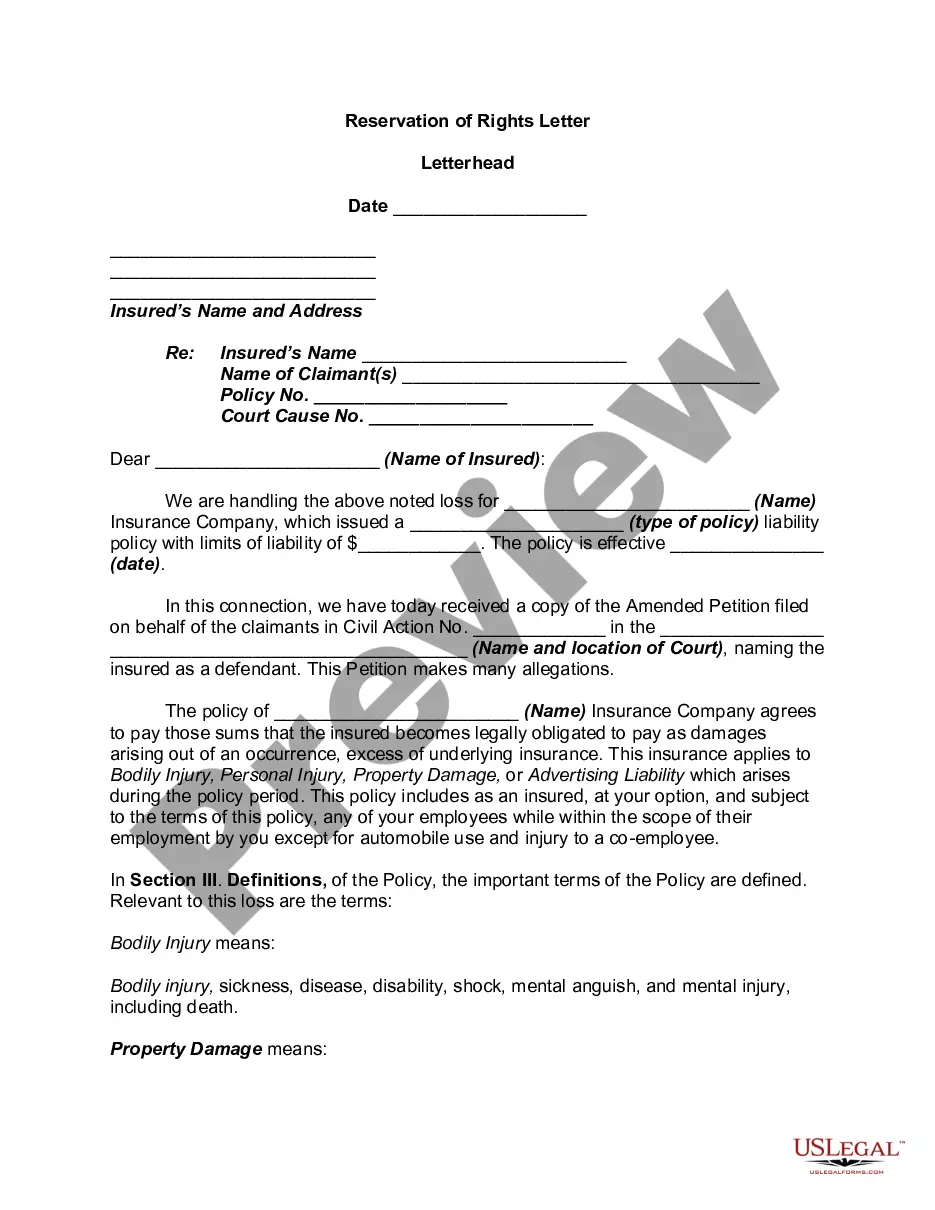

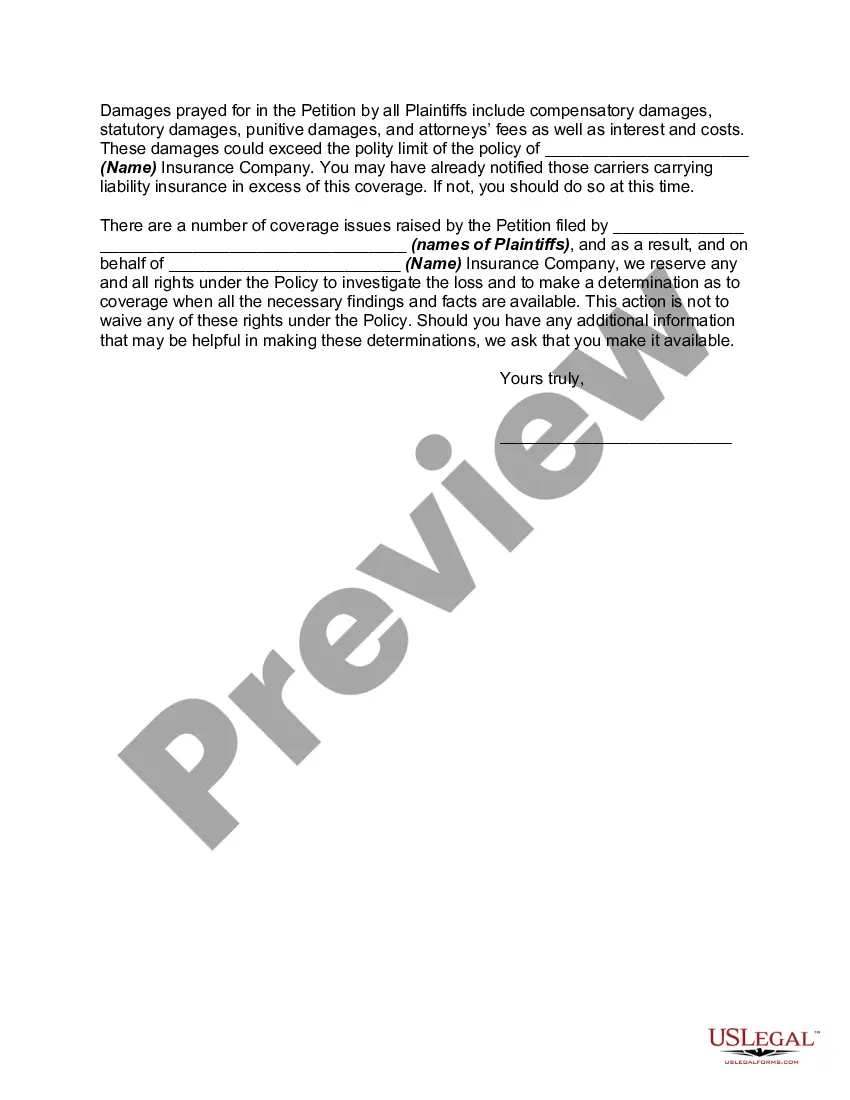

A reservation of rights defense is a means by which a liability insurance carrier agrees to protect and defend its insured against a claim or suit while reserving the right to further evaluate and perhaps even deny coverage for some or all of the claim. It is most commonly used when the claim or suit contains both covered and non-covered allegations, when the allegations are in excess of policy limits, or when the insurer is still investigating its defense and coverage obligations. For the insurer, a reservation of rights provides the flexibility to satisfy its duty to defend without committing to coverage. For the business owner who ultimately may have to pay for an adverse judgment, it requires careful monitoring and attention.

A Collin Texas Reservation of Rights Letter is a legal document that is used to protect the rights of an individual or party involved in a legal dispute in Collin County, Texas. This letter is typically sent by an insurance company to an insured individual or entity, informing them that their liability coverage for a specific claim is being provided under a reservation of rights. The purpose of this letter is to notify the insured party that while the insurance company is providing coverage, they are reserving their right to deny coverage or defend the claim based on certain grounds. It is important to understand that the reservation of rights does not mean that the insurance company has decided to deny coverage or limit their obligations, but rather it allows them to further investigate the claim and potentially deny coverage in the future if certain conditions are met. The Reservation of Rights Letter outlines the specific reasons why the insurance company may deny coverage, such as policy exclusions, breaches of policy conditions, or the insured individual's failure to cooperate with the investigation. It also informs the insured party that they have the right to hire their own legal representation to protect their interests in the claim, as the insurance company's attorney may not have the same interests or priorities. In Collin Texas, there may be different types of Reservation of Rights Letters based on the specific circumstances or types of insurance policies involved in the claim. Some common types may include: 1. Automobile Insurance Reservation of Rights Letter: Sent in cases where the claim involves an automobile accident and the insured party is seeking coverage under an auto insurance policy. 2. Property Insurance Reservation of Rights Letter: Sent when the claim involves damage to or loss of property covered under a property insurance policy, such as homeowner's or renter's insurance. 3. Professional Liability Insurance Reservation of Rights Letter: Used in cases where the claim is related to professional services and the insured party is seeking coverage under a professional liability insurance policy, often referred to as errors and omissions (E&O) insurance. 4. General Liability Insurance Reservation of Rights Letter: Sent when the claim involves bodily injury or property damage caused by the insured party, and coverage is sought under a general liability insurance policy. It's important for recipients of a Collin Texas Reservation of Rights Letter to carefully review the contents, seek legal advice if needed, and respond within the given timeframe. Failure to respond or comply with the specified conditions in the letter may result in a denial of coverage or limitation of the insurance company's obligations.