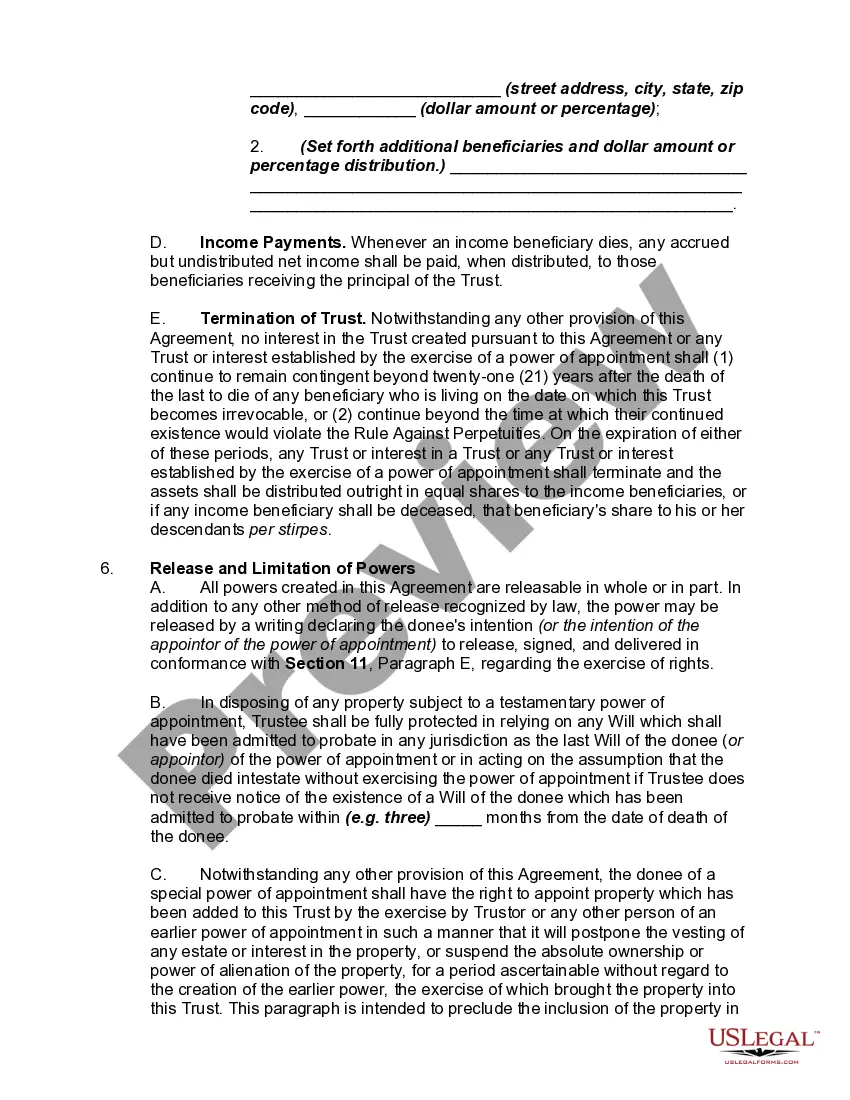

An A-B trust is a revocable living trust which divides into two trusts upon the death of the first spouse. This type of trust makes use of both the estate tax exemption ($3.5 million per person in 2009) and the marital deduction to make it so that no estate taxes are due upon the death of the first spouse. The B Trust is also known as the Bypass trust and it contains the amount of that years applicable exclusion amount. The A trust is the marital deduction trust which will typically contain both the surviving spouse's separate property and one half community property interests but also the residue of the deceased spouse's estate after the estate tax exemption has been utilized by the B trust. The use of an A-B trust ensures that both spouse's applicable exclusion amounts are effectively used, thereby doubling the amount of property which can pass to heirs free of Federal Estate Taxes.

Nassau New York Marital Deduction Trust, often referred to as Trust A, and Bypass Trust B are estate planning tools designed to assist married couples in maximizing their tax benefits and preserving assets for their beneficiaries. These trusts are commonly utilized in Nassau County, New York, and are known for their effectiveness in minimizing estate taxes. Trust A, or the Marital Deduction Trust, is created to take advantage of the unlimited marital deduction offered by the IRS. This deduction allows one spouse to transfer an unlimited amount of assets to the other spouse tax-free upon their death. By utilizing Trust A, the assets transferred are not part of the first spouse's taxable estate and can greatly reduce the overall estate tax liability. Bypass Trust B, also known as the Credit Shelter Trust or Family Trust, is created to make use of the deceased spouse's estate tax exemption. The estate tax exemption is the amount of assets an individual can pass on to their beneficiaries without incurring any estate tax. By placing assets in Trust B up to the value of their exemption, the deceased spouse effectively "bypasses" these assets from being included in their taxable estate. This ensures that the exemption is fully utilized, potentially saving a significant amount in estate taxes. Other types of Nassau New York Marital Deduction Trusts may include: 1. Qualified Terminable Interest Property (TIP) Trust: This trust provides income and support to a surviving spouse while ensuring that the principal is eventually distributed to other chosen beneficiaries, such as children from a previous marriage. 2. Qualified Personnel Residence Trust (PRT): This trust allows a couple to transfer their primary residence or vacation home into an irrevocable trust while continuing to use the property for a specified period. This strategy helps reduce the value of the estate and minimizes potential estate tax liability. 3. Charitable Remainder Trust (CRT): A CRT enables a spouse to transfer assets into a trust that provides income to the surviving spouse during their lifetime. After the surviving spouse's death, the remaining assets are distributed to charitable beneficiaries, resulting in potential estate tax benefits. In summary, Nassau New York Marital Deduction Trust — Trust A and Bypass Trust B are two important estate planning tools that provide tax advantages for married couples. By leveraging these trusts, individuals can potentially minimize estate taxes and ensure their assets are passed on to their chosen beneficiaries efficiently. Variations of these trusts, such as TIP Trusts, Parts, and CRTs, may be considered based on individual circumstances and preferences.Nassau New York Marital Deduction Trust, often referred to as Trust A, and Bypass Trust B are estate planning tools designed to assist married couples in maximizing their tax benefits and preserving assets for their beneficiaries. These trusts are commonly utilized in Nassau County, New York, and are known for their effectiveness in minimizing estate taxes. Trust A, or the Marital Deduction Trust, is created to take advantage of the unlimited marital deduction offered by the IRS. This deduction allows one spouse to transfer an unlimited amount of assets to the other spouse tax-free upon their death. By utilizing Trust A, the assets transferred are not part of the first spouse's taxable estate and can greatly reduce the overall estate tax liability. Bypass Trust B, also known as the Credit Shelter Trust or Family Trust, is created to make use of the deceased spouse's estate tax exemption. The estate tax exemption is the amount of assets an individual can pass on to their beneficiaries without incurring any estate tax. By placing assets in Trust B up to the value of their exemption, the deceased spouse effectively "bypasses" these assets from being included in their taxable estate. This ensures that the exemption is fully utilized, potentially saving a significant amount in estate taxes. Other types of Nassau New York Marital Deduction Trusts may include: 1. Qualified Terminable Interest Property (TIP) Trust: This trust provides income and support to a surviving spouse while ensuring that the principal is eventually distributed to other chosen beneficiaries, such as children from a previous marriage. 2. Qualified Personnel Residence Trust (PRT): This trust allows a couple to transfer their primary residence or vacation home into an irrevocable trust while continuing to use the property for a specified period. This strategy helps reduce the value of the estate and minimizes potential estate tax liability. 3. Charitable Remainder Trust (CRT): A CRT enables a spouse to transfer assets into a trust that provides income to the surviving spouse during their lifetime. After the surviving spouse's death, the remaining assets are distributed to charitable beneficiaries, resulting in potential estate tax benefits. In summary, Nassau New York Marital Deduction Trust — Trust A and Bypass Trust B are two important estate planning tools that provide tax advantages for married couples. By leveraging these trusts, individuals can potentially minimize estate taxes and ensure their assets are passed on to their chosen beneficiaries efficiently. Variations of these trusts, such as TIP Trusts, Parts, and CRTs, may be considered based on individual circumstances and preferences.