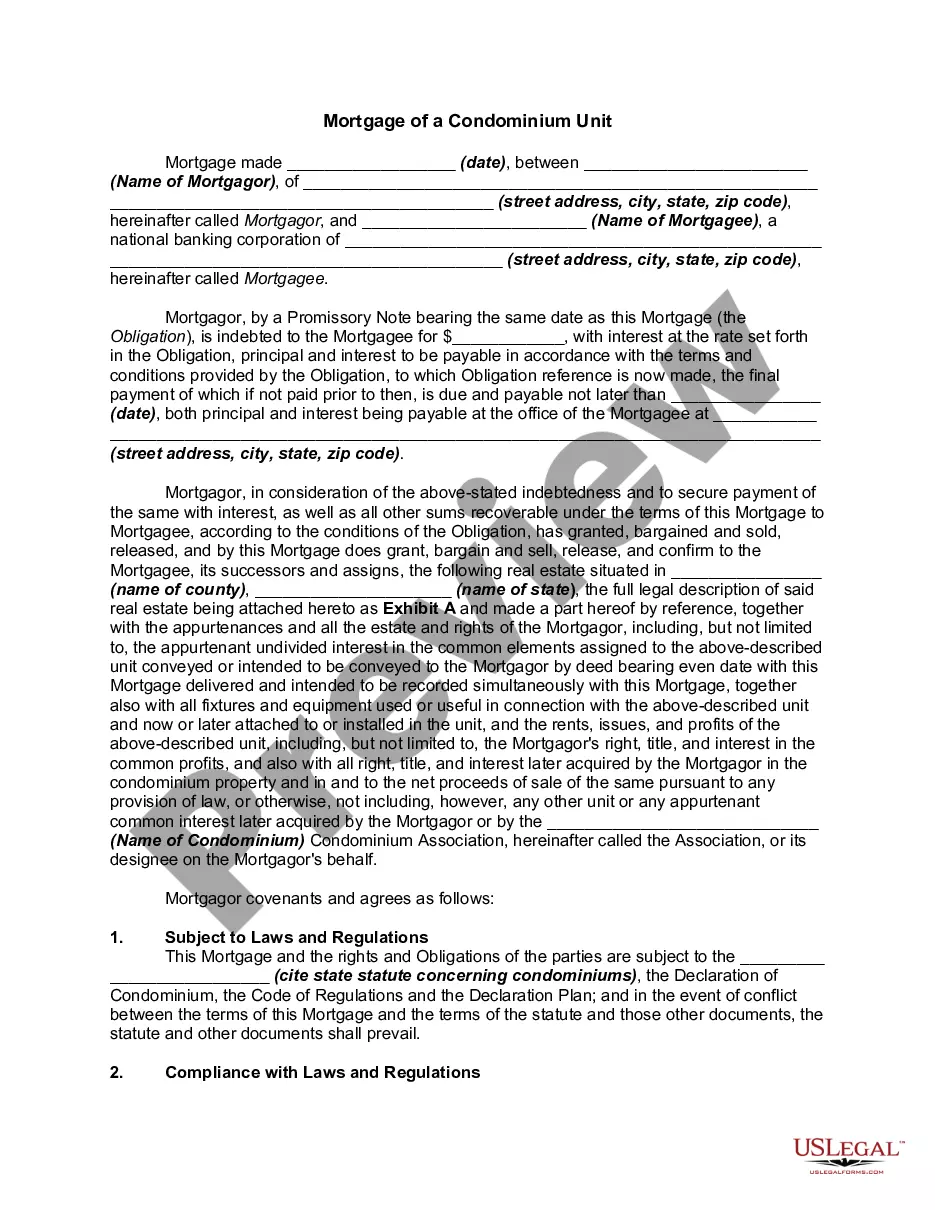

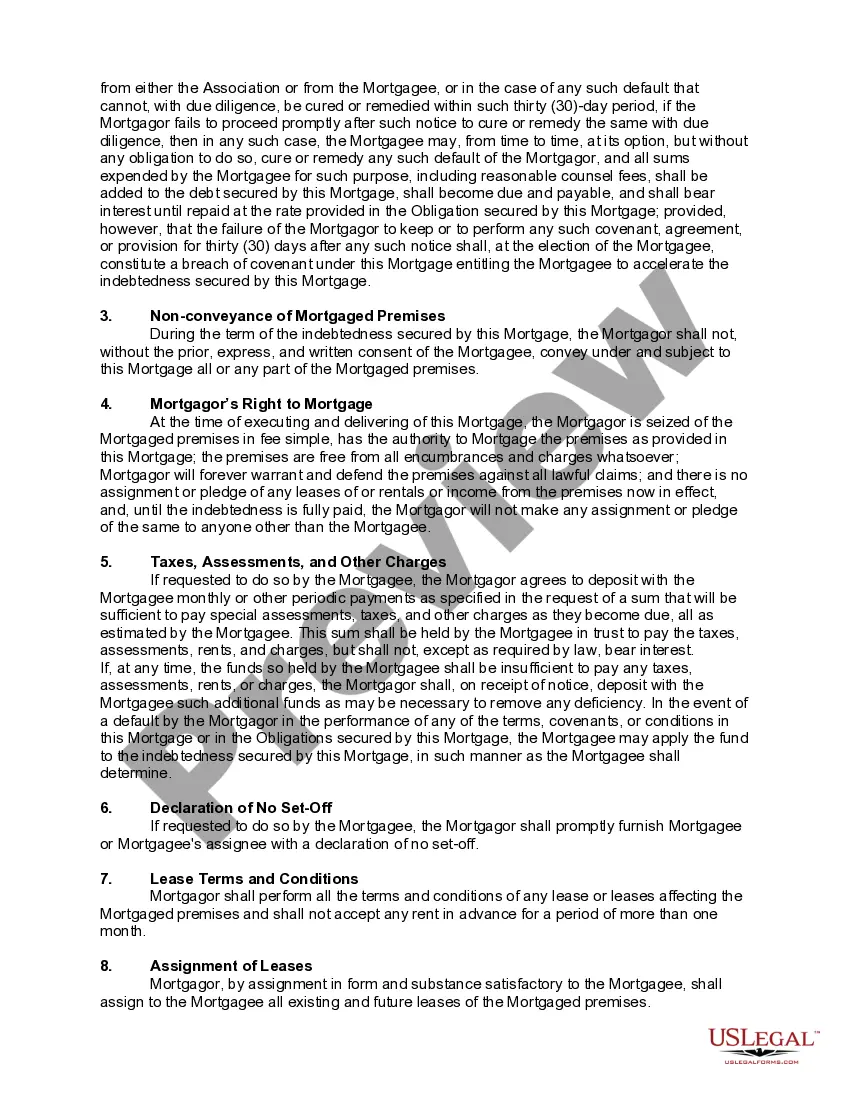

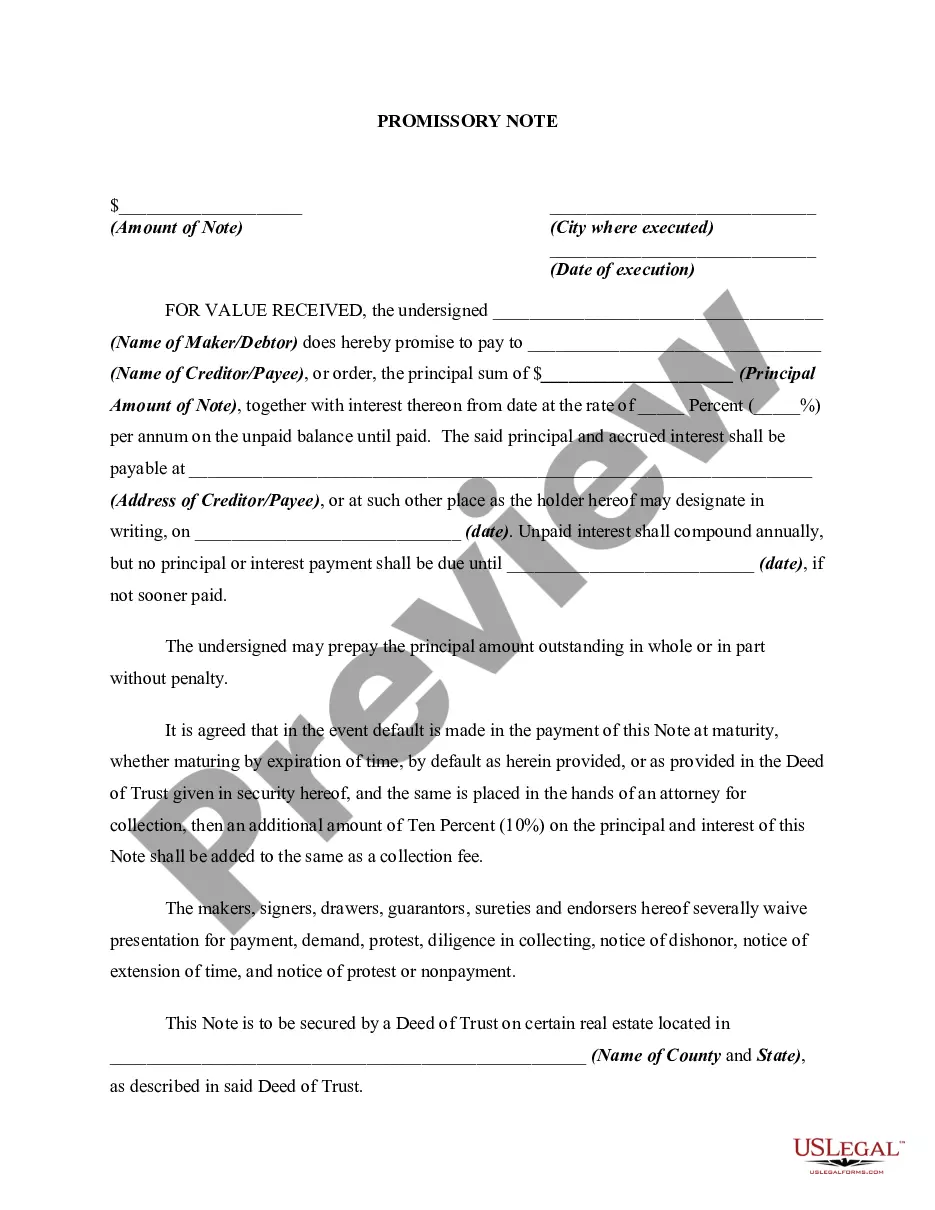

An agreement that creates an interest in real property as security for an obligation, such as the payment of a note, and that is to cease upon the performance of the obligation, is called a mortgage. The person whose interest in the property is given as security is the mortgagor. The person who receives the security is the mortgagee (lender). Two characteristics of a mortgage are (a) the mortgagee's interest terminates upon the performance of the obligation secured by the mortgage such as payment of the note secured by the mortgage; and (b) the mortgagee has the right to enforce the mortgage by foreclosure if the mortgagor fails to perform the obligation (such as defaulting on the note payments).

A condominium is a combination of co-ownership and individual ownership. Those who own an apartment house or buy a condominium are co-owners of the land and of the halls, lobby, and other common areas, but each apartment in the building is individually owned by its occupant. In some States, the owners of the various units in the condominium have equal voice in the management and share an equal part of the expenses. In other States, control and liability for expenses are shared by a unit owner in the same ratio as the value of the unit bears to the value of the entire condominium project. The bigger condominium owners would have more say-so than the smaller condominium owners.

A Chicago Illinois Mortgage of a Condominium Unit refers to a loan obtained by a homebuyer to finance the purchase of a condominium in Chicago, Illinois. Condos are a popular housing option in the city, offering a mix of convenience, affordability, and community living. This type of mortgage allows individuals or families to finance their condo unit with the help of a lending institution, usually a bank or a mortgage company. Condominiums are multi-unit properties that typically feature individual units owned by different individuals and common areas maintained by a homeowners' association (HOA). When purchasing a condo in Chicago, obtaining a mortgage becomes crucial for most buyers as it allows them to spread the cost over a period of time, typically through monthly payments. The terms and conditions of the mortgage vary and are influenced by factors such as the buyer's creditworthiness, the condo's market value, and prevailing interest rates. Different types of mortgages available for purchasing a Chicago condominium unit include: 1. Conventional Mortgage for Condos: This is the most common type of mortgage, usually requiring a down payment of 10-20% of the condo's purchase price. It follows the guidelines set by Fannie Mae and Freddie Mac, the two government-sponsored enterprises that purchase and guarantee mortgage-backed securities. 2. FHA Mortgages for Condos: Backed by the Federal Housing Administration (FHA), this mortgage is popular among first-time homebuyers and those with a lower credit score. It requires a lower down payment, around 3.5%, but also has additional eligibility criteria for the condo complex itself, such as meeting certain owner-occupancy and financial stability standards. 3. VA Mortgages for Condos: Available exclusively to eligible military veterans and active-duty service members, this mortgage is offered by the Department of Veterans Affairs (VA). It provides competitive interest rates and flexible terms, offering veterans an opportunity to buy a condo with little to now down payment. 4. Jumbo Mortgage for Condos: For luxury or high-value condos in Chicago, a jumbo mortgage may be required. This type of mortgage exceeds the loan limits set by Fannie Mae and Freddie Mac. 5. Portfolio Mortgage for Condos: Some lenders, such as community banks or credit unions, may offer portfolio mortgages, which are loans they keep in their own portfolio instead of selling them to other institutions. This type of mortgage may provide more flexibility in terms of eligibility requirements. Obtaining a Chicago Illinois Mortgage of a Condominium Unit requires careful consideration of various factors, including the buyer's financial situation, credit score, and long-term goals. Buyers are encouraged to consult with mortgage professionals, explore different mortgage options, and assess the terms and conditions before committing to a loan.A Chicago Illinois Mortgage of a Condominium Unit refers to a loan obtained by a homebuyer to finance the purchase of a condominium in Chicago, Illinois. Condos are a popular housing option in the city, offering a mix of convenience, affordability, and community living. This type of mortgage allows individuals or families to finance their condo unit with the help of a lending institution, usually a bank or a mortgage company. Condominiums are multi-unit properties that typically feature individual units owned by different individuals and common areas maintained by a homeowners' association (HOA). When purchasing a condo in Chicago, obtaining a mortgage becomes crucial for most buyers as it allows them to spread the cost over a period of time, typically through monthly payments. The terms and conditions of the mortgage vary and are influenced by factors such as the buyer's creditworthiness, the condo's market value, and prevailing interest rates. Different types of mortgages available for purchasing a Chicago condominium unit include: 1. Conventional Mortgage for Condos: This is the most common type of mortgage, usually requiring a down payment of 10-20% of the condo's purchase price. It follows the guidelines set by Fannie Mae and Freddie Mac, the two government-sponsored enterprises that purchase and guarantee mortgage-backed securities. 2. FHA Mortgages for Condos: Backed by the Federal Housing Administration (FHA), this mortgage is popular among first-time homebuyers and those with a lower credit score. It requires a lower down payment, around 3.5%, but also has additional eligibility criteria for the condo complex itself, such as meeting certain owner-occupancy and financial stability standards. 3. VA Mortgages for Condos: Available exclusively to eligible military veterans and active-duty service members, this mortgage is offered by the Department of Veterans Affairs (VA). It provides competitive interest rates and flexible terms, offering veterans an opportunity to buy a condo with little to now down payment. 4. Jumbo Mortgage for Condos: For luxury or high-value condos in Chicago, a jumbo mortgage may be required. This type of mortgage exceeds the loan limits set by Fannie Mae and Freddie Mac. 5. Portfolio Mortgage for Condos: Some lenders, such as community banks or credit unions, may offer portfolio mortgages, which are loans they keep in their own portfolio instead of selling them to other institutions. This type of mortgage may provide more flexibility in terms of eligibility requirements. Obtaining a Chicago Illinois Mortgage of a Condominium Unit requires careful consideration of various factors, including the buyer's financial situation, credit score, and long-term goals. Buyers are encouraged to consult with mortgage professionals, explore different mortgage options, and assess the terms and conditions before committing to a loan.