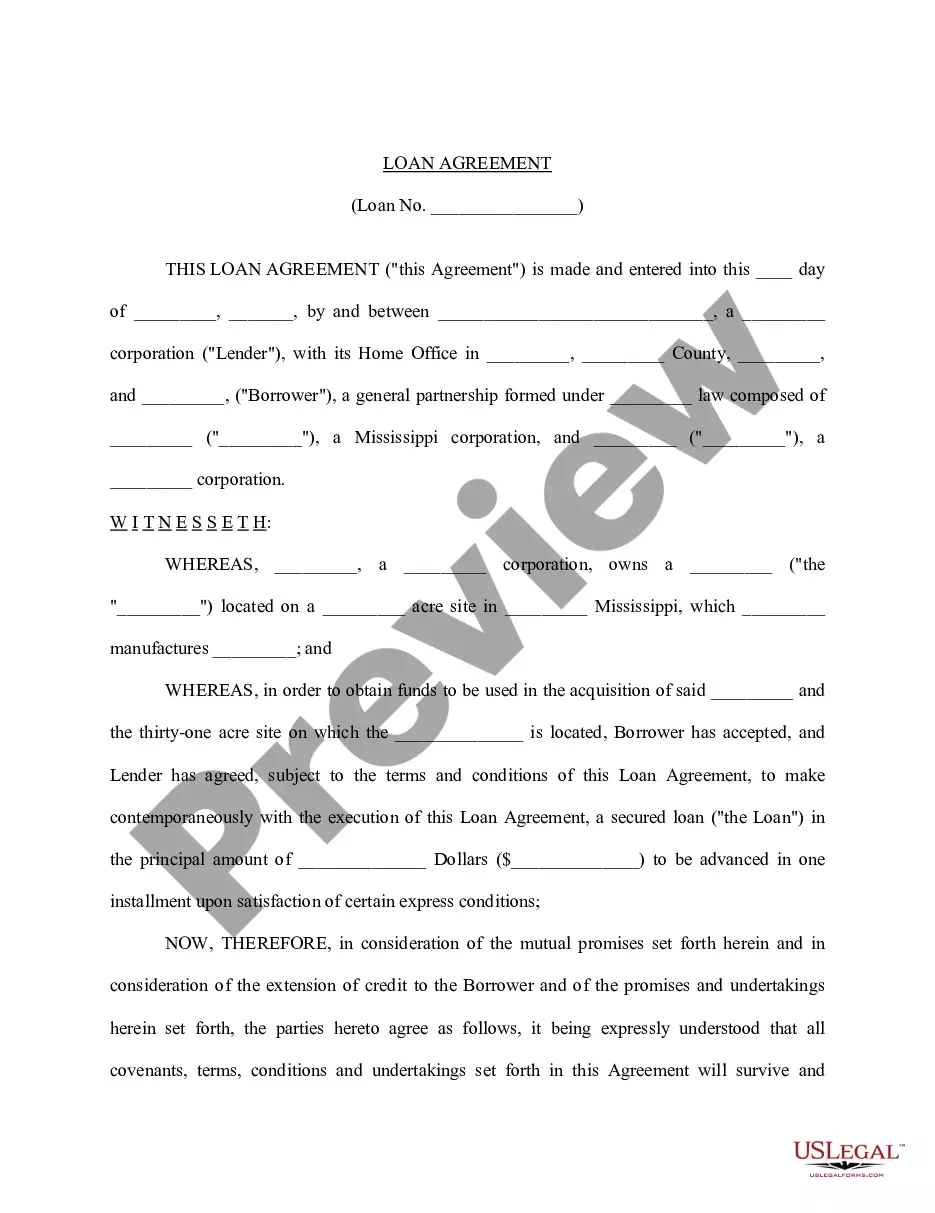

Suffolk New York Building Loan Agreement between Lender and Borrower

Description

How to fill out Building Loan Agreement Between Lender And Borrower?

Creating documents for business or personal requirements is always a significant obligation.

When preparing a contract, a public service application, or a power of attorney, it's crucial to consider all federal and state regulations pertinent to the particular area.

Nonetheless, smaller counties and even municipalities also have legislative measures that must be taken into account.

To find the template that fits your requisites, use the search tab located in the page header.

- All these factors make it arduous and time-intensive to draft a Suffolk Building Loan Agreement between Lender and Borrower without professional assistance.

- It is feasible to avoid unnecessary expenses on lawyers preparing your documents and create a legally binding Suffolk Building Loan Agreement between Lender and Borrower independently by utilizing the US Legal Forms online library.

- This is the most comprehensive digital collection of state-specific legal records that are officially validated, ensuring you can trust their legitimacy when selecting a template for your county.

- Users who subscribed earlier need merely to Log In to their accounts to download the required document.

- If you haven't yet subscribed, follow the step-by-step instructions below to acquire the Suffolk Building Loan Agreement between Lender and Borrower.

- Examine the page you’ve accessed and verify that it includes the sample you need.

- To accomplish this, use the form description and preview if these functionalities are offered.

Form popularity

FAQ

The lender has the right to amend the agreement at any time by adding, deleting, or changing provisions of the agreement. The lender has the right to charge late or interest fees if the borrower fails to pay the credit back on time.

Key Takeaways. A credit agreement is a legally-binding contract documenting the terms of a loan agreement; it is made between a person or party borrowing money and a lender. A credit agreement is part of the process for securing many different types of loans, including mortgages, credit cards, auto loans, and others.

party construction loan agreement typically lists the rights and remedies of all three parties, from the perspective of the borrower, the lender, and the builder.

The lender, sometimes also called the holder, is the person or business that will be providing the goods, money, or services to the borrower once the agreement has been agreed to and signed.

This term has many meanings in the financial world, but credit is generally defined as a contract agreement in which a borrower receives a sum of money or something of value and repays the lender at a later date, generally with interest.

Loan agreements are an important part of borrowing money; they protect both the borrower and the lender. A loan agreement spells out the details of the transaction, including the loan amount, the interest rate, and the terms.

Lender has the right to obtain information on Borrower's operations, financial activities, inventory, use of the loan, etc., and request Borrower to provide documents, materials and information such as financial statements. Lender's Rights and Obligations.

A lending agreement (loan agreement) is a formal contract between a lender and a borrower. Lending agreements spell out all the details of the loan, such as the principal amount, interest rate, amortization period, term, fees, payment terms and any covenants.

A credit agreement is a legally-binding contract documenting the terms of a loan agreement; it is made between a person or party borrowing money and a lender. The credit agreement outlines all of the terms associated with the loan.

Loan Agreements, Promissory Notes, and IOUs The most basic loan agreement is commonly called an "IOU." These are typically used between friends or relatives for small amounts of money, and simply state the dollar amount that is owed. They do not usually say when payment is due, nor include any interest provisions.