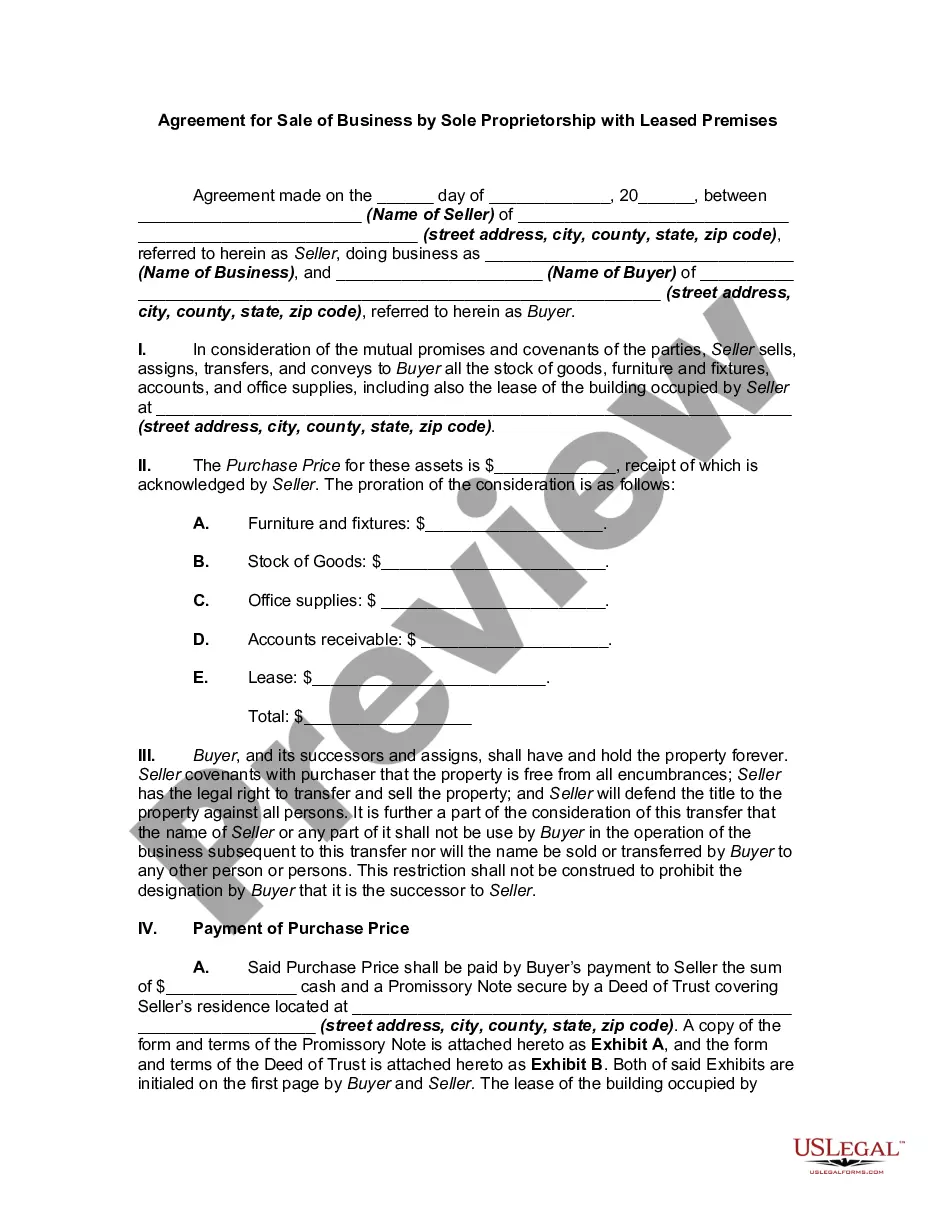

This form involves the sale of a small business where the real estate on which the Business is located is leased from a third party. This form assumes that the Seller has received the right to assign the lease from the lessor/owner.

The Queens New York Agreement for Sale of Business by Sole Proprietorship with Leased Premises is a legal document that outlines the terms and conditions for transferring ownership of a business operated as a sole proprietorship in Queens, New York. It specifically addresses situations where the business is located in leased premises. This agreement encompasses all the essential details involved in the sale, ensuring a smooth and legally binding transaction between the seller (sole proprietor) and the buyer. It provides a comprehensive framework for transferring the business, assets, and liabilities, and includes provisions for the lease of the premises. Keywords: Queens New York, Agreement for Sale of Business, Sole Proprietorship, Leased Premises, Transfer of Ownership, Legal Document, Seller, Buyer, Assets, Liabilities. There can be various types of Queens New York Agreement for Sale of Business by Sole Proprietorship with Leased Premises, some of which include: 1. Asset Purchase Agreement: This type of agreement focuses on the sale and transfer of specific assets of the business. It outlines the items being sold, such as equipment, inventory, intellectual property, customer lists, etc., while also considering the lease of the premises. 2. Stock Purchase Agreement: In this case, the agreement focuses on the sale of the stock or shares of the sole proprietorship. It usually involves the transfer of ownership of the entire business, including all its assets, liabilities, and lease obligations. 3. Assignment and Assumption Agreement: This agreement addresses the assignment of the existing lease from the seller to the buyer. It defines the responsibilities and obligations of each party in regard to the lease agreement, ensuring a smooth transfer of lease rights and obligations. 4. Leaseback Agreement: In certain situations, the sole proprietor might decide to sell the business and simultaneously lease back the premises from the buyer. This agreement outlines the terms of the leaseback, including the rental terms, duration, and any additional provisions related to the continued operation of the business. It is crucial for both the seller and buyer to carefully review and negotiate the terms of the Agreement for Sale of Business by Sole Proprietorship with Leased Premises to ensure that all relevant factors and considerations are addressed, protecting their respective interests and facilitating a successful business transfer.The Queens New York Agreement for Sale of Business by Sole Proprietorship with Leased Premises is a legal document that outlines the terms and conditions for transferring ownership of a business operated as a sole proprietorship in Queens, New York. It specifically addresses situations where the business is located in leased premises. This agreement encompasses all the essential details involved in the sale, ensuring a smooth and legally binding transaction between the seller (sole proprietor) and the buyer. It provides a comprehensive framework for transferring the business, assets, and liabilities, and includes provisions for the lease of the premises. Keywords: Queens New York, Agreement for Sale of Business, Sole Proprietorship, Leased Premises, Transfer of Ownership, Legal Document, Seller, Buyer, Assets, Liabilities. There can be various types of Queens New York Agreement for Sale of Business by Sole Proprietorship with Leased Premises, some of which include: 1. Asset Purchase Agreement: This type of agreement focuses on the sale and transfer of specific assets of the business. It outlines the items being sold, such as equipment, inventory, intellectual property, customer lists, etc., while also considering the lease of the premises. 2. Stock Purchase Agreement: In this case, the agreement focuses on the sale of the stock or shares of the sole proprietorship. It usually involves the transfer of ownership of the entire business, including all its assets, liabilities, and lease obligations. 3. Assignment and Assumption Agreement: This agreement addresses the assignment of the existing lease from the seller to the buyer. It defines the responsibilities and obligations of each party in regard to the lease agreement, ensuring a smooth transfer of lease rights and obligations. 4. Leaseback Agreement: In certain situations, the sole proprietor might decide to sell the business and simultaneously lease back the premises from the buyer. This agreement outlines the terms of the leaseback, including the rental terms, duration, and any additional provisions related to the continued operation of the business. It is crucial for both the seller and buyer to carefully review and negotiate the terms of the Agreement for Sale of Business by Sole Proprietorship with Leased Premises to ensure that all relevant factors and considerations are addressed, protecting their respective interests and facilitating a successful business transfer.