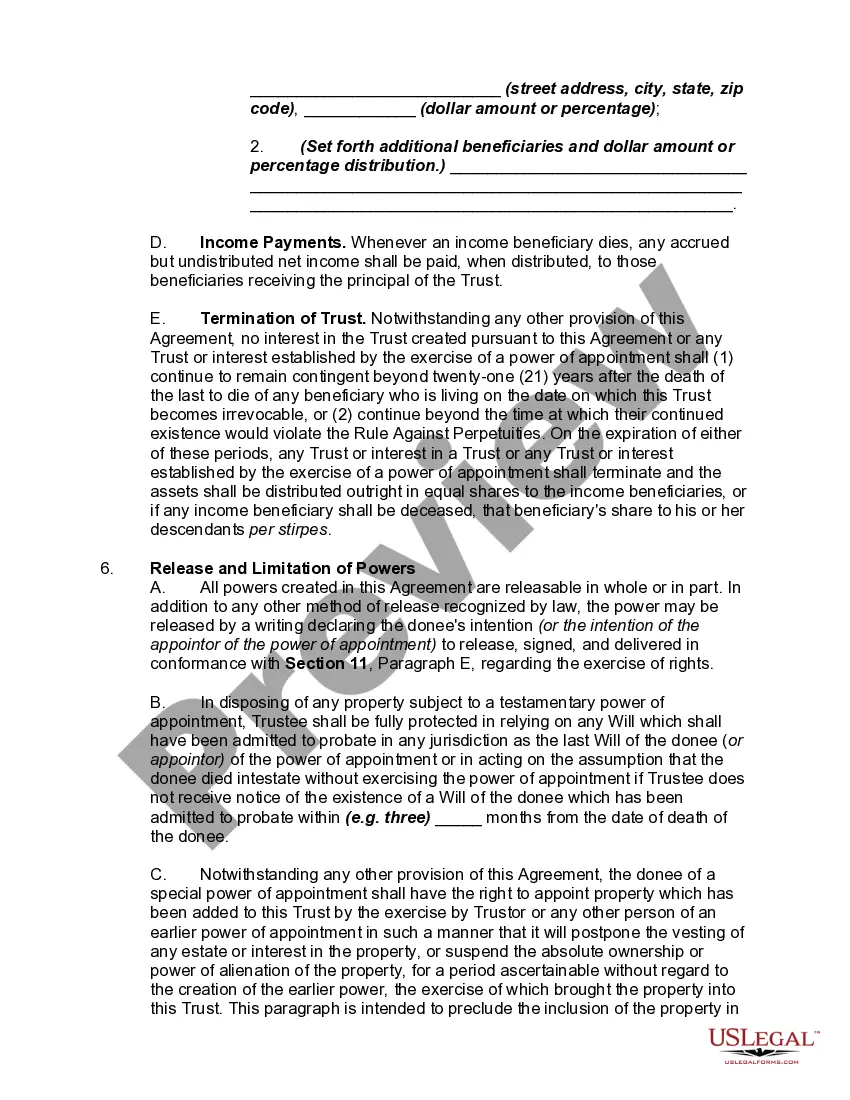

An A-B trust is a revocable living trust which divides into two trusts upon the death of the first spouse. This type of trust makes use of both the estate tax exemption ($3.5 million per person in 2009) and the marital deduction to make it so that no estate taxes are due upon the death of the first spouse. The B Trust is also known as the Bypass trust and it contains the amount of that years applicable exclusion amount. The A trust is the marital deduction trust which will typically contain both the surviving spouse's separate property and one half community property interests but also the residue of the deceased spouse's estate after the estate tax exemption has been utilized by the B trust. The use of an A-B trust ensures that both spouse's applicable exclusion amounts are effectively used, thereby doubling the amount of property which can pass to heirs free of Federal Estate Taxes.

Mecklenburg North Carolina Marital Deduction Trust — Trust A and Bypass Trust B are two specific types of trust structures commonly used in estate planning in Mecklenburg County, North Carolina. These trusts allow married couples to maximize the amount of assets they can pass on to their heirs while minimizing estate taxes. Here is a detailed description of these trusts along with relevant keywords: 1. Mecklenburg North Carolina Marital Deduction Trust (Trust A): The Mecklenburg North Carolina Marital Deduction Trust, also known as a TIP trust (Qualified Terminable Interest Property), is a type of trust designed to take advantage of the unlimited marital deduction for federal estate tax purposes. It allows one spouse to transfer assets to the trust, ensuring the surviving spouse receives income from it for their lifetime. The surviving spouse has limited access to the principal but receives income distributions. With this trust, the value of the assets in the trust is not included in the surviving spouse's estate upon their death, thereby reducing potential estate tax liabilities. Keywords: Marital deduction, TIP trust, unlimited marital deduction, federal estate tax, surviving spouse, income distributions, estate tax liabilities. 2. Bypass Trust (Trust B): The Bypass Trust, also known as an A/B trust or credit shelter trust, is another type of trust utilized by married couples to minimize estate taxes. When the first spouse dies, a portion of the deceased spouse's assets, up to the estate tax exemption amount, are placed in the Bypass Trust. This trust ensures that the exemption amount is effectively used, as it is not subject to estate taxes upon the surviving spouse's death. The remaining assets (above the exemption amount) pass to the Marital Deduction Trust. By splitting the assets between the Bypass Trust and the Marital Deduction Trust, the couple can take advantage of both spouses' estate tax exemptions, reducing the total estate tax due. Keywords: Bypass Trust, A/B trust, credit shelter trust, estate tax exemption, estate taxes, surviving spouse, Marital Deduction Trust, estate tax due. These two trusts, the Mecklenburg North Carolina Marital Deduction Trust — Trust A and Bypass Trust B, are commonly used in estate planning to help married couples minimize estate taxes and efficiently distribute their assets. Both trusts offer different mechanisms for asset protection and tax efficiency, depending on the specific circumstances and goals of the individuals. Estate planning professionals in Mecklenburg County can provide personalized guidance on whether these trusts are suitable for a particular situation and help their clients implement them effectively.Mecklenburg North Carolina Marital Deduction Trust — Trust A and Bypass Trust B are two specific types of trust structures commonly used in estate planning in Mecklenburg County, North Carolina. These trusts allow married couples to maximize the amount of assets they can pass on to their heirs while minimizing estate taxes. Here is a detailed description of these trusts along with relevant keywords: 1. Mecklenburg North Carolina Marital Deduction Trust (Trust A): The Mecklenburg North Carolina Marital Deduction Trust, also known as a TIP trust (Qualified Terminable Interest Property), is a type of trust designed to take advantage of the unlimited marital deduction for federal estate tax purposes. It allows one spouse to transfer assets to the trust, ensuring the surviving spouse receives income from it for their lifetime. The surviving spouse has limited access to the principal but receives income distributions. With this trust, the value of the assets in the trust is not included in the surviving spouse's estate upon their death, thereby reducing potential estate tax liabilities. Keywords: Marital deduction, TIP trust, unlimited marital deduction, federal estate tax, surviving spouse, income distributions, estate tax liabilities. 2. Bypass Trust (Trust B): The Bypass Trust, also known as an A/B trust or credit shelter trust, is another type of trust utilized by married couples to minimize estate taxes. When the first spouse dies, a portion of the deceased spouse's assets, up to the estate tax exemption amount, are placed in the Bypass Trust. This trust ensures that the exemption amount is effectively used, as it is not subject to estate taxes upon the surviving spouse's death. The remaining assets (above the exemption amount) pass to the Marital Deduction Trust. By splitting the assets between the Bypass Trust and the Marital Deduction Trust, the couple can take advantage of both spouses' estate tax exemptions, reducing the total estate tax due. Keywords: Bypass Trust, A/B trust, credit shelter trust, estate tax exemption, estate taxes, surviving spouse, Marital Deduction Trust, estate tax due. These two trusts, the Mecklenburg North Carolina Marital Deduction Trust — Trust A and Bypass Trust B, are commonly used in estate planning to help married couples minimize estate taxes and efficiently distribute their assets. Both trusts offer different mechanisms for asset protection and tax efficiency, depending on the specific circumstances and goals of the individuals. Estate planning professionals in Mecklenburg County can provide personalized guidance on whether these trusts are suitable for a particular situation and help their clients implement them effectively.