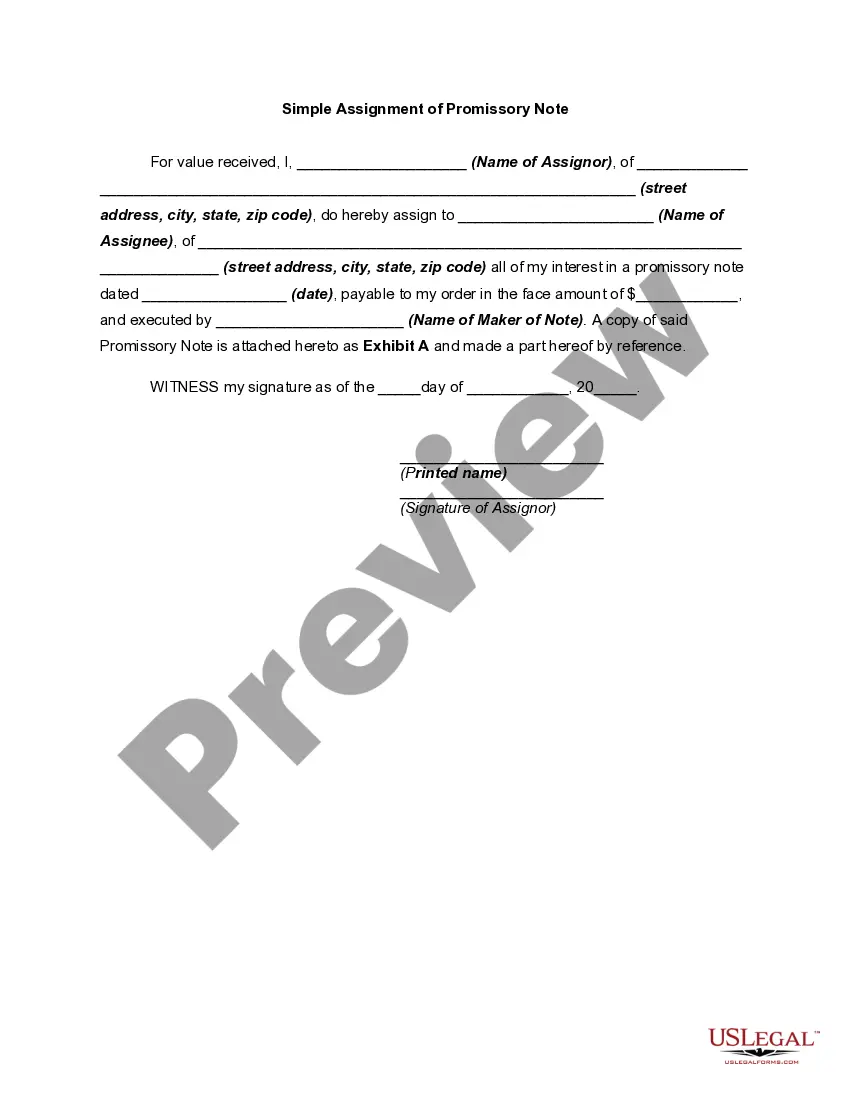

Mecklenburg North Carolina Simple Promissory Note for Personal Loan: A Comprehensive Guide Introduction: In Mecklenburg County, North Carolina, a simple promissory note is a legally binding document that establishes a formal agreement between a borrower and a lender for a personal loan. This note clearly outlines the terms and conditions, repayment schedule, interest rate, and consequences of defaulting on the loan. Understanding the intricacies of this note is essential for both borrowers and lenders in Mecklenburg County. Key Information in Mecklenburg North Carolina Simple Promissory Note: 1. Parties Involved: The promissory note identifies the lender (also known as the payee) and the borrower (also known as the maker or mayor). 2. Loan Amount: The note specifies the principal amount the borrower agrees to repay to the lender. 3. Interest Rate: The document highlights the interest rate that the borrower will pay on the loan, stated as an annual percentage rate (APR). 4. Repayment Terms: The note outlines the length of the loan and the repayment schedule, including the frequency of payments (monthly, bi-monthly, etc.). 5. Late Fees: It may also include details about late payment penalties, specifying the amount or percentage to be charged when payments are overdue. 6. Default and Legal Actions: The note outlines the consequences and legal remedies available to the lender if the borrower defaults on the loan. 7. Collateral: If applicable, the note can include information about any collateral provided by the borrower to secure the loan. Types of Mecklenburg North Carolina Simple Promissory Notes for Personal Loans: 1. Secured Promissory Note: This type of note involves the borrower providing collateral, such as real estate or valuable assets, to secure the loan. If the borrower fails to repay, the lender can seize the collateral as specified in the note. 2. Unsecured Promissory Note: In contrast to a secured note, the unsecured promissory note does not require any collateral. In this case, the lender relies solely on the borrower's creditworthiness and trust. 3. Fixed-Rate Promissory Note: This type of note establishes a fixed interest rate that remains constant throughout the loan term. Borrowers find it easier to plan their finances as they know the exact interest amount they will pay. 4. Variable-Rate Promissory Note: These notes, also known as adjustable-rate notes, come with an interest rate that fluctuates over time. Typically, the interest rate is tied to a benchmark, such as the Prime Rate or LIBOR, and changes periodically as specified in the note. 5. Demand Promissory Note: Unlike other promissory notes that have a specific loan term, a demand note allows the lender to request repayment in full at any time. However, the borrower is usually given a predetermined notice period to comply. Conclusion: In Mecklenburg County, North Carolina, a simple promissory note for personal loans establishes the legal framework for borrowers and lenders. Whether it's a secured or unsecured note, issued with a fixed or variable interest rate, or even a demand note, understanding the terms and conditions laid out in the note is crucial for all parties involved. It ensures transparency, helps borrowers make informed decisions, and protects lenders' rights in case of default or non-payment.

Mecklenburg North Carolina Simple Promissory Note for Personal Loan

Description

How to fill out Mecklenburg North Carolina Simple Promissory Note For Personal Loan?

Laws and regulations in every area differ from state to state. If you're not an attorney, it's easy to get lost in a variety of norms when it comes to drafting legal documents. To avoid expensive legal assistance when preparing the Mecklenburg Simple Promissory Note for Personal Loan, you need a verified template legitimate for your region. That's when using the US Legal Forms platform is so helpful.

US Legal Forms is a trusted by millions web collection of more than 85,000 state-specific legal forms. It's an excellent solution for professionals and individuals looking for do-it-yourself templates for various life and business situations. All the forms can be used many times: once you obtain a sample, it remains available in your profile for further use. Therefore, when you have an account with a valid subscription, you can simply log in and re-download the Mecklenburg Simple Promissory Note for Personal Loan from the My Forms tab.

For new users, it's necessary to make a few more steps to get the Mecklenburg Simple Promissory Note for Personal Loan:

- Analyze the page content to make sure you found the correct sample.

- Take advantage of the Preview option or read the form description if available.

- Look for another doc if there are inconsistencies with any of your criteria.

- Click on the Buy Now button to obtain the document when you find the correct one.

- Choose one of the subscription plans and log in or create an account.

- Choose how you prefer to pay for your subscription (with a credit card or PayPal).

- Pick the format you want to save the file in and click Download.

- Fill out and sign the document on paper after printing it or do it all electronically.

That's the easiest and most affordable way to get up-to-date templates for any legal scenarios. Find them all in clicks and keep your documentation in order with the US Legal Forms!