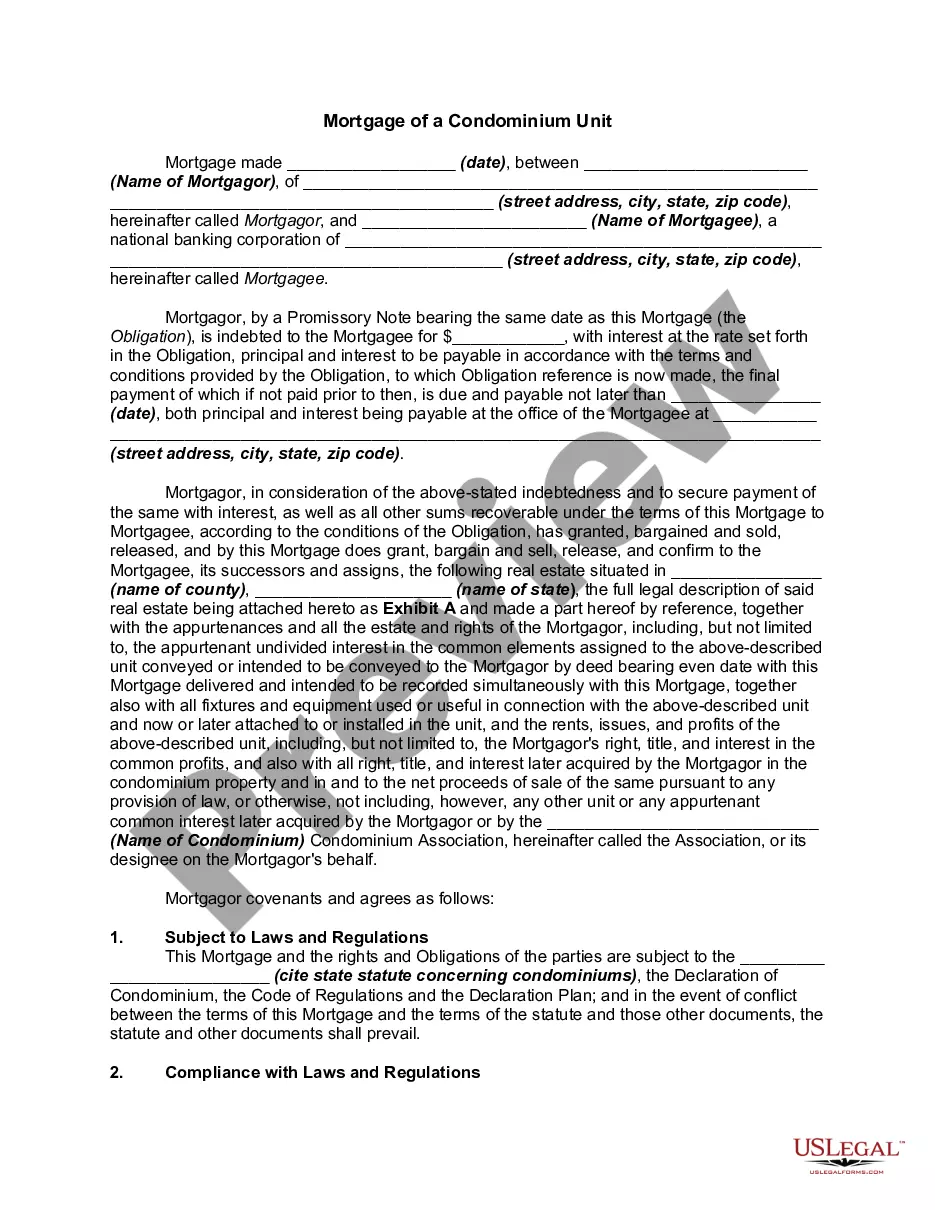

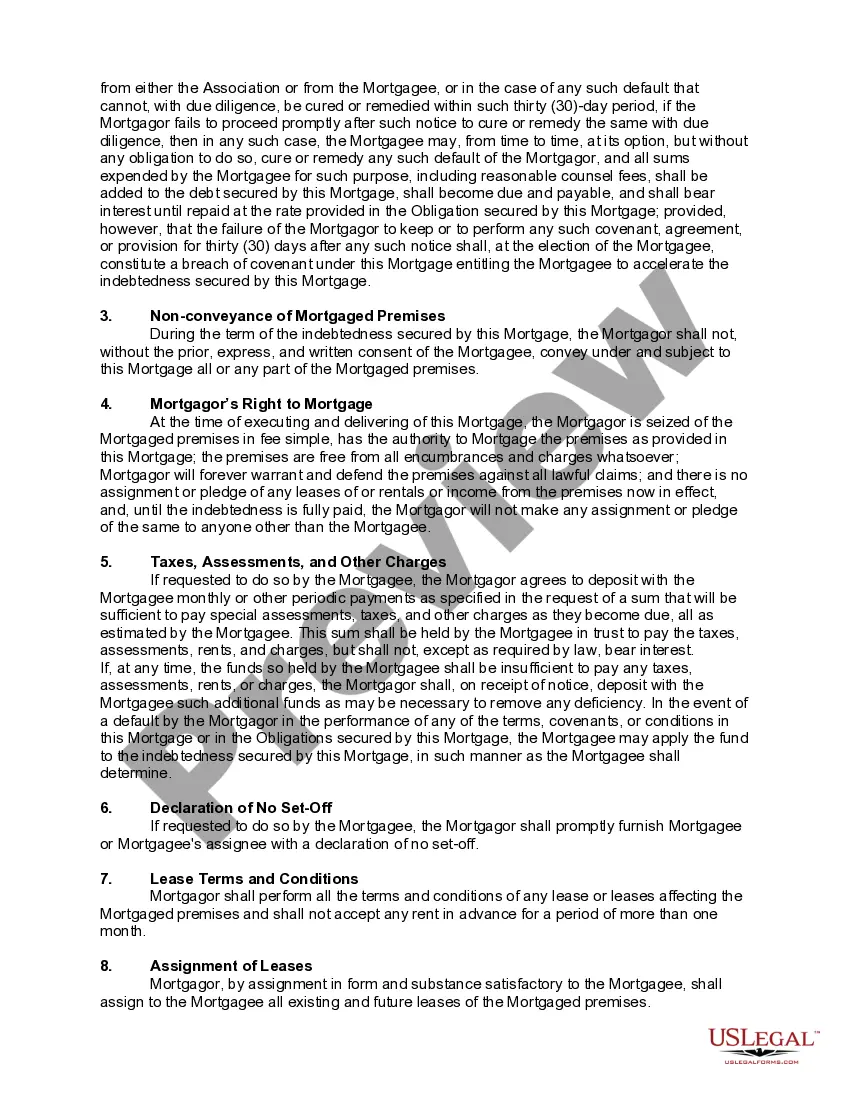

An agreement that creates an interest in real property as security for an obligation, such as the payment of a note, and that is to cease upon the performance of the obligation, is called a mortgage. The person whose interest in the property is given as security is the mortgagor. The person who receives the security is the mortgagee (lender). Two characteristics of a mortgage are (a) the mortgagee's interest terminates upon the performance of the obligation secured by the mortgage such as payment of the note secured by the mortgage; and (b) the mortgagee has the right to enforce the mortgage by foreclosure if the mortgagor fails to perform the obligation (such as defaulting on the note payments).

A condominium is a combination of co-ownership and individual ownership. Those who own an apartment house or buy a condominium are co-owners of the land and of the halls, lobby, and other common areas, but each apartment in the building is individually owned by its occupant. In some States, the owners of the various units in the condominium have equal voice in the management and share an equal part of the expenses. In other States, control and liability for expenses are shared by a unit owner in the same ratio as the value of the unit bears to the value of the entire condominium project. The bigger condominium owners would have more say-so than the smaller condominium owners.

Houston Texas Mortgage of a Condominium Unit: A Detailed Description If you are considering purchasing a condominium unit in Houston, Texas, understanding the mortgage options available to you is crucial. A Houston Texas Mortgage of a Condominium Unit refers to the financing provided by lenders specifically for purchasing or refinancing a condo in Houston. When it comes to Houston Texas Mortgage of a Condominium Unit, there are a few different types available to cater to diverse buyer needs. Some common types include: 1. Conventional Condo Mortgage: This is the most traditional type of mortgage, offered by banks, credit unions, or mortgage lenders. It follows Fannie Mae or Freddie Mac guidelines and requires a down payment of at least 5% to 20%, depending on the lender's requirements. Interest rates may be fixed or adjustable. 2. FHA (Federal Housing Administration) Condo Mortgage: Backed by the government, an FHA condo mortgage is ideal for buyers with lower credit scores or those who cannot afford a large down payment. The down payment requirement is usually lower (3.5% of the purchase price), but buyers are required to pay mortgage insurance premiums (MIP) to protect the lender. 3. VA (Department of Veterans Affairs) Condo Mortgage: Specifically designed for active-duty military personnel, veterans, and eligible surviving spouses, VA condo mortgages offer favorable terms, including no down payment requirement, competitive interest rates, and no private mortgage insurance (PMI) requirement. 4. Jumbo Condo Mortgage: A jumbo condo mortgage is suitable when purchasing high-value condos that exceed the conventional loan limits set by Fannie Mae or Freddie Mac. These loans typically require a larger down payment and may have stricter qualification criteria. 5. Portfolio Condo Mortgage: When condos do not meet the standard guidelines set by Fannie Mae or Freddie Mac, some local banks or credit unions may offer portfolio loans. These mortgages have more flexible terms and may be ideal for borrowers who don't fit the conventional mortgage criteria, such as self-employed individuals or those with non-traditional income sources. When applying for a Houston Texas Mortgage of a Condominium Unit, it is essential to gather the necessary documentation, including financial statements, tax returns, proof of income, credit history, and the condo association's financial documents like budget, bylaws, and insurance coverage. Lenders will also review the condo's eligibility, including the percentage of owner-occupied units, insurance coverage, and financial stability of the condo association. Choosing the right mortgage for your Houston condominium unit depends on various factors, such as your financial situation, credit score, down payment capability, and the specific requirements set by the condo association. Working with a professional mortgage lender or broker specializing in condo financing can help you navigate through the options and find the most suitable mortgage loan that meets your needs and budget.Houston Texas Mortgage of a Condominium Unit: A Detailed Description If you are considering purchasing a condominium unit in Houston, Texas, understanding the mortgage options available to you is crucial. A Houston Texas Mortgage of a Condominium Unit refers to the financing provided by lenders specifically for purchasing or refinancing a condo in Houston. When it comes to Houston Texas Mortgage of a Condominium Unit, there are a few different types available to cater to diverse buyer needs. Some common types include: 1. Conventional Condo Mortgage: This is the most traditional type of mortgage, offered by banks, credit unions, or mortgage lenders. It follows Fannie Mae or Freddie Mac guidelines and requires a down payment of at least 5% to 20%, depending on the lender's requirements. Interest rates may be fixed or adjustable. 2. FHA (Federal Housing Administration) Condo Mortgage: Backed by the government, an FHA condo mortgage is ideal for buyers with lower credit scores or those who cannot afford a large down payment. The down payment requirement is usually lower (3.5% of the purchase price), but buyers are required to pay mortgage insurance premiums (MIP) to protect the lender. 3. VA (Department of Veterans Affairs) Condo Mortgage: Specifically designed for active-duty military personnel, veterans, and eligible surviving spouses, VA condo mortgages offer favorable terms, including no down payment requirement, competitive interest rates, and no private mortgage insurance (PMI) requirement. 4. Jumbo Condo Mortgage: A jumbo condo mortgage is suitable when purchasing high-value condos that exceed the conventional loan limits set by Fannie Mae or Freddie Mac. These loans typically require a larger down payment and may have stricter qualification criteria. 5. Portfolio Condo Mortgage: When condos do not meet the standard guidelines set by Fannie Mae or Freddie Mac, some local banks or credit unions may offer portfolio loans. These mortgages have more flexible terms and may be ideal for borrowers who don't fit the conventional mortgage criteria, such as self-employed individuals or those with non-traditional income sources. When applying for a Houston Texas Mortgage of a Condominium Unit, it is essential to gather the necessary documentation, including financial statements, tax returns, proof of income, credit history, and the condo association's financial documents like budget, bylaws, and insurance coverage. Lenders will also review the condo's eligibility, including the percentage of owner-occupied units, insurance coverage, and financial stability of the condo association. Choosing the right mortgage for your Houston condominium unit depends on various factors, such as your financial situation, credit score, down payment capability, and the specific requirements set by the condo association. Working with a professional mortgage lender or broker specializing in condo financing can help you navigate through the options and find the most suitable mortgage loan that meets your needs and budget.