Chicago, Illinois Proof of Residency for Mortgage: A Detailed Description When applying for a mortgage in Chicago, Illinois, lenders typically require applicants to provide proof of residency. This important documentation assists in verifying an applicant's identity, ensuring that the mortgage is being granted to a legitimate resident of Chicago. Understanding the various types of proof of residency accepted by lenders in this vibrant city is crucial, so let's delve into them. 1. Chicago Utility Bills: One commonly accepted form of Chicago residency proof is utility bills, such as electricity, water, gas, or sewage bills. These bills should display the homeowner's name, current address, and be issued within the last three or six months, as per the lender's requirements. 2. Rental or Lease Agreement: For those residing in rental properties within Chicago, submitting a valid and current rental or lease agreement could serve as proof of residency. This document should include the lessee's name, address, the landlord's contact information, and the lease term. 3. Driver's License: A Chicago-issued driver's license is another valid document to confirm residency for mortgage purposes. The license must be unexpired and present the homeowner's current address within Chicago. 4. State ID Card: In the absence of a driver's license, a state-issued identification card, which includes the homeowner's name and address, can serve as proof of residency. The ID card should be current and unexpired. 5. Real Estate Tax Bill: Homeowners could provide a recent real estate tax bill reflecting their Chicago address. This document not only verifies residency but also helps lenders understand the homeowner's tax obligations. 6. Voter Registration Card: A Chicago voter registration card with the homeowner's current address is often accepted as proof of residency. This document is particularly helpful if the homeowner has recently relocated and is new to Chicago. 7. Bank Statements: Lenders may accept recent bank statements that display the homeowner's name and address as proof of residency. These statements, typically covering the previous three to six months, confirm that the applicant maintains an active bank account within Chicago. It is important to note that different lenders may have varying requirements for proof of residency for mortgages in Chicago, Illinois. Consulting with the specific lending institution or mortgage broker is crucial to ensure compliance with their guidelines. In conclusion, when applying for a mortgage in Chicago, Illinois, homeowners need to provide various forms of proof of residency to validate their status as residents. Acceptable documents include Chicago utility bills, rental or lease agreements, driver's licenses, state identification cards, real estate tax bills, voter registration cards, and bank statements. Ensuring that all necessary documents are up to date and meet the lender's specific requirements will expedite the mortgage application process.

Chicago Illinois Proof of Residency for Mortgage

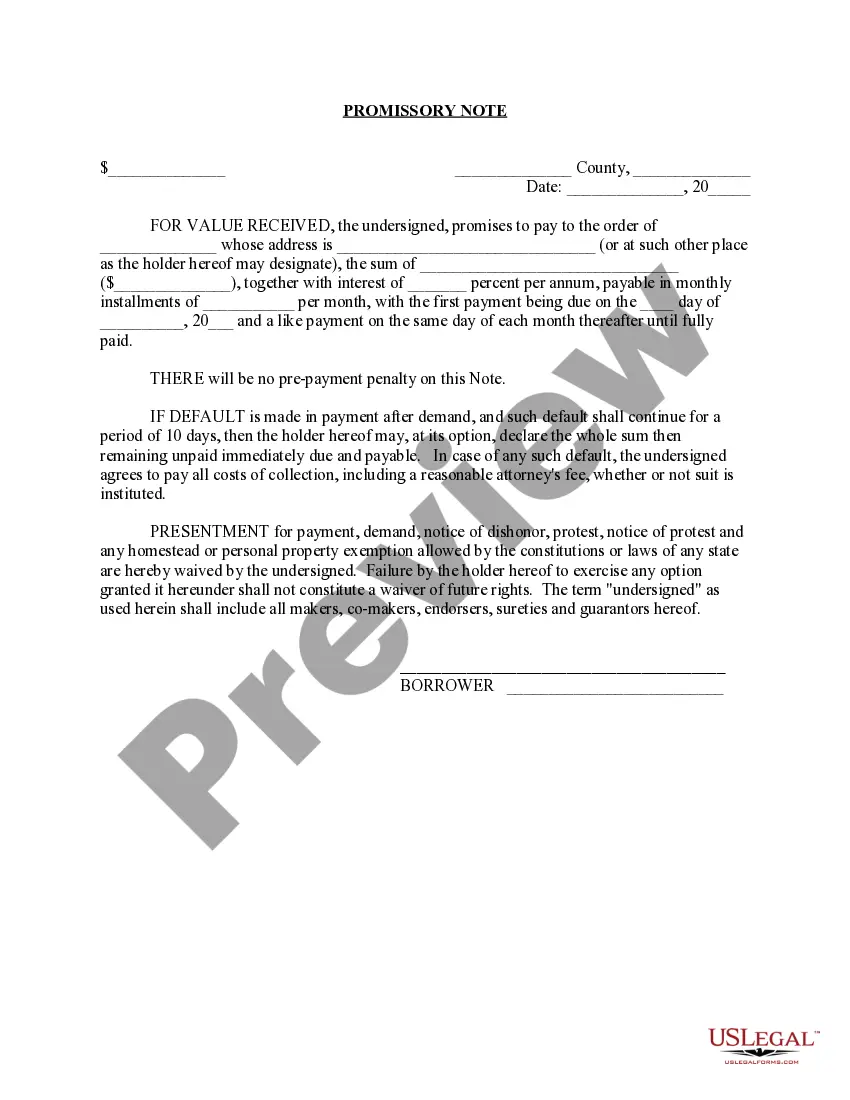

Description

How to fill out Chicago Illinois Proof Of Residency For Mortgage?

Do you need to quickly draft a legally-binding Chicago Proof of Residency for Mortgage or probably any other document to take control of your personal or business affairs? You can go with two options: contact a legal advisor to write a valid paper for you or draft it entirely on your own. Luckily, there's another option - US Legal Forms. It will help you receive neatly written legal documents without paying sky-high fees for legal services.

US Legal Forms offers a rich collection of over 85,000 state-compliant document templates, including Chicago Proof of Residency for Mortgage and form packages. We offer documents for an array of life circumstances: from divorce paperwork to real estate documents. We've been on the market for more than 25 years and got a spotless reputation among our customers. Here's how you can become one of them and get the necessary document without extra hassles.

- To start with, double-check if the Chicago Proof of Residency for Mortgage is adapted to your state's or county's laws.

- If the document has a desciption, make sure to verify what it's suitable for.

- Start the searching process again if the document isn’t what you were seeking by using the search box in the header.

- Choose the plan that best suits your needs and proceed to the payment.

- Select the file format you would like to get your document in and download it.

- Print it out, complete it, and sign on the dotted line.

If you've already registered an account, you can easily log in to it, locate the Chicago Proof of Residency for Mortgage template, and download it. To re-download the form, simply head to the My Forms tab.

It's easy to buy and download legal forms if you use our catalog. Moreover, the templates we provide are updated by industry experts, which gives you greater confidence when writing legal affairs. Try US Legal Forms now and see for yourself!