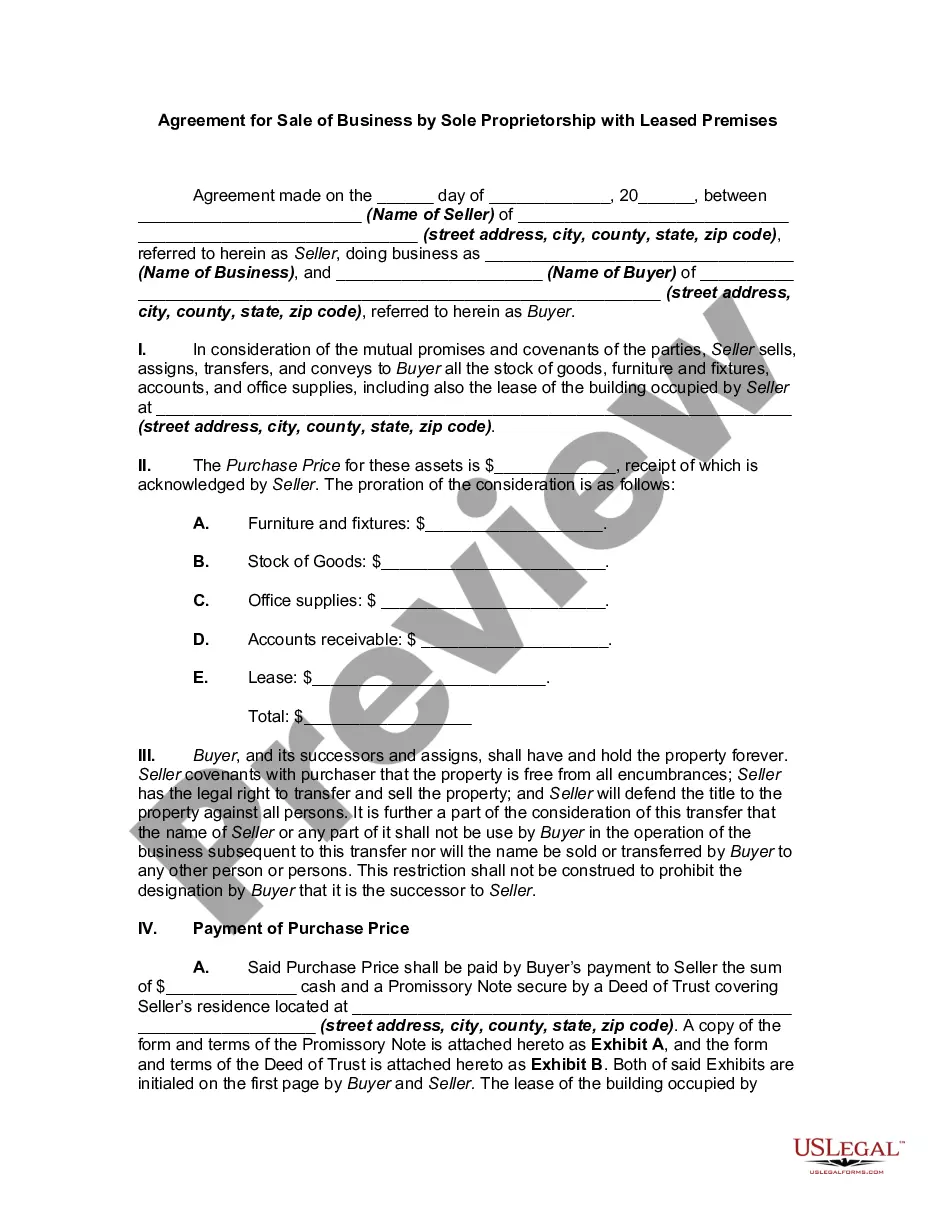

This form involves the sale of a small business where the real estate on which the Business is located is leased from a third party. This form assumes that the Seller has received the right to assign the lease from the lessor/owner.

Los Angeles, California offers a diverse and vibrant business environment, making it an attractive location for entrepreneurs looking to sell their sole proprietorship with leased premises. A well-structured Agreement for Sale of Business by Sole Proprietorship with Leased Premises provides legal protection and outlines the terms and conditions of the transaction. Here, we discuss the key aspects of this agreement, along with its various types based on specific circumstances: 1. Asset Purchase Agreement: This type of agreement focuses on the sale of the sole proprietorship's assets, including tangible assets like inventory, equipment, and intellectual property rights. It specifies the exact assets being transferred and their agreed-upon value. 2. Stock Purchase Agreement: In this agreement, the sole proprietorship's owner sells the company's stocks to the buyer, effectively transferring ownership rights and responsibilities. It highlights the number of shares being sold and any relevant conditions or restrictions. 3. Assignment of Lease: This specific agreement deals with the transfer of leasehold rights from the sole proprietorship to the buyer. It ensures a smooth transition of the lease agreement with the landlord, including the transfer of security deposits, rental terms, and any necessary consents or approvals. 4. Non-Compete Agreement: Often incorporated within the sale agreement, a non-compete clause restricts the seller from engaging in similar business activities within a defined geographic location and timeframe, protecting the buyer's interests and the value of the sold business. Regardless of the specific type, a Los Angeles California Agreement for Sale of Business by Sole Proprietorship with Leased Premises typically includes crucial components such as: a. Parties Involved: Identifying the buyer, seller, and any additional parties involved in the transaction, such as attorneys or brokers. b. Purchase Price and Payment Terms: Stating the agreed-upon sale price, including any down payments, financing arrangements, or installment plans. c. Representations and Warranties: Outlining assurances given by both the seller and buyer regarding the accuracy and completeness of the information provided, including financial statements, tax returns, and legal compliance. d. Conditions Precedent: Specifying any conditions that must be met before the sale can be finalized, such as obtaining necessary permits or licenses, or the completion of due diligence. e. Indemnification: Addressing the allocation of responsibility for any liabilities or claims related to the business operations before or after the sale, protecting both parties from unforeseen risks. f. Confidentiality and Non-Disclosure: Protecting sensitive business information and trade secrets by including clauses preventing the disclosure of proprietary information. g. Governing Law and Dispute Resolution: Determining the jurisdiction whose laws will govern the agreement and outlining the preferred method of resolving any disputes that may arise. It is essential to consult legal professionals experienced in business transactions to tailor the Los Angeles California Agreement for Sale of Business by Sole Proprietorship with Leased Premises to the specific needs and circumstances of the parties involved.