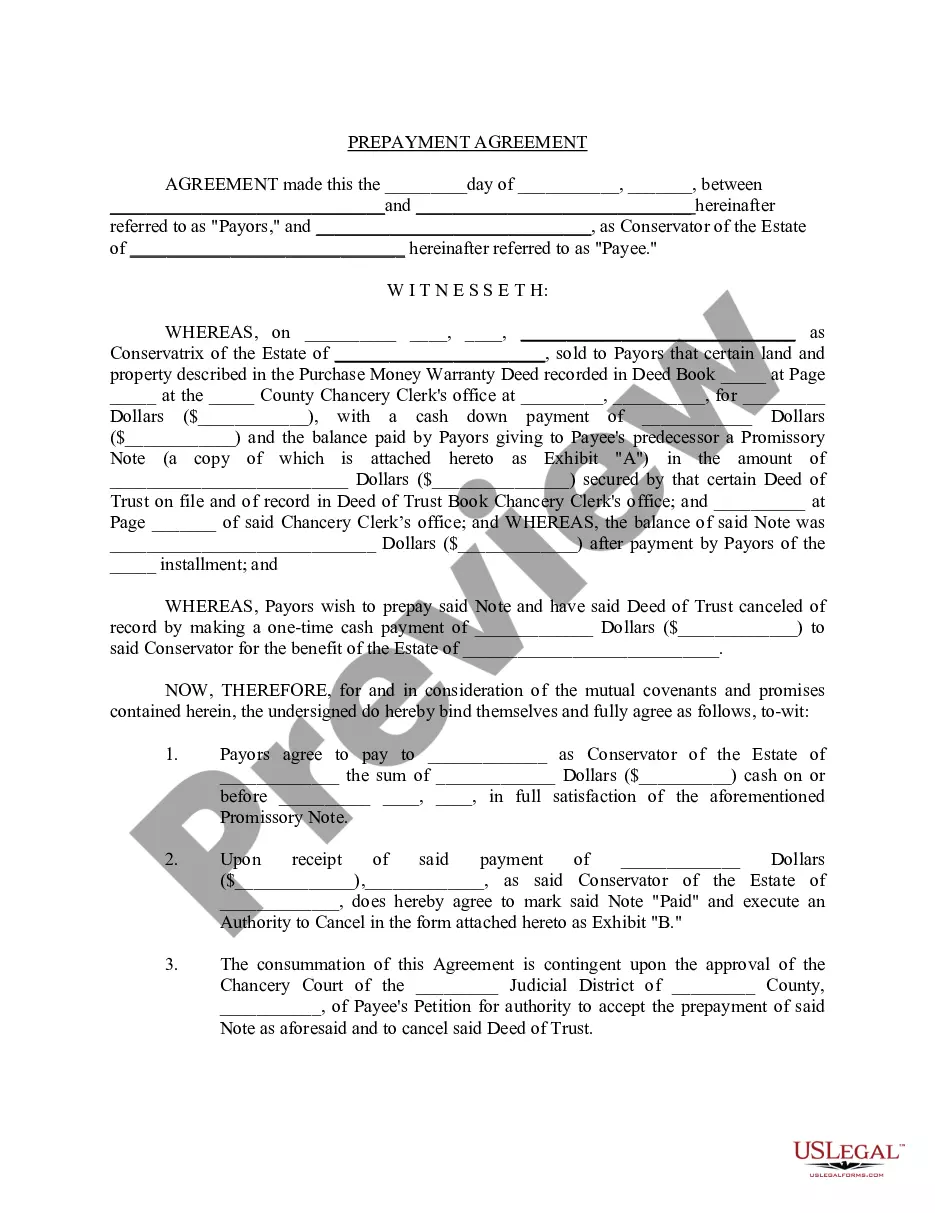

The Contra Costa California Prepayment Agreement is a legal contract that outlines the terms and conditions for prepaying a loan or mortgage in the Contra Costa County area of California. This agreement is typically used in real estate transactions and provides borrowers with the option to pay off their loan amount before the agreed-upon maturity date. The Contra Costa California Prepayment Agreement is designed to protect the interests of both the lender and the borrower. It specifies the prepayment terms, fees, and any conditions that may apply when the borrower decides to prepay their loan. This agreement is important as it allows borrowers to have more flexibility and control over their finances by providing an avenue to pay off their debt early, potentially saving on interest expenses. There are two main types of Contra Costa California Prepayment Agreements: 1. Hard Prepayment Penalty: This type of prepayment agreement imposes a significant penalty on the borrower if they choose to prepay their loan before a certain predetermined period. The penalty is often calculated as a percentage of the outstanding loan balance and serves as a deterrent for borrowers who may intend to refinance or pay off their loan early. 2. Soft Prepayment Penalty: In contrast to the hard prepayment penalty, this type of agreement allows borrowers to prepay their loan without incurring substantial penalties. Instead, a soft penalty may apply, which is typically a percentage of the outstanding loan balance but is significantly lower than that of a hard prepayment penalty. This type of agreement offers more flexibility to borrowers who anticipate paying off their loan early. By entering into a Contra Costa California Prepayment Agreement, borrowers can better understand the terms and conditions associated with early repayment and make informed decisions about their financial obligations. It is important for both lenders and borrowers to carefully review and negotiate the terms of this agreement to ensure fairness and transparency.

Contra Costa California Prepayment Agreement

Description

How to fill out Contra Costa California Prepayment Agreement?

Creating forms, like Contra Costa Prepayment Agreement, to take care of your legal affairs is a difficult and time-consumming process. Many cases require an attorney’s participation, which also makes this task not really affordable. Nevertheless, you can acquire your legal affairs into your own hands and handle them yourself. US Legal Forms is here to the rescue. Our website features over 85,000 legal forms created for different cases and life situations. We make sure each document is compliant with the regulations of each state, so you don’t have to worry about potential legal issues compliance-wise.

If you're already familiar with our website and have a subscription with US, you know how straightforward it is to get the Contra Costa Prepayment Agreement template. Go ahead and log in to your account, download the form, and customize it to your needs. Have you lost your document? Don’t worry. You can get it in the My Forms folder in your account - on desktop or mobile.

The onboarding process of new customers is just as simple! Here’s what you need to do before downloading Contra Costa Prepayment Agreement:

- Make sure that your document is specific to your state/county since the regulations for writing legal documents may differ from one state another.

- Learn more about the form by previewing it or reading a brief description. If the Contra Costa Prepayment Agreement isn’t something you were hoping to find, then use the header to find another one.

- Log in or create an account to start using our website and download the document.

- Everything looks great on your side? Hit the Buy now button and select the subscription option.

- Pick the payment gateway and type in your payment details.

- Your template is good to go. You can go ahead and download it.

It’s easy to find and purchase the needed document with US Legal Forms. Thousands of organizations and individuals are already benefiting from our rich library. Sign up for it now if you want to check what other perks you can get with US Legal Forms!