Tenants in common hold title to real or personal property so that each has an "undivided interest" in the property and all have an equal right to use the property. Tenants in common each own a portion of the property, which may be unequal, but have the right to possess the entire property.

There is no "right of survivorship" if one of the tenants in common dies, and each interest may be separately sold, mortgaged or willed to another. A tenancy in common interest is distinguished from a joint tenancy interest, which passes automatically to the survivor. Upon the death of a tenant in common there must be a court supervised administration of the estate of the deceased to transfer the interest in the tenancy in common.

This form is a generic example that may be referred to when preparing such a form for your particular state. It is for illustrative purposes only. Local laws should be consulted to determine any specific requirements for such a form in a particular jurisdiction.

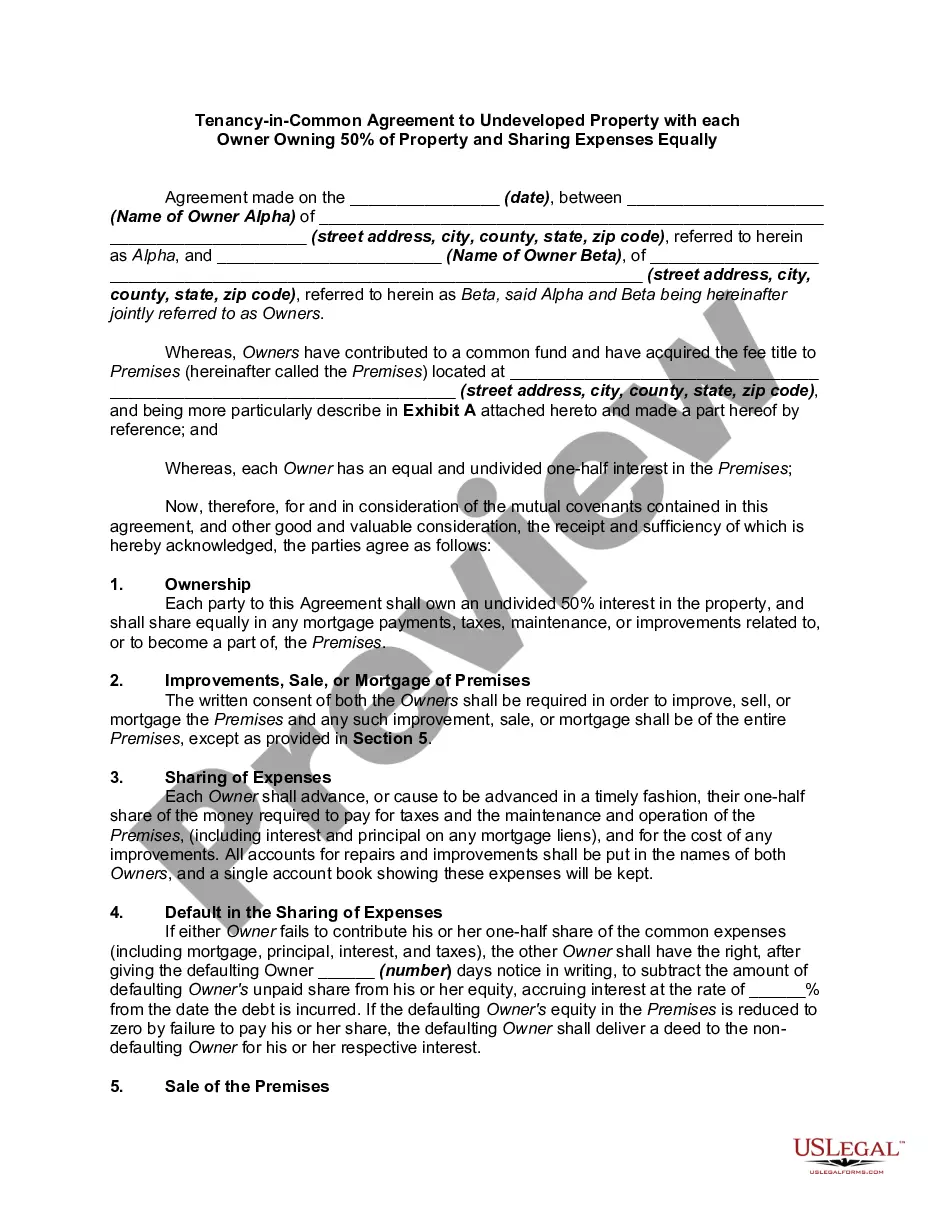

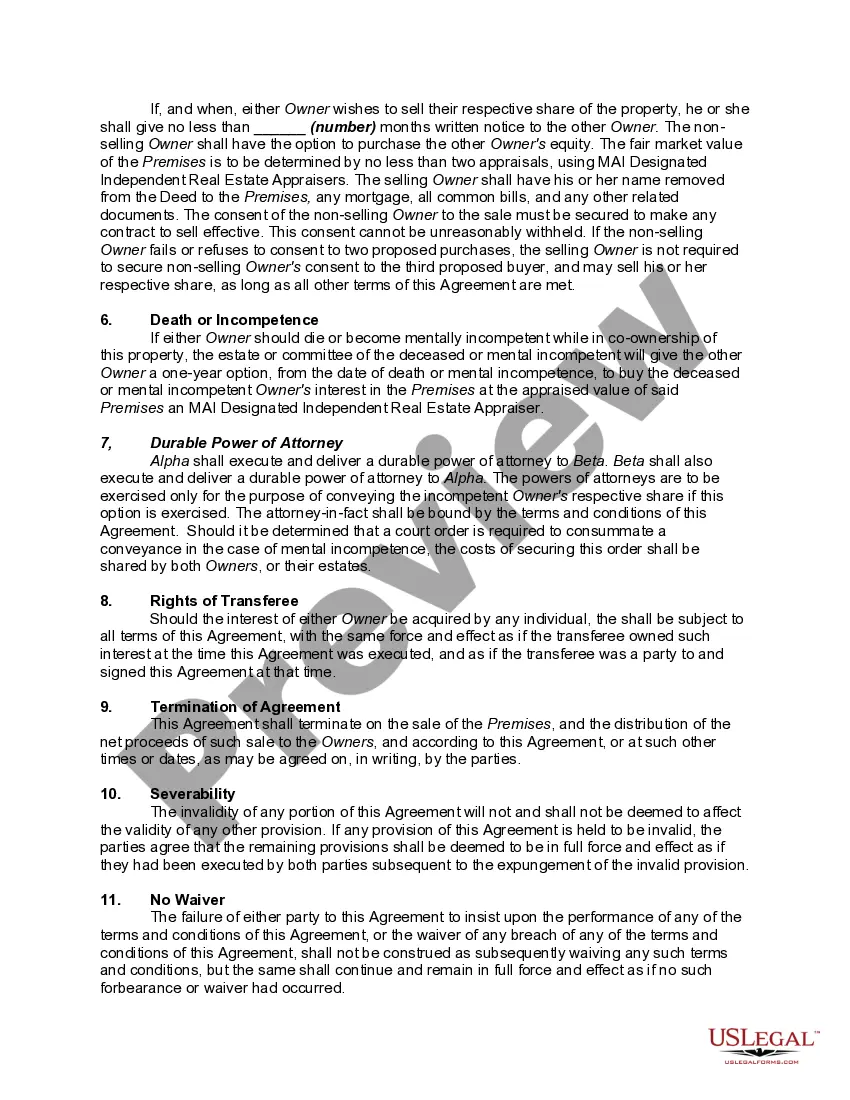

A Nassau New York Tenancy-in-Common Agreement to Undeveloped Property with each Owner Owning Fifty Percent of Property and Sharing Expenses Equally is a legal document that outlines the rights and responsibilities of multiple owners who jointly own a piece of undeveloped property in Nassau County, New York. In this agreement, each owner has an equal ownership share, usually fifty percent, and is responsible for sharing the expenses associated with maintaining and managing the property equally. This type of tenancy-in-common agreement is commonly used when multiple individuals or entities wish to invest in undeveloped property together while maintaining individual ownership rights. The agreement provides clarity and establishes rules for the co-owners to follow, ensuring a fair and organized approach to the property's ownership and its associated expenses. The Nassau New York Tenancy-in-Common Agreement to Undeveloped Property with each Owner Owning Fifty Percent of Property and Sharing Expenses Equally may also come in different variations or versions based on specific factors or requirements. Some possible variations may include: 1. Limited Partnership Agreement: This agreement may be used when the owners form a limited partnership to jointly own and manage the undeveloped property. It outlines the roles and responsibilities of the general partners and limited partners, with each partner still owning fifty percent and sharing expenses equally. 2. Co-Ownership Agreement with Development Plan: In some cases, the owners of the undeveloped property may have a common development plan in mind. This agreement may lay out the specific plans, timelines, and responsibilities for each owner regarding the development of the property, while still maintaining an equal ownership share and equal sharing of expenses. 3. Agreement with Buyout Option: This agreement may offer an option for one owner to buy out the other owner's share in the future. It outlines the terms and conditions under which a buyout can occur, including the valuation of the property and the process for executing the buyout, while still maintaining an equal ownership share and equal sharing of expenses until a buyout takes place. In summary, a Nassau New York Tenancy-in-Common Agreement to Undeveloped Property with each Owner Owning Fifty Percent of Property and Sharing Expenses Equally is a legally binding document that ensures a fair and organized approach to co-owning and managing undeveloped property. Different versions or variations of this agreement may exist to cater to specific needs or preferences of the co-owners.A Nassau New York Tenancy-in-Common Agreement to Undeveloped Property with each Owner Owning Fifty Percent of Property and Sharing Expenses Equally is a legal document that outlines the rights and responsibilities of multiple owners who jointly own a piece of undeveloped property in Nassau County, New York. In this agreement, each owner has an equal ownership share, usually fifty percent, and is responsible for sharing the expenses associated with maintaining and managing the property equally. This type of tenancy-in-common agreement is commonly used when multiple individuals or entities wish to invest in undeveloped property together while maintaining individual ownership rights. The agreement provides clarity and establishes rules for the co-owners to follow, ensuring a fair and organized approach to the property's ownership and its associated expenses. The Nassau New York Tenancy-in-Common Agreement to Undeveloped Property with each Owner Owning Fifty Percent of Property and Sharing Expenses Equally may also come in different variations or versions based on specific factors or requirements. Some possible variations may include: 1. Limited Partnership Agreement: This agreement may be used when the owners form a limited partnership to jointly own and manage the undeveloped property. It outlines the roles and responsibilities of the general partners and limited partners, with each partner still owning fifty percent and sharing expenses equally. 2. Co-Ownership Agreement with Development Plan: In some cases, the owners of the undeveloped property may have a common development plan in mind. This agreement may lay out the specific plans, timelines, and responsibilities for each owner regarding the development of the property, while still maintaining an equal ownership share and equal sharing of expenses. 3. Agreement with Buyout Option: This agreement may offer an option for one owner to buy out the other owner's share in the future. It outlines the terms and conditions under which a buyout can occur, including the valuation of the property and the process for executing the buyout, while still maintaining an equal ownership share and equal sharing of expenses until a buyout takes place. In summary, a Nassau New York Tenancy-in-Common Agreement to Undeveloped Property with each Owner Owning Fifty Percent of Property and Sharing Expenses Equally is a legally binding document that ensures a fair and organized approach to co-owning and managing undeveloped property. Different versions or variations of this agreement may exist to cater to specific needs or preferences of the co-owners.