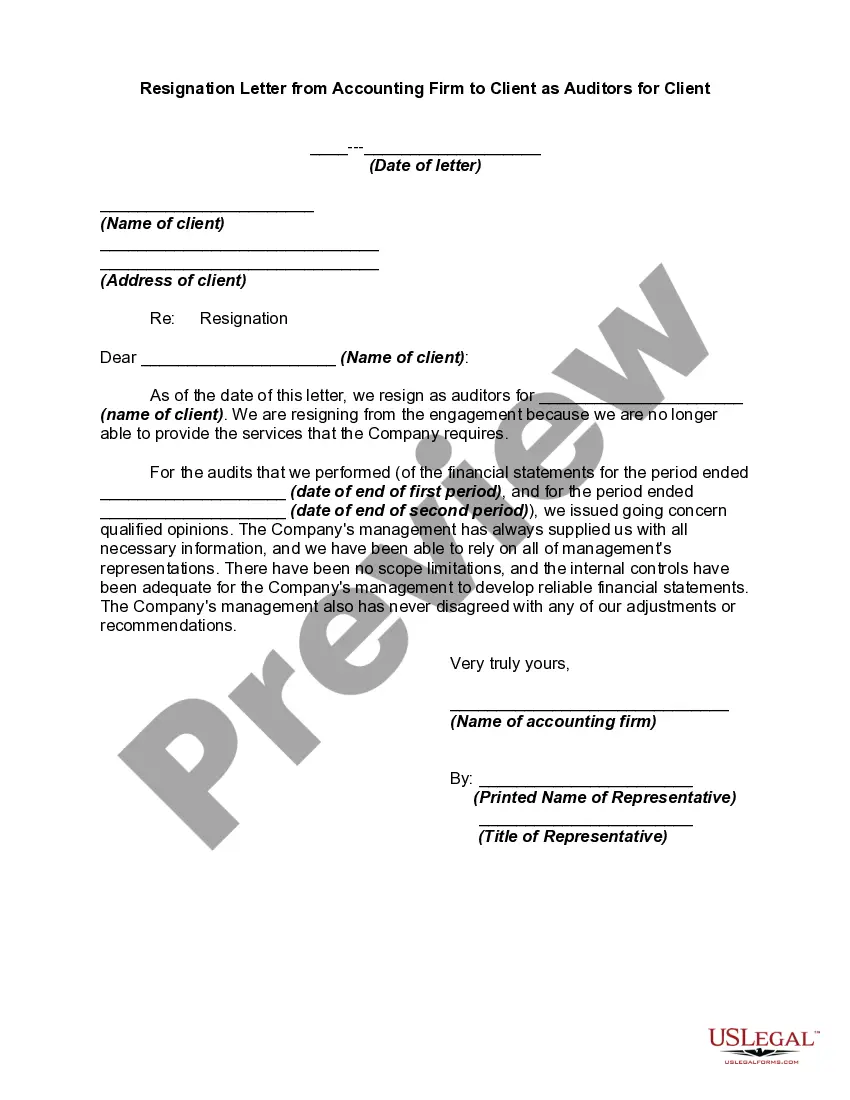

San Antonio, Texas is a vibrant city located in the southern part of the state. Known for its rich history, diverse culture, and thriving economy, San Antonio offers a unique blend of modern amenities and traditional Texan charm. Resignation letters from accounting firms to clients as auditors are a formal way of terminating the professional relationship between the firm and the client. These letters can be categorized into two types: voluntary resignation and forced resignation. 1. Voluntary Resignation: A voluntary resignation letter from an accounting firm to a client as auditors is initiated when the firm decides to terminate the auditing services due to various reasons. It could be the result of the firm's business strategy changes, capacity limitations, or a shift in the firm's focus to other clients or industries. The letter typically expresses gratitude for the opportunity to work with the client and provides a clear timeline for the transition of any remaining tasks or documentation. Keywords: voluntary resignation, accounting firm, client, auditors, terminating auditing services, business strategy, capacity limitations, transition, remaining tasks, documentation. 2. Forced Resignation: A forced resignation letter from an accounting firm to a client as auditors occurs when the client and/or regulatory authorities deem the firm's services to be incompatible, unsatisfactory, or in violation of professional standards or legal requirements. This type of resignation letter is typically a result of extreme circumstances, such as a breach of trust, unethical conduct, or discovery of misconduct. The letter highlights the reasons for the forced resignation and assures the client of the firm's commitment to rectifying any issues or cooperating with legal investigations if necessary. Keywords: forced resignation, accounting firm, client, auditors, incompatibility, unsatisfactory services, professional standards, legal requirements, breach of trust, unethical conduct, misconduct, rectifying issues, cooperating with legal investigations. In both types of resignation letters, it is crucial to maintain professionalism, clarity, and transparency in communicating the decision to terminate the auditing services. The letters should focus on ensuring a smooth transition for the client, whether it involves recommending alternative auditors or providing assistance during the handover of financial records, ensuring minimal disruption to the client's operations.

San Antonio Texas Resignation Letter from Accounting Firm to Client as Auditors for Client

Description

How to fill out San Antonio Texas Resignation Letter From Accounting Firm To Client As Auditors For Client?

How much time does it normally take you to draft a legal document? Because every state has its laws and regulations for every life sphere, locating a San Antonio Resignation Letter from Accounting Firm to Client as Auditors for Client meeting all regional requirements can be exhausting, and ordering it from a professional attorney is often expensive. Numerous web services offer the most common state-specific documents for download, but using the US Legal Forms library is most advantegeous.

US Legal Forms is the most comprehensive web catalog of templates, gathered by states and areas of use. In addition to the San Antonio Resignation Letter from Accounting Firm to Client as Auditors for Client, here you can get any specific document to run your business or individual affairs, complying with your regional requirements. Specialists check all samples for their actuality, so you can be sure to prepare your documentation properly.

Using the service is remarkably straightforward. If you already have an account on the platform and your subscription is valid, you only need to log in, select the needed sample, and download it. You can pick the document in your profile at any time in the future. Otherwise, if you are new to the website, there will be some extra steps to complete before you obtain your San Antonio Resignation Letter from Accounting Firm to Client as Auditors for Client:

- Examine the content of the page you’re on.

- Read the description of the template or Preview it (if available).

- Search for another document using the corresponding option in the header.

- Click Buy Now when you’re certain in the selected document.

- Decide on the subscription plan that suits you most.

- Create an account on the platform or log in to proceed to payment options.

- Make a payment via PalPal or with your credit card.

- Change the file format if necessary.

- Click Download to save the San Antonio Resignation Letter from Accounting Firm to Client as Auditors for Client.

- Print the sample or use any preferred online editor to complete it electronically.

No matter how many times you need to use the acquired document, you can find all the samples you’ve ever downloaded in your profile by opening the My Forms tab. Give it a try!