlines the accounting firm's agreement to compile, without expressing any assurance or opinion, the financial statements based on information provided by the client. Unlike a review engagement, a compilation engagement does not involve the performance of substantive procedures or independent verification of the data presented. The accounting firm will present the financial statements in an appropriate financial reporting framework and disclose the lack of assurance provided. The Sacramento California Engagement Letter for Review of Financial Statements and Compilation by Accounting Firm typically includes several important elements: 1. Engagement Objective: Clearly states the purpose of engagement, whether it is a review or compilation of financial statements. 2. Responsibilities of the Accounting Firm: Outlines the tasks and procedures the accounting firm will perform to complete the engagement and prepare the financial statements. 3. Responsibilities of the Client: Specifies the client's role, cooperation requirements, and timely provision of accurate and complete financial data and records. 4. Limitations of the Engagement: Describes any limitations on the methodology, scope, or procedures to be followed by the accounting firm. 5. Timetable and Deadlines: Outlines the agreed-upon schedule for completing the engagement, including the submission of financial statements. 6. Fee Structure: States the agreed-upon fee and payment terms for the accounting firm's services. 7. Confidentiality: Specifies the confidentiality obligations of both the accounting firm and the client. 8. Limitations of Liability: Details any limitations of liability on the accounting firm's part, usually addressing instances of negligence or errors. 9. Termination: Outlines the conditions under which either party can terminate the engagement. It is important for both the accounting firm and the client to carefully review and understand the engagement letter before signing it, ensuring mutual compliance with the agreed-upon terms. This helps to establish a clear understanding of expectations, promote effective communication, and mitigate potential conflicts.