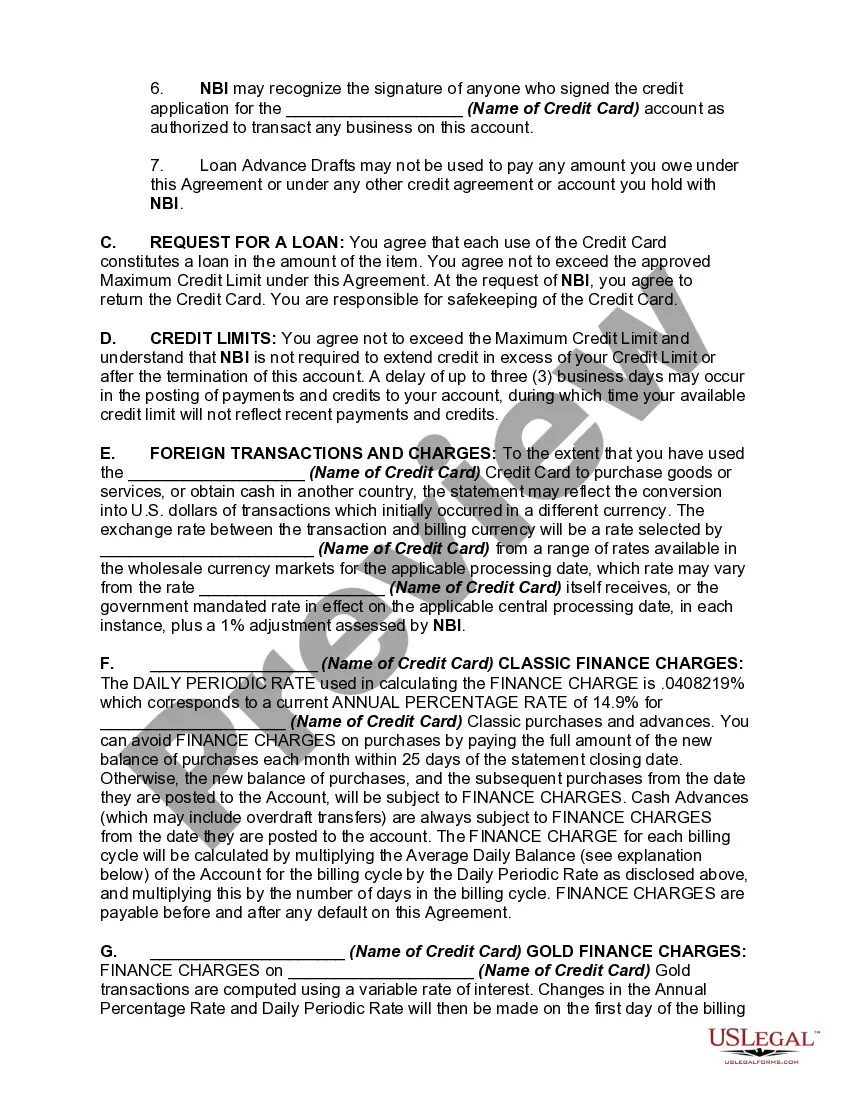

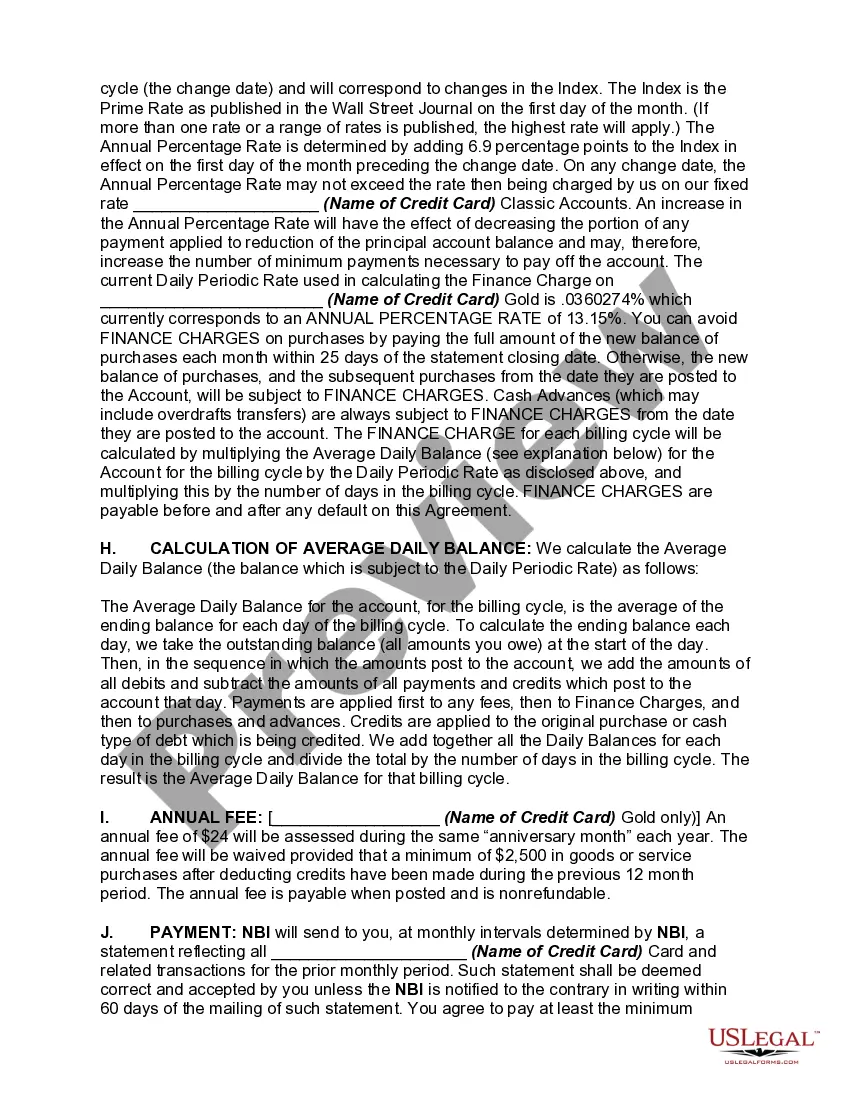

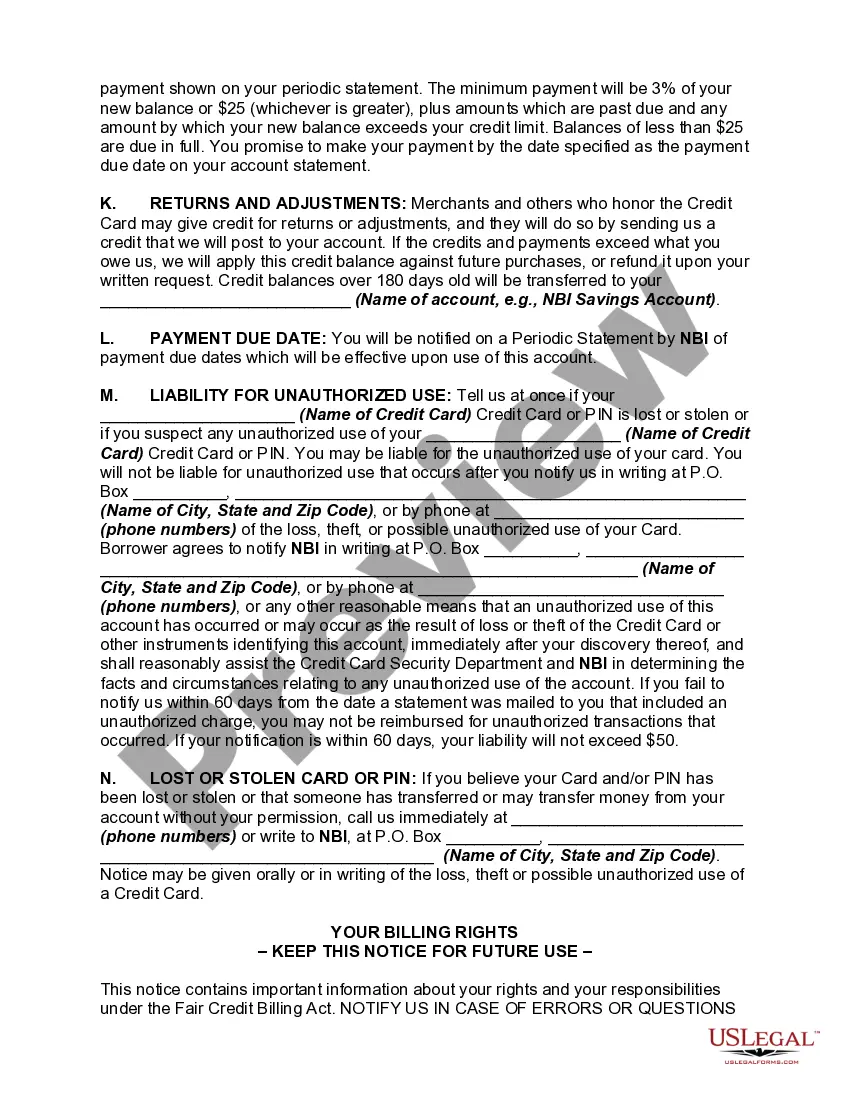

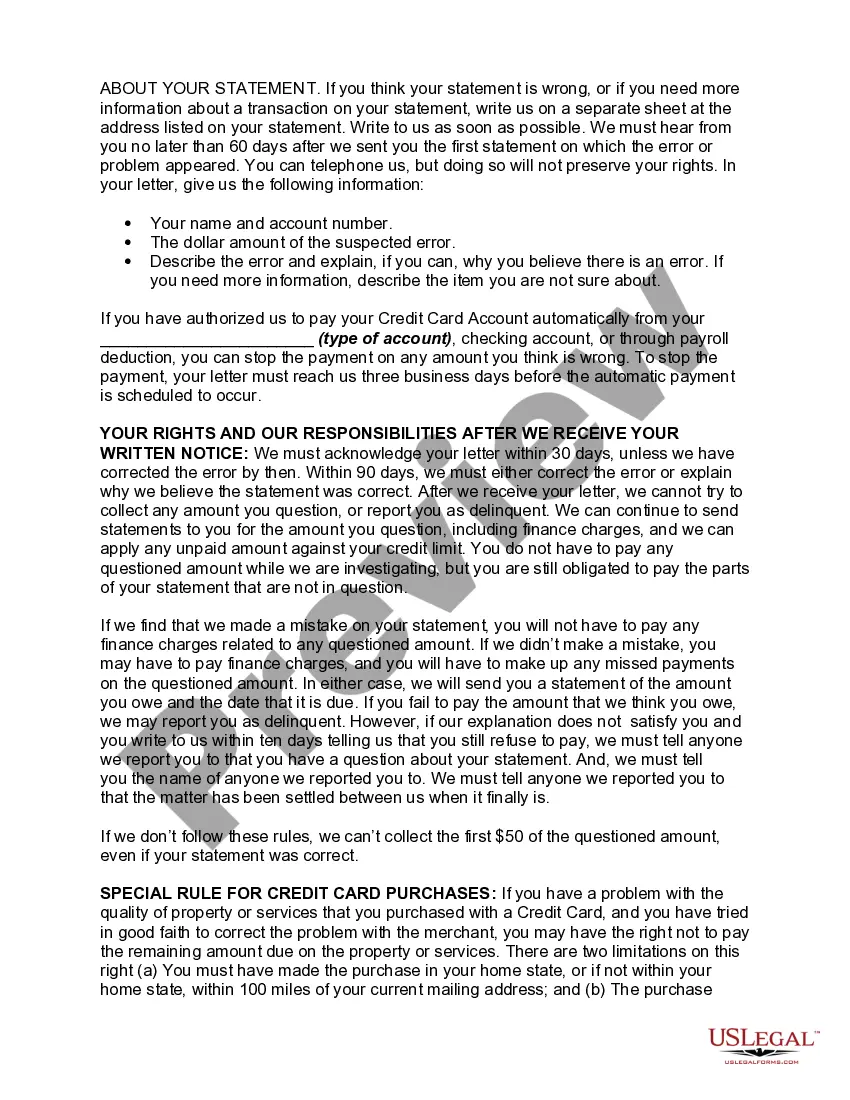

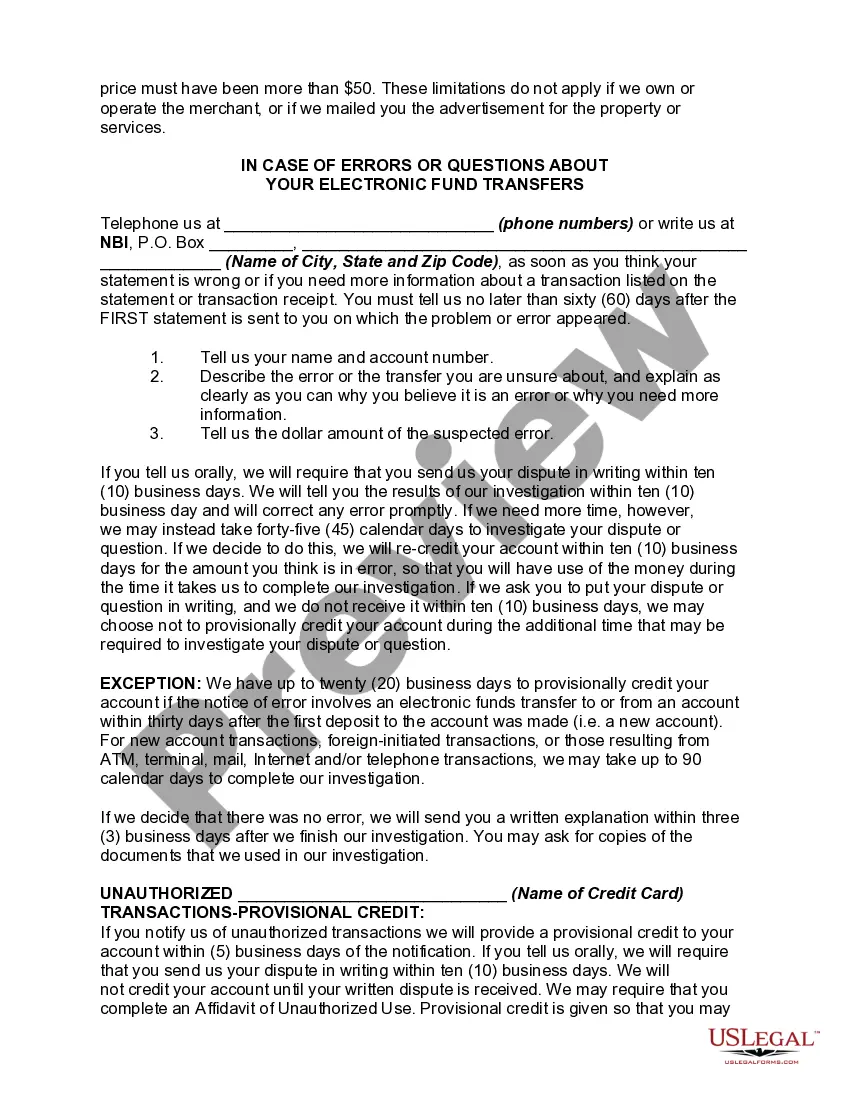

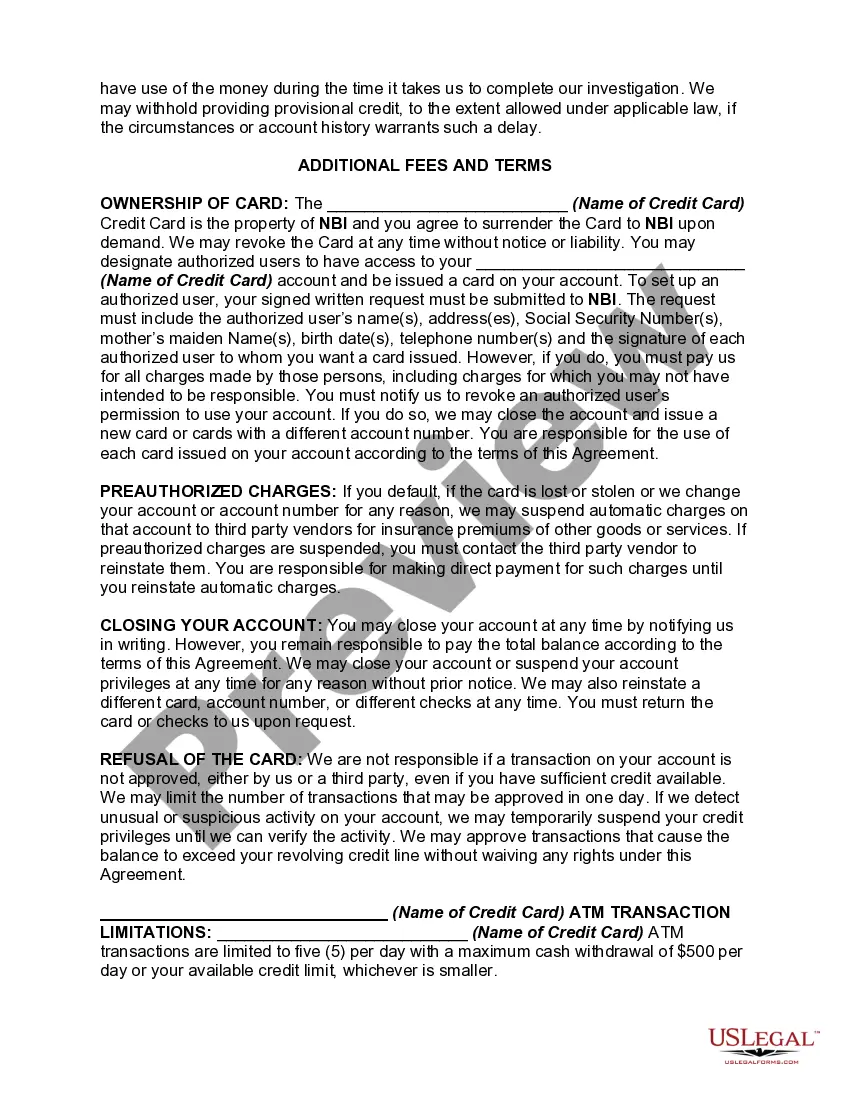

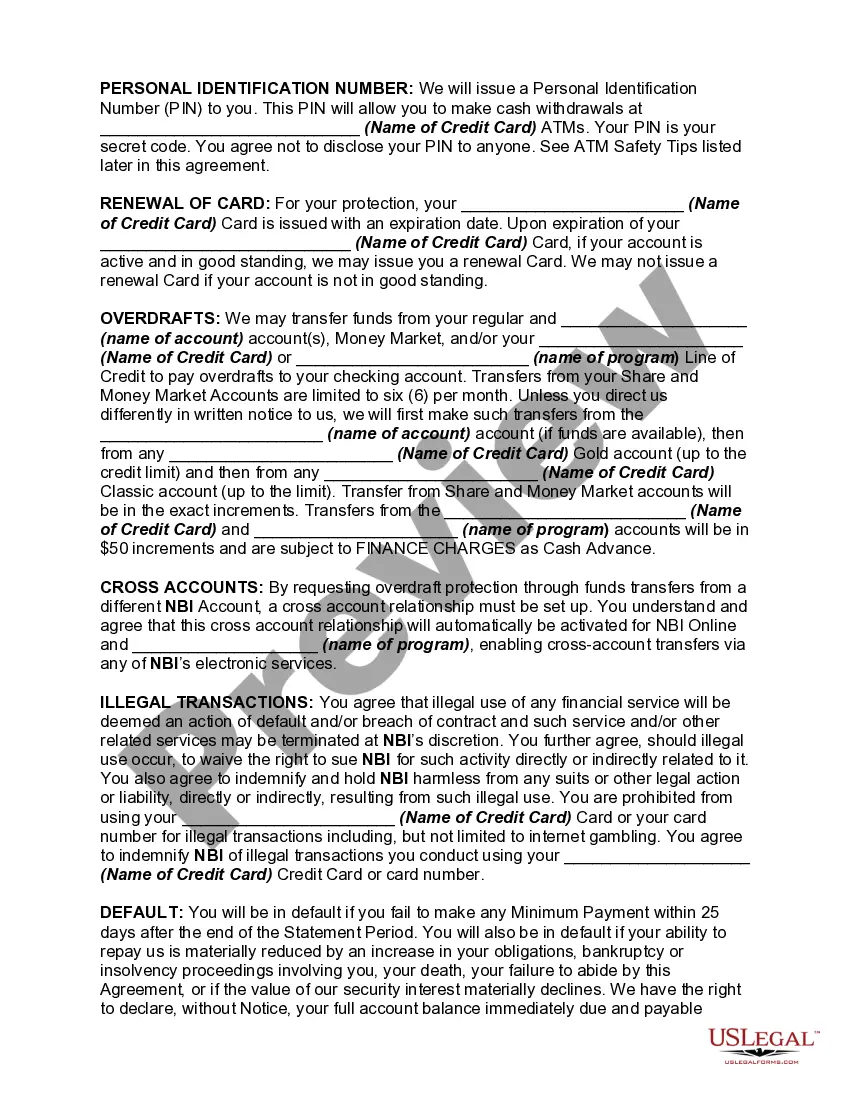

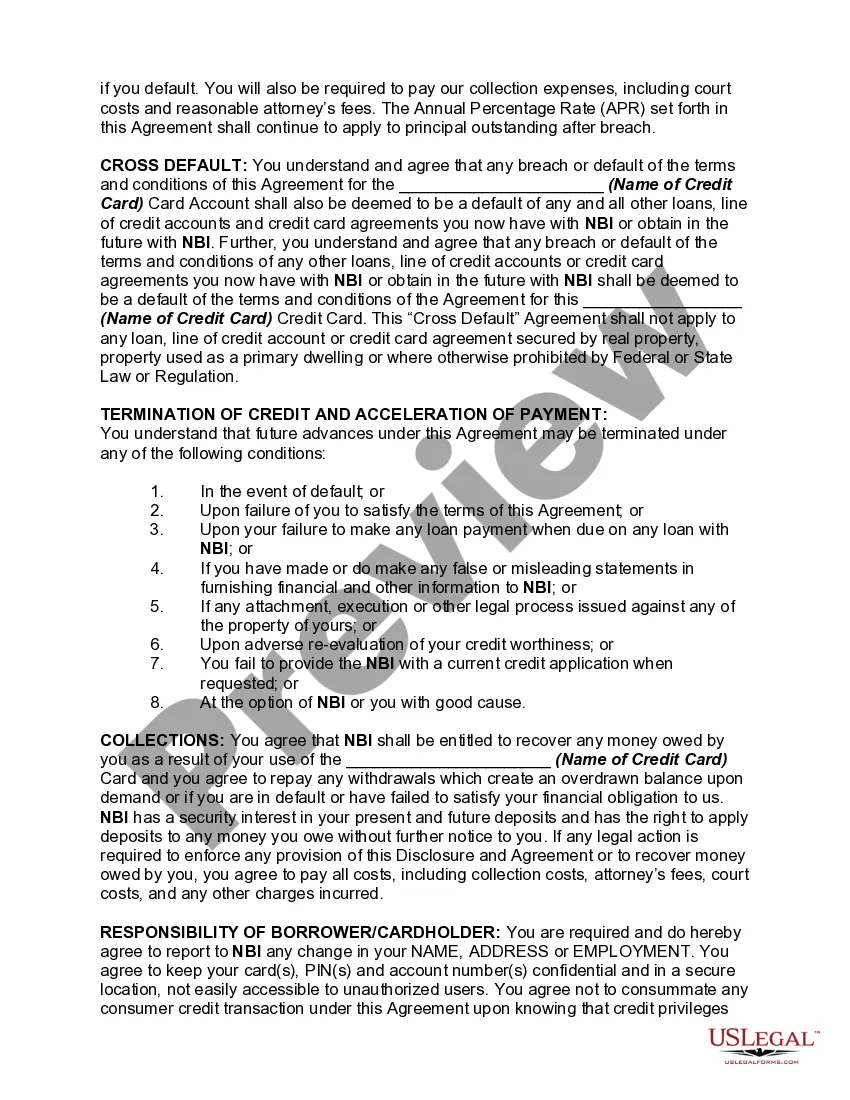

The Alameda California Credit Card Agreement and Disclosure Statement is a legal document that outlines the terms and conditions of a credit card issued by financial institutions in Alameda, California. This agreement serves as a binding contract between the credit card issuer and the cardholder, providing important information regarding the card's usage, fees, interest rates, and other important aspects. It is crucial for individuals to review and understand this document before applying for or using a credit card to avoid any confusion or potential disputes. The Alameda California Credit Card Agreement and Disclosure Statement typically contains various sections, including: 1. Definitions: This section clarifies the terms used throughout the document, ensuring both parties are on the same page. 2. Annual Percentage Rates (APR): It specifies the interest rate charged on outstanding balances, as well as the different APR's for purchases, cash advances, balance transfers, and penalty rates. 3. Fees and Charges: This section outlines the fees associated with using the credit card, such as annual fees, late payment fees, over-limit fees, and cash advance fees. 4. Payment Terms: This section explains the minimum payment requirements, due dates, and any penalties for missed or late payments. 5. Credit Limit: It specifies the maximum amount of credit extended to the cardholder and the criteria used to determine credit limit increases or decreases. 6. Billing Statements: This section clarifies the frequency of billing statements and provides details on how to dispute any errors or inaccuracies. 7. Rewards and Benefits: If applicable, this section outlines any reward programs, perks, or promotional offers associated with the credit card. 8. Liability and Fraud Protection: This section explains the cardholder's responsibilities in case of loss, theft, or unauthorized use of the credit card, as well as the issuer's liability policy. 9. Termination: This outlines the conditions under which either party can terminate the agreement, including reasons such as non-payment, default, or violation of terms. It is important to note that different credit card issuers may have variations in their specific Alameda California Credit Card Agreement and Disclosure Statement, tailored to their respective credit card products. For instance, there may be variations in terms of penalty rates, grace periods, prepayment penalties, or other specific details. Therefore, it is vital for cardholders to carefully review the agreement provided by their specific credit card issuer to ensure full comprehension of the terms and conditions.

Alameda California Credit Card Agreement and Disclosure Statement

Description

How to fill out Alameda California Credit Card Agreement And Disclosure Statement?

Preparing papers for the business or individual needs is always a huge responsibility. When drawing up a contract, a public service request, or a power of attorney, it's essential to take into account all federal and state laws of the particular area. Nevertheless, small counties and even cities also have legislative provisions that you need to consider. All these aspects make it burdensome and time-consuming to create Alameda Credit Card Agreement and Disclosure Statement without professional assistance.

It's possible to avoid wasting money on attorneys drafting your paperwork and create a legally valid Alameda Credit Card Agreement and Disclosure Statement by yourself, using the US Legal Forms web library. It is the biggest online collection of state-specific legal documents that are professionally verified, so you can be certain of their validity when choosing a sample for your county. Previously subscribed users only need to log in to their accounts to save the needed form.

In case you still don't have a subscription, adhere to the step-by-step guideline below to obtain the Alameda Credit Card Agreement and Disclosure Statement:

- Look through the page you've opened and verify if it has the document you require.

- To achieve this, use the form description and preview if these options are presented.

- To locate the one that satisfies your needs, use the search tab in the page header.

- Recheck that the sample complies with juridical standards and click Buy Now.

- Pick the subscription plan, then sign in or register for an account with the US Legal Forms.

- Utilize your credit card or PayPal account to pay for your subscription.

- Download the selected document in the preferred format, print it, or fill it out electronically.

The exceptional thing about the US Legal Forms library is that all the paperwork you've ever purchased never gets lost - you can get it in your profile within the My Forms tab at any time. Join the platform and quickly obtain verified legal forms for any use case with just a couple of clicks!