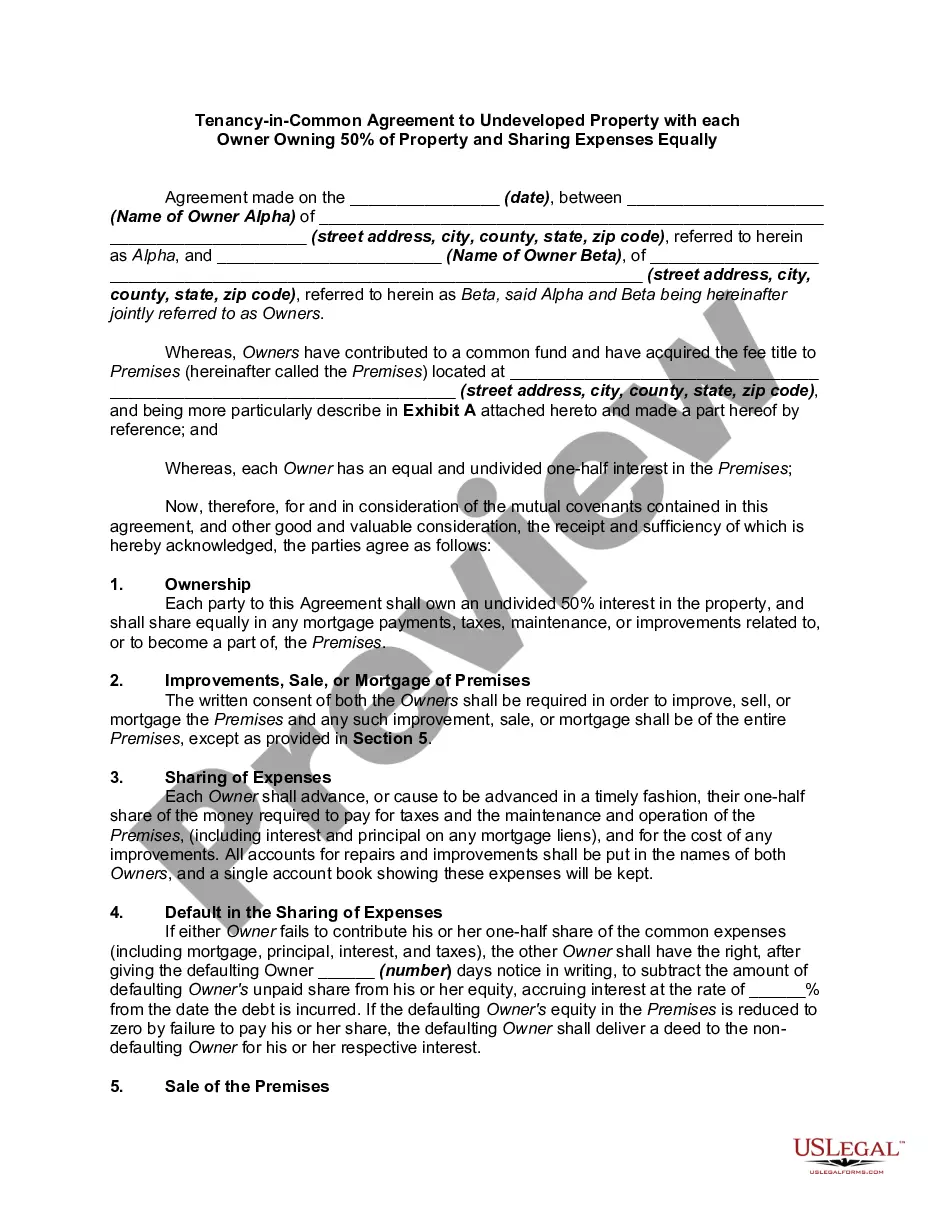

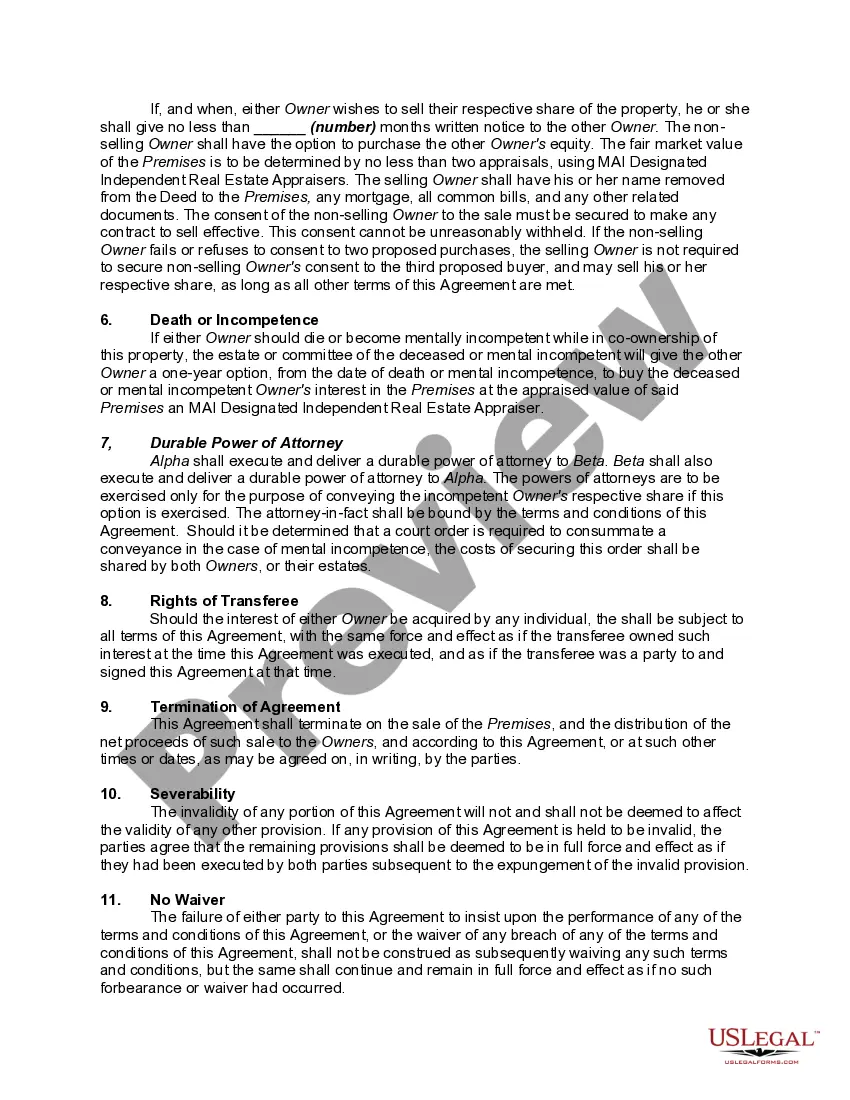

Tenants in common hold title to real or personal property so that each has an "undivided interest" in the property and all have an equal right to use the property. Tenants in common each own a portion of the property, which may be unequal, but have the right to possess the entire property.

There is no "right of survivorship" if one of the tenants in common dies, and each interest may be separately sold, mortgaged or willed to another. A tenancy in common interest is distinguished from a joint tenancy interest, which passes automatically to the survivor. Upon the death of a tenant in common there must be a court supervised administration of the estate of the deceased to transfer the interest in the tenancy in common.

This form is a generic example that may be referred to when preparing such a form for your particular state. It is for illustrative purposes only. Local laws should be consulted to determine any specific requirements for such a form in a particular jurisdiction.

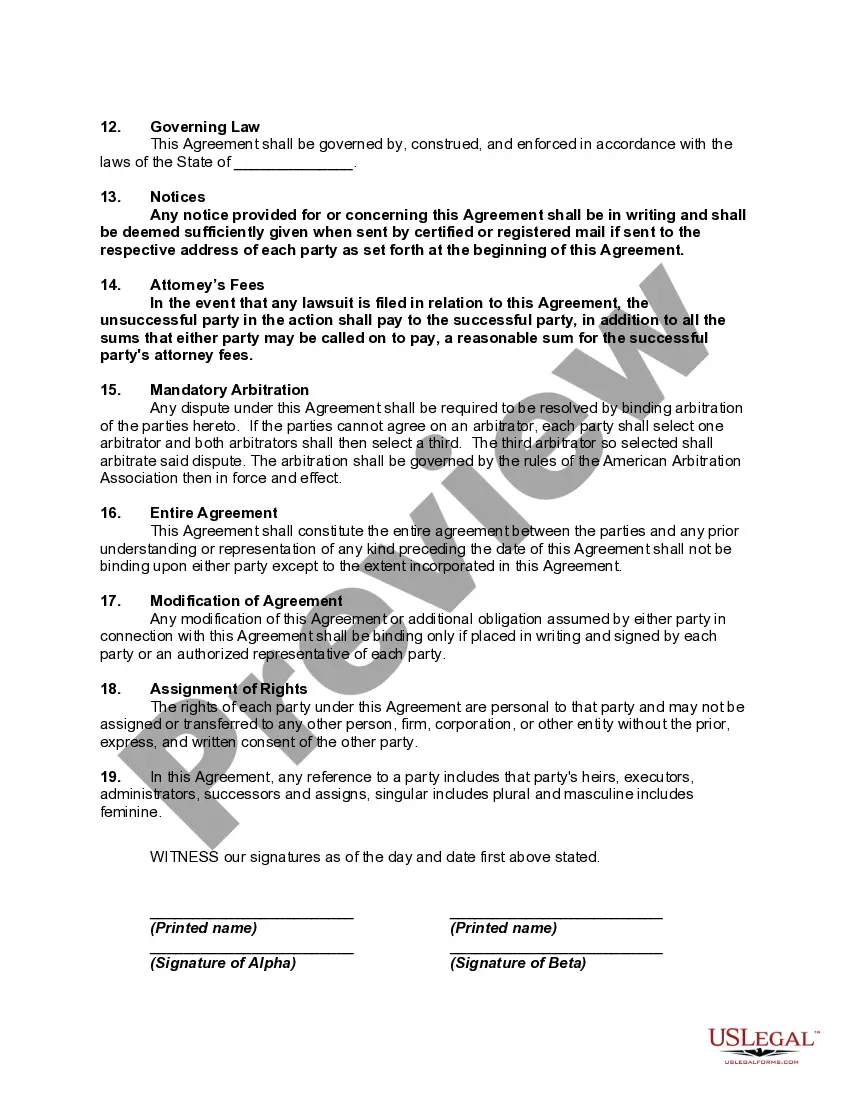

A Fairfax Virginia Tenancy-in-Common Agreement to Undeveloped Property with each Owner Owning Fifty Percent of Property and Sharing Expenses Equally is a legal document that outlines the rights and responsibilities of multiple owners of an undeveloped property in Fairfax, Virginia. This type of agreement is commonly used when two or more individuals or entities decide to jointly own and share the expenses associated with an undeveloped property. In this arrangement, each owner holds a fifty percent ownership interest in the property, granting them equal rights and benefits. This can include the right to access and use the property, the right to make improvements or changes, and the right to enjoy any financial gains or losses resulting from any future development or sale. The agreement also outlines the equitable division of expenses among the co-owners. This typically includes costs related to property maintenance, taxes, insurance, and any other shared expenses necessary to keep the property in good condition. By distributing the expenses equally, the agreement ensures fairness and prevents disputes that may arise due to differing financial capabilities or investment interests. Furthermore, the agreement may address various aspects of property management and decision-making processes. It can discuss procedures for making unanimous or majority decisions regarding the property, setting limitations on individual owner's actions that may impact the property, and specifying any restrictions or conditions on the potential development or use of the land. Different types of Fairfax Virginia Tenancy-in-Common Agreements to Undeveloped Property with each Owner Owning Fifty Percent of Property and Sharing Expenses Equally may vary based on specific clauses and provisions included. For example, some agreements might include a buyout clause, allowing one owner to buy out the other's share of the property under certain circumstances. Other types of agreements may include stipulations on the permitted uses of the property, such as restrictions on construction or commercial activities. In summary, a Fairfax Virginia Tenancy-in-Common Agreement to Undeveloped Property with each Owner Owning Fifty Percent of Property and Sharing Expenses Equally is a legal document that establishes the rights, responsibilities, and financial obligations of co-owners of an undeveloped property. It ensures fair distribution of expenses and outlines procedures for decision-making and property management. These agreements may have different variations and additional provisions based on the specific needs and preferences of the co-owners.A Fairfax Virginia Tenancy-in-Common Agreement to Undeveloped Property with each Owner Owning Fifty Percent of Property and Sharing Expenses Equally is a legal document that outlines the rights and responsibilities of multiple owners of an undeveloped property in Fairfax, Virginia. This type of agreement is commonly used when two or more individuals or entities decide to jointly own and share the expenses associated with an undeveloped property. In this arrangement, each owner holds a fifty percent ownership interest in the property, granting them equal rights and benefits. This can include the right to access and use the property, the right to make improvements or changes, and the right to enjoy any financial gains or losses resulting from any future development or sale. The agreement also outlines the equitable division of expenses among the co-owners. This typically includes costs related to property maintenance, taxes, insurance, and any other shared expenses necessary to keep the property in good condition. By distributing the expenses equally, the agreement ensures fairness and prevents disputes that may arise due to differing financial capabilities or investment interests. Furthermore, the agreement may address various aspects of property management and decision-making processes. It can discuss procedures for making unanimous or majority decisions regarding the property, setting limitations on individual owner's actions that may impact the property, and specifying any restrictions or conditions on the potential development or use of the land. Different types of Fairfax Virginia Tenancy-in-Common Agreements to Undeveloped Property with each Owner Owning Fifty Percent of Property and Sharing Expenses Equally may vary based on specific clauses and provisions included. For example, some agreements might include a buyout clause, allowing one owner to buy out the other's share of the property under certain circumstances. Other types of agreements may include stipulations on the permitted uses of the property, such as restrictions on construction or commercial activities. In summary, a Fairfax Virginia Tenancy-in-Common Agreement to Undeveloped Property with each Owner Owning Fifty Percent of Property and Sharing Expenses Equally is a legal document that establishes the rights, responsibilities, and financial obligations of co-owners of an undeveloped property. It ensures fair distribution of expenses and outlines procedures for decision-making and property management. These agreements may have different variations and additional provisions based on the specific needs and preferences of the co-owners.