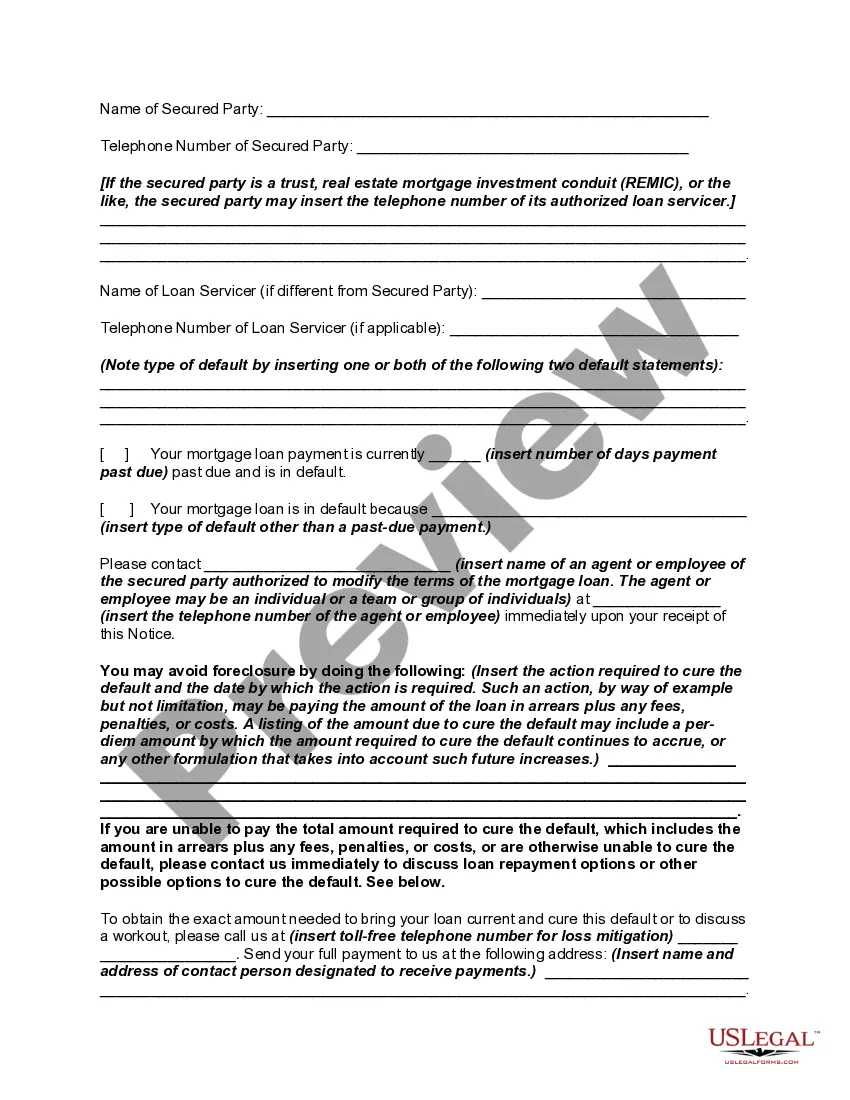

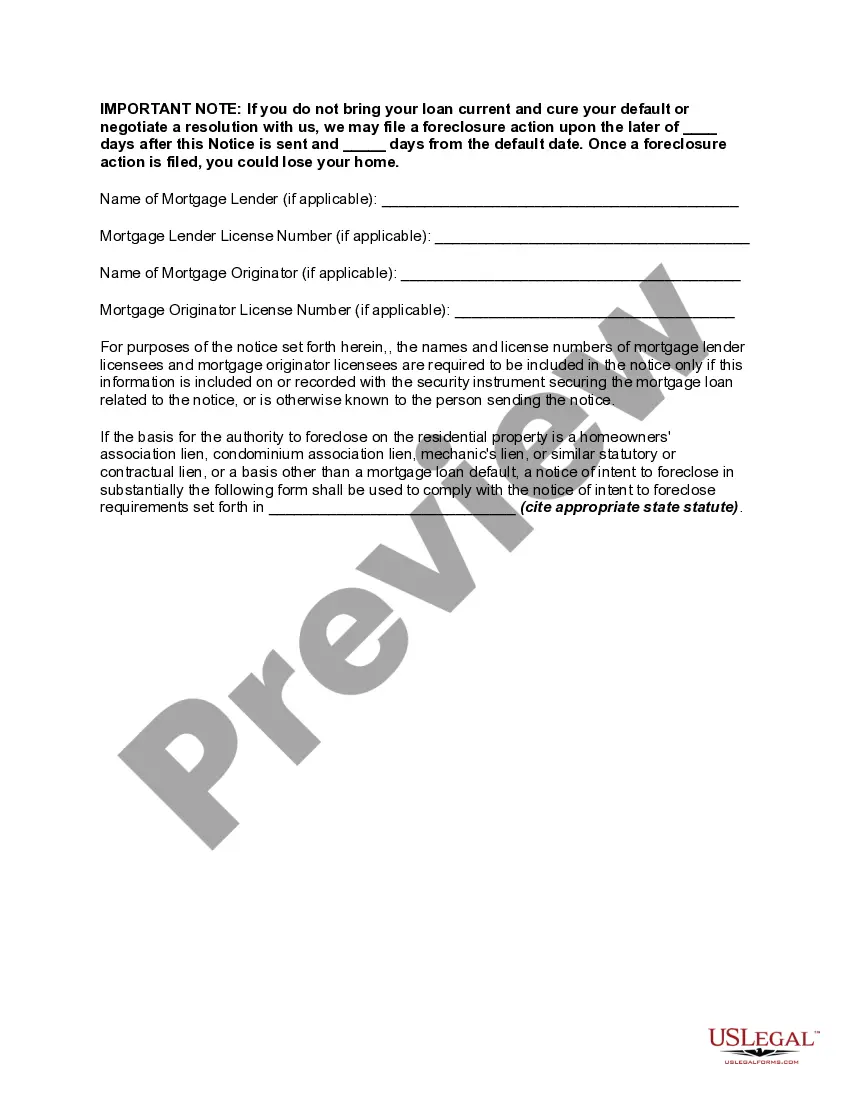

A number of states have enacted measures to facilitate greater communication between borrowers and lenders by requiring mortgage servicers to provide certain notices to defaulted borrowers prior to commencing a foreclosure action. The measures serve a dual purpose, providing more meaningful notice to borrowers of the status of their loans and slowing down the rate of foreclosures within these states. For instance, one state now requires a mortgagee to mail a homeowner a notice of intent to foreclose at least 45 days before initiating a foreclosure action on a loan. The notice must be in writing, and must detail all amounts that are past due and any itemized charges that must be paid to bring the loan current, inform the homeowner that he or she may have options as an alternative to foreclosure, and provide contact information of the servicer, HUD-approved foreclosure counseling agencies, and the state Office of Commissioner of Banks.

1. Understanding Middlesex Massachusetts Notice of Intent to Foreclose — Mortgage Loan Default A Notice of Intent to Foreclose is a legal document issued by the lender to a borrower who has defaulted on their mortgage loan in Middlesex County, Massachusetts. It serves as a warning or a preliminary step before the actual foreclosure process is initiated. When a borrower fails to make mortgage payments for a prolonged period, the lender has the right to take legal action to recover the outstanding debt. In Middlesex County, Massachusetts, the lender is legally required to send a Notice of Intent to Foreclose, notifying the borrower of their default and the consequences that may follow if the payment issues are not resolved promptly. 2. Types of Middlesex Massachusetts Notice of Intent to Foreclose — Mortgage Loan Default There are different types or variations of the Middlesex Massachusetts Notice of Intent to Foreclose — Mortgage Loan Default, depending on specific circumstances or regulations. These variations typically include: a. Pre-Foreclosure Notice: This type of notice is typically sent by the lender to the borrower when they have missed several mortgage payments. It serves as a formal warning, notifying the homeowner that they are in danger of losing their property through foreclosure if the overdue payments are not resolved within a specific period. b. Acceleration Notice: An Acceleration Notice is sent when the lender declares the full loan amount due immediately, rather than allowing the borrower to catch up on missed payments over time. This notice is usually sent after multiple payment defaults and serves as an indication that immediate action is required to resolve the debt. c. Sheriff's Notice of Sale: In cases where the borrower fails to respond to the previous notices and rectify the default, a Sheriff's Notice of Sale may be issued. This notice informs the borrower that the property is scheduled for a foreclosure auction. It specifies the date, time, and location of the sale, providing the borrower with a final opportunity to prevent the foreclosure by paying off the outstanding debt. 3. Dealing with a Middlesex Massachusetts Notice of Intent to Foreclose — Mortgage Loan Default If you receive a Middlesex Massachusetts Notice of Intent to Foreclose — Mortgage Loan Default, it is crucial to act promptly to address the default and prevent foreclosure. Here are important steps to consider: a. Contact the Lender: Reach out to your lender as soon as you receive the notice. Discuss your financial situation, explore possible alternatives, and demonstrate your willingness to resolve the default. b. Seek Legal Assistance: Consult with an experienced foreclosure attorney to better understand your rights and legal options. They can guide you through the process, negotiate with your lender, and potentially help you avoid foreclosure. c. Explore Loan Modification or Refinancing: Investigate whether you qualify for a loan modification or refinancing, which could help you lower your mortgage payments, alter the loan terms, or extend the repayment period. d. Consider Foreclosure Alternatives: If all else fails, explore foreclosure alternatives such as short sales or deeds in lieu of foreclosure. These options can help you mitigate the negative impact on your credit and possibly negotiate a more favorable outcome. Remember, understanding your rights and taking immediate action upon receiving a Notice of Intent to Foreclose can significantly improve your chances of resolving the default and protecting your property. Seek professional guidance and explore all available options to find the best solution for your specific situation.1. Understanding Middlesex Massachusetts Notice of Intent to Foreclose — Mortgage Loan Default A Notice of Intent to Foreclose is a legal document issued by the lender to a borrower who has defaulted on their mortgage loan in Middlesex County, Massachusetts. It serves as a warning or a preliminary step before the actual foreclosure process is initiated. When a borrower fails to make mortgage payments for a prolonged period, the lender has the right to take legal action to recover the outstanding debt. In Middlesex County, Massachusetts, the lender is legally required to send a Notice of Intent to Foreclose, notifying the borrower of their default and the consequences that may follow if the payment issues are not resolved promptly. 2. Types of Middlesex Massachusetts Notice of Intent to Foreclose — Mortgage Loan Default There are different types or variations of the Middlesex Massachusetts Notice of Intent to Foreclose — Mortgage Loan Default, depending on specific circumstances or regulations. These variations typically include: a. Pre-Foreclosure Notice: This type of notice is typically sent by the lender to the borrower when they have missed several mortgage payments. It serves as a formal warning, notifying the homeowner that they are in danger of losing their property through foreclosure if the overdue payments are not resolved within a specific period. b. Acceleration Notice: An Acceleration Notice is sent when the lender declares the full loan amount due immediately, rather than allowing the borrower to catch up on missed payments over time. This notice is usually sent after multiple payment defaults and serves as an indication that immediate action is required to resolve the debt. c. Sheriff's Notice of Sale: In cases where the borrower fails to respond to the previous notices and rectify the default, a Sheriff's Notice of Sale may be issued. This notice informs the borrower that the property is scheduled for a foreclosure auction. It specifies the date, time, and location of the sale, providing the borrower with a final opportunity to prevent the foreclosure by paying off the outstanding debt. 3. Dealing with a Middlesex Massachusetts Notice of Intent to Foreclose — Mortgage Loan Default If you receive a Middlesex Massachusetts Notice of Intent to Foreclose — Mortgage Loan Default, it is crucial to act promptly to address the default and prevent foreclosure. Here are important steps to consider: a. Contact the Lender: Reach out to your lender as soon as you receive the notice. Discuss your financial situation, explore possible alternatives, and demonstrate your willingness to resolve the default. b. Seek Legal Assistance: Consult with an experienced foreclosure attorney to better understand your rights and legal options. They can guide you through the process, negotiate with your lender, and potentially help you avoid foreclosure. c. Explore Loan Modification or Refinancing: Investigate whether you qualify for a loan modification or refinancing, which could help you lower your mortgage payments, alter the loan terms, or extend the repayment period. d. Consider Foreclosure Alternatives: If all else fails, explore foreclosure alternatives such as short sales or deeds in lieu of foreclosure. These options can help you mitigate the negative impact on your credit and possibly negotiate a more favorable outcome. Remember, understanding your rights and taking immediate action upon receiving a Notice of Intent to Foreclose can significantly improve your chances of resolving the default and protecting your property. Seek professional guidance and explore all available options to find the best solution for your specific situation.