Houston Texas Promissory Note in Connection with a Sale and Purchase of a Mobile Home

Description

How to fill out Promissory Note In Connection With A Sale And Purchase Of A Mobile Home?

Creating documents for business or personal requirements is always a significant obligation.

When formulating a contract, a public service petition, or a power of attorney, it is crucial to consider all federal and state laws of the specific region.

Nevertheless, small counties and even towns also possess legislative regulations that must be taken into account.

Join the platform and swiftly access verified legal documents for any situation with just a few clicks!

- All these aspects contribute to the anxiety and time-consuming nature of drafting a Houston Promissory Note in Relation to a Sale and Purchase of a Mobile Home without expert help.

- It is feasible to circumvent spending on attorneys for drafting your documents and create a legally binding Houston Promissory Note in Relation to a Sale and Purchase of a Mobile Home independently, utilizing the US Legal Forms online library.

- This is the largest online compilation of state-specific legal templates that are professionally validated, ensuring their legitimacy when selecting a template for your county.

- Previous subscribers merely need to Log In to their accounts to retrieve the necessary document.

- If you still lack a subscription, follow the detailed guide below to acquire the Houston Promissory Note in Relation to a Sale and Purchase of a Mobile Home.

- Browse through the page you've opened and confirm if it contains the sample you require.

- To do this, utilize the form description and preview if these features are accessible.

Form popularity

FAQ

In Texas, a promissory note does not require notarization to be valid; however, it is beneficial for legal clarity. Notarization provides an additional layer of verification and can help prevent disputes in the future. When using a Houston Texas Promissory Note for transactions involving a mobile home, having it notarized might offer both parties extra peace of mind.

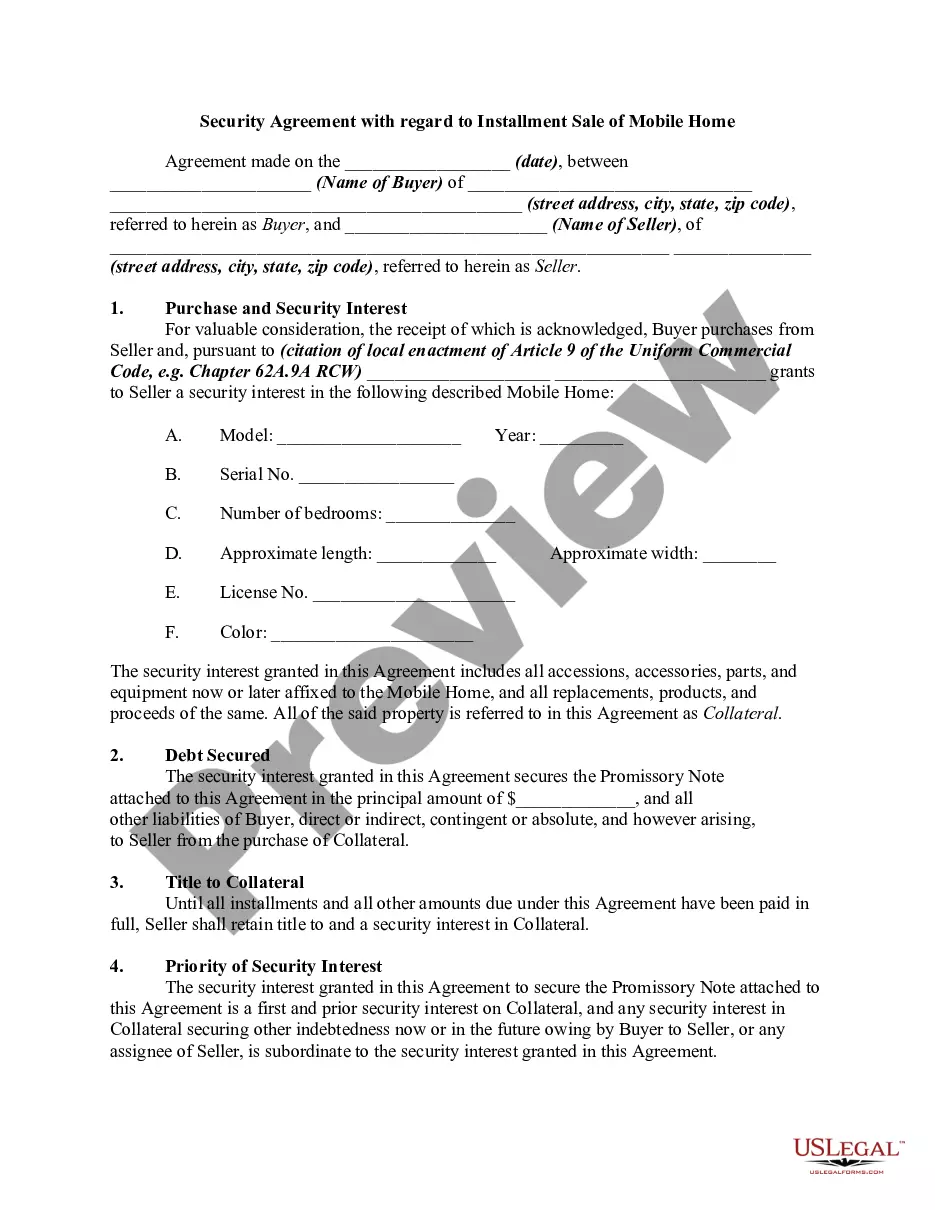

Securing a promissory note with real property involves creating a deed of trust or mortgage that links the note to the property. This document provides the lender with rights to the property in case the borrower defaults. When dealing with a Houston Texas Promissory Note for a mobile home, this process ensures that both parties have clear, legal recourse if needed.

Transferring a mobile home title to a family member in Texas typically requires a few key steps. First, you must complete the title transfer form, which you can obtain from the Texas Department of Motor Vehicles. After filling out the necessary details, both the seller and the family member must sign the document. Lastly, submit the signed form along with any applicable fees to the county tax assessor-collector’s office to finalize the transfer.

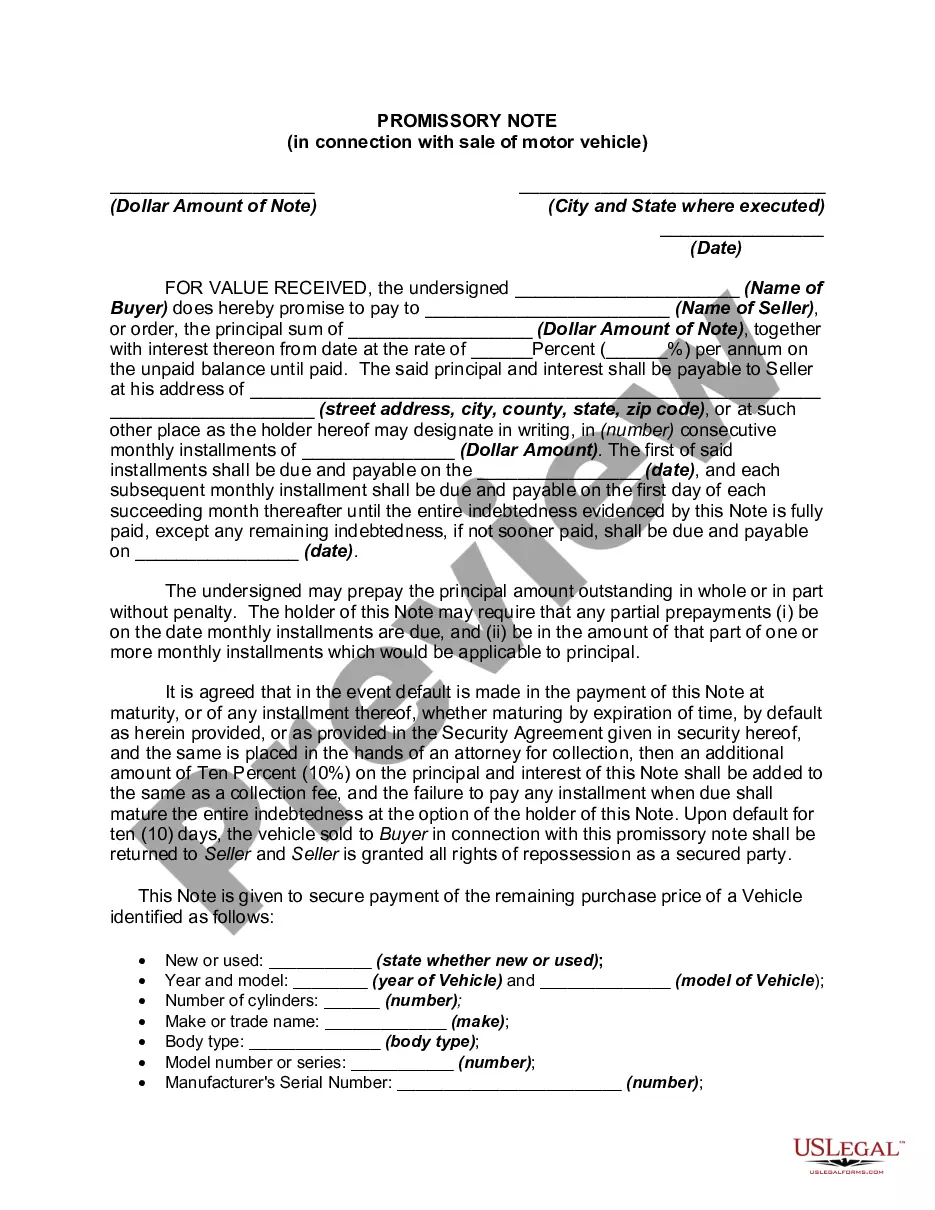

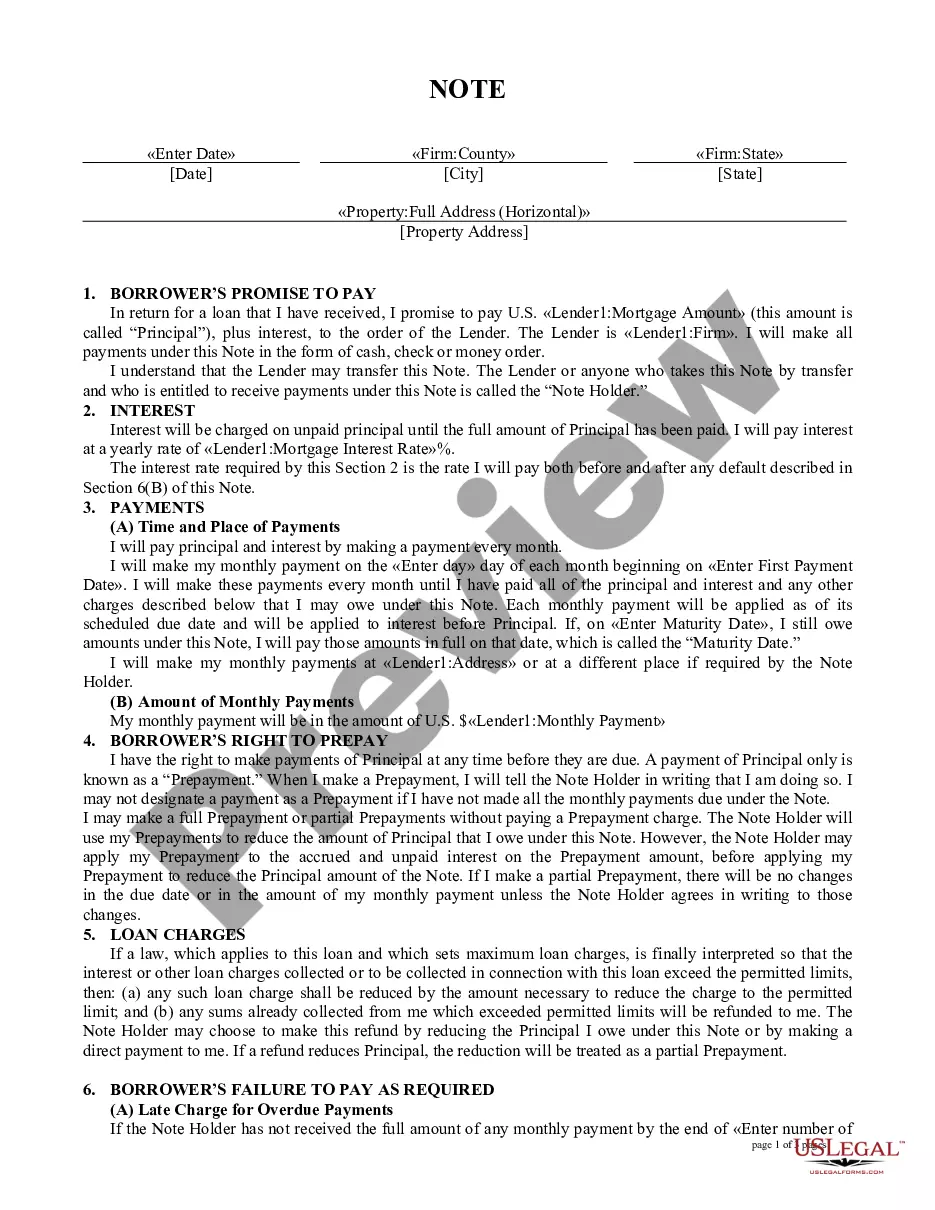

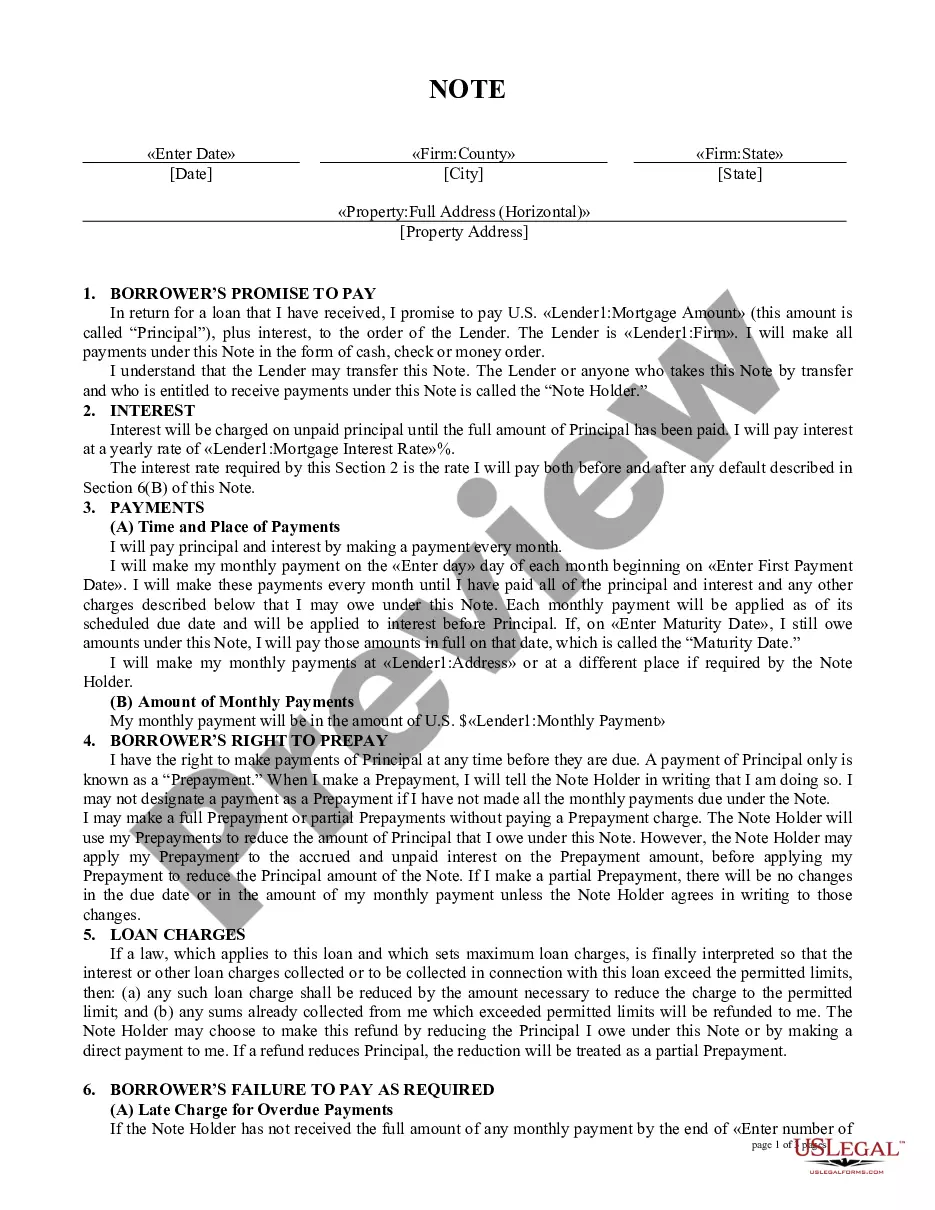

A promissory note must include the date of the loan, the dollar amount, the names of both parties, the rate of interest, any collateral involved, and the timeline for repayment. When this document is signed by the borrower, it becomes a legally binding contract.

This Promissory Note is transferable and assignable by the Lender to any person or entity previously approved by the Company. The Company agrees to issue replacement Notes to facilitate such approved transfers and assignments.

Unless specifically prohibited in the language of the note, a promissory note is assignable by the lender. That is, the lender can sell or assign the note to a third party who the borrower must then repay.

A promissory note should have several essential elements, including the amount of the loan, the date by which it is to be paid back, the interest rate, and a record of any collateral that is being used to secure the loan.

Even without a signature from a notary public, it can still be a valid promissory note. Getting your loan agreement notarized can strengthen it in sensitive cases: Notarizing your note could make it legally stronger. ? This means it's more likely to stand up in court thanks to the extra witness of a notary public.

The person who owns the promissory note may sell it. Lenders typically sell promissory notes when they no longer want to be responsible for the loan or they need a lump sum of cash. The buyer of the note assumes the responsibility of collecting the money.

When a loan changes hands, the promissory note is endorsed (signed over) to the loan's new owner. In some cases, the note is endorsed in blank, making it a bearer instrument under Article 3 of the Uniform Commercial Code. Whoever holds the note has the legal authority to enforce it and has standing to foreclose.