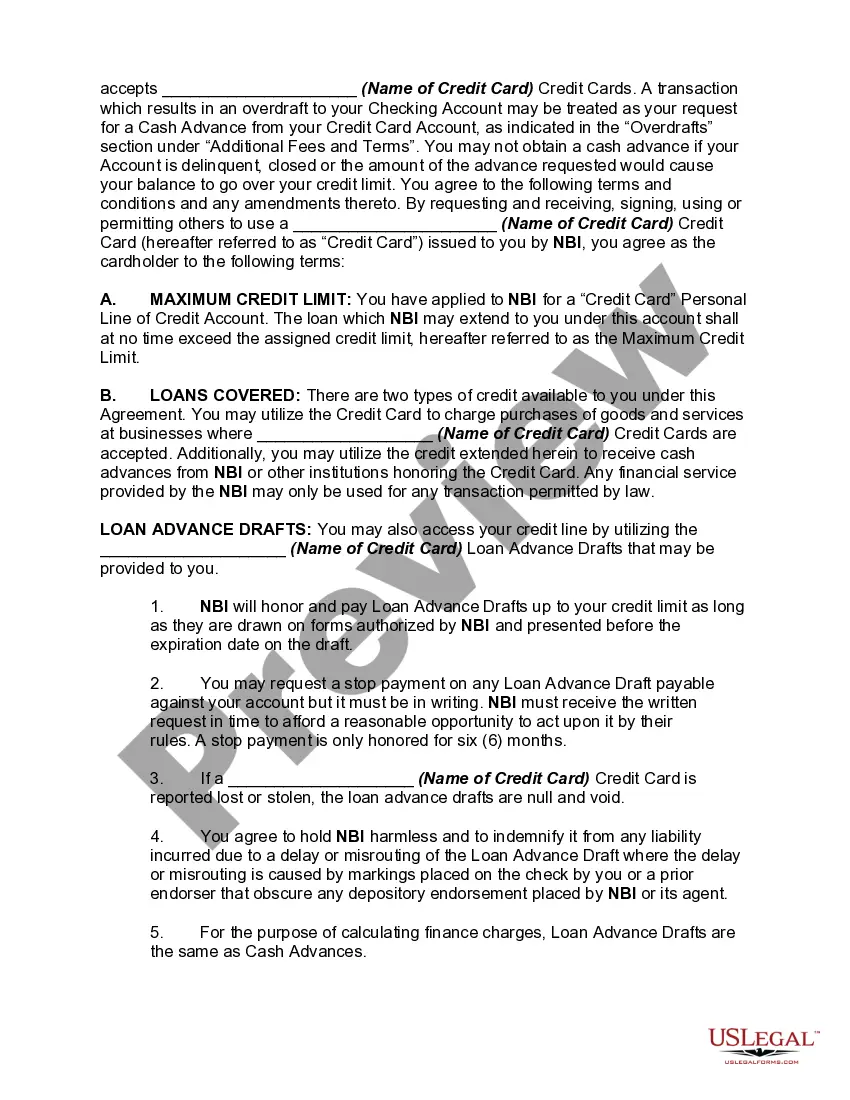

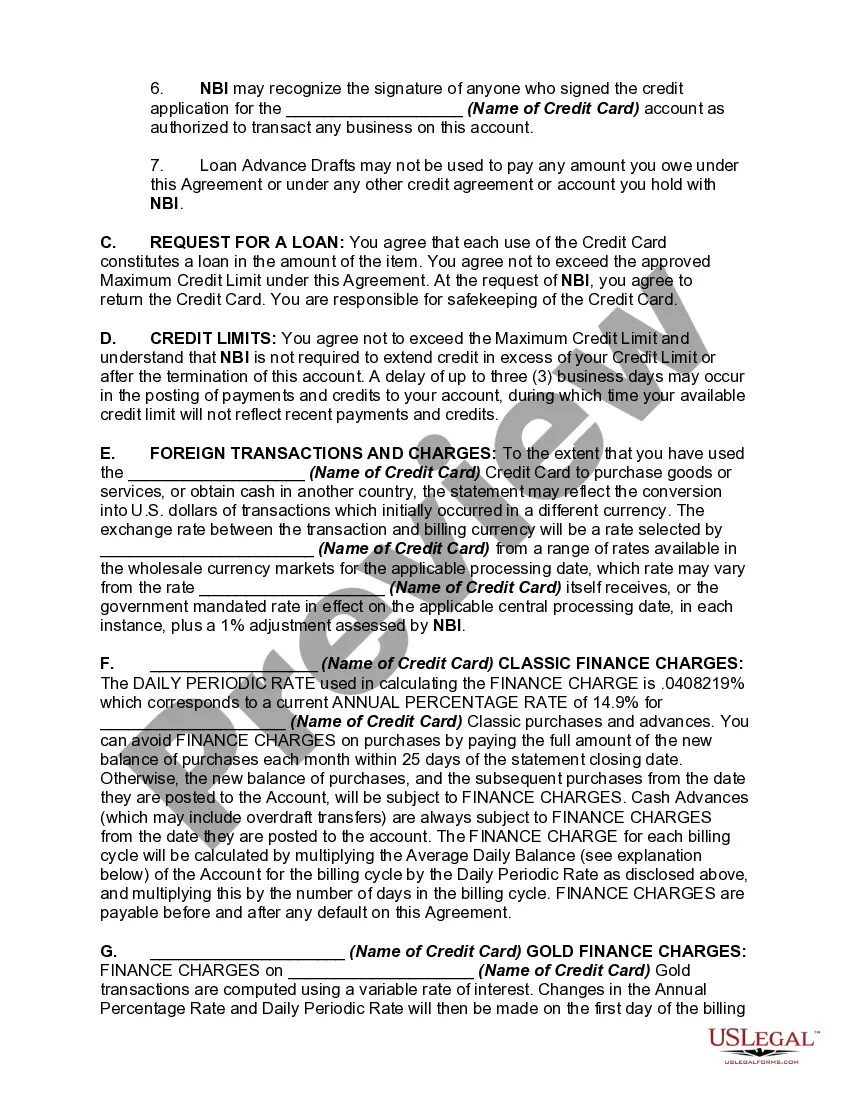

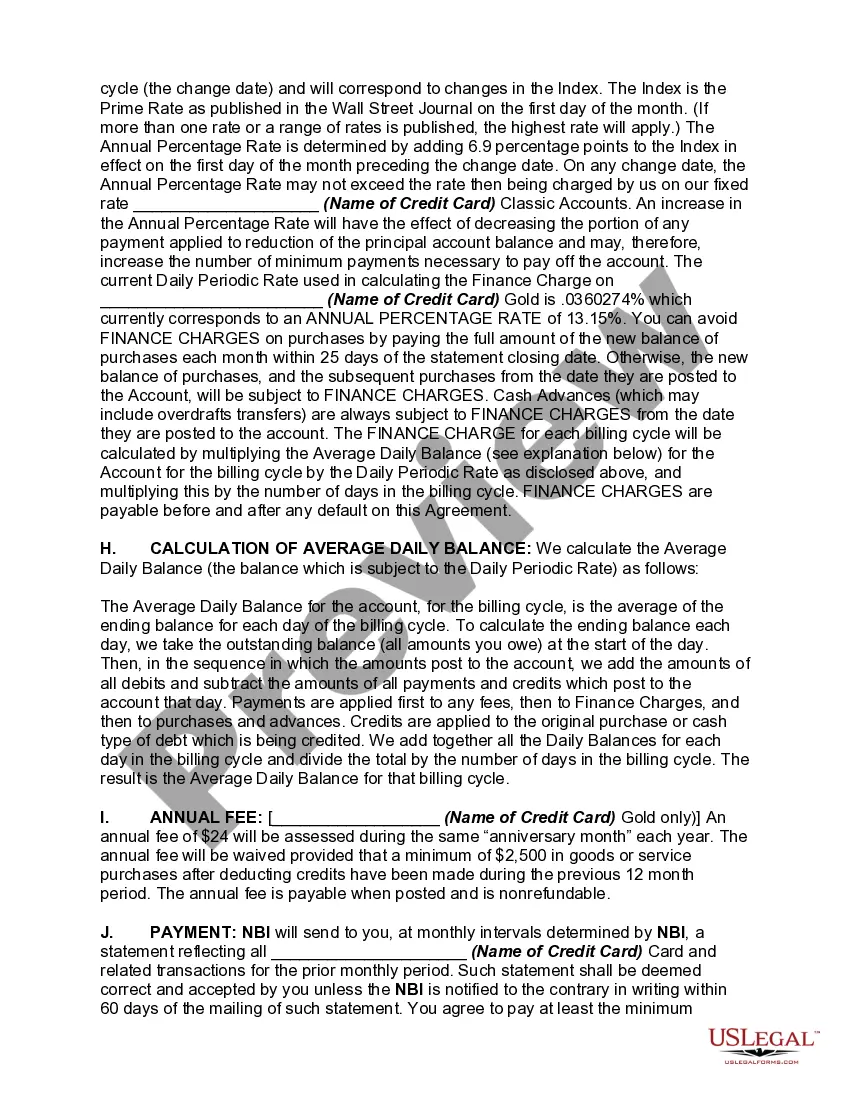

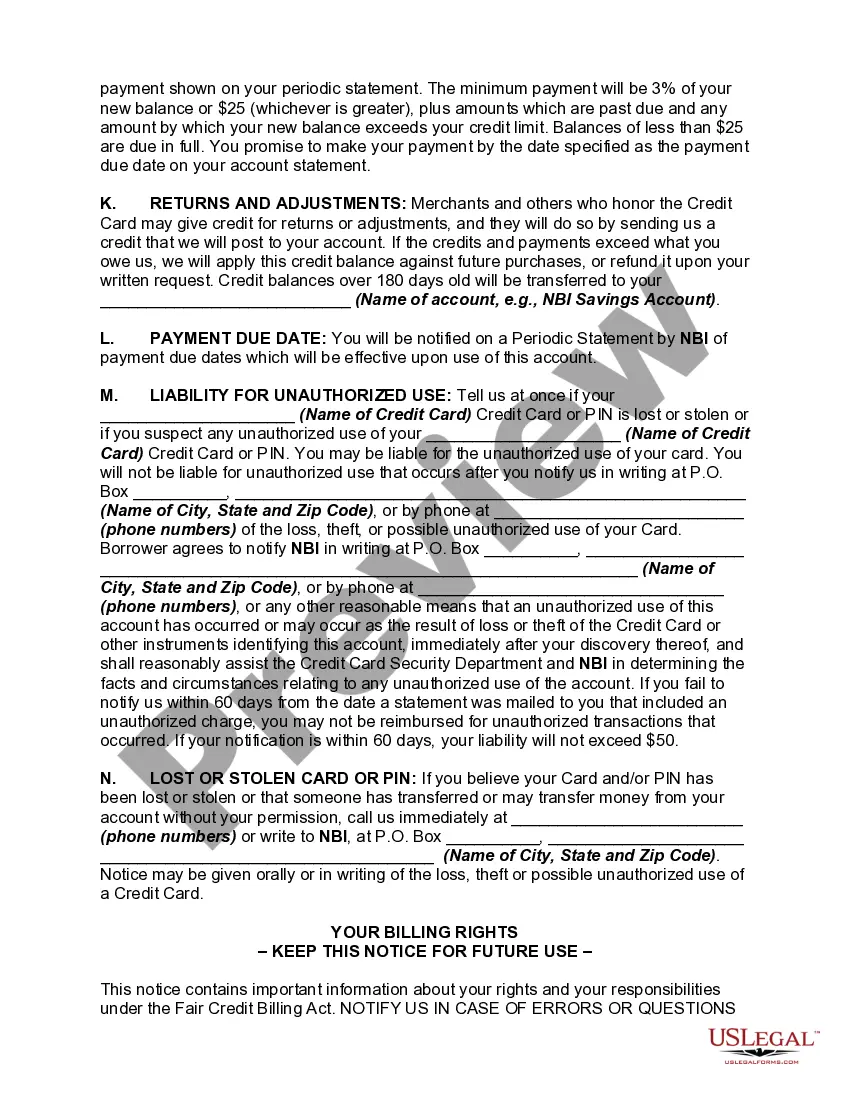

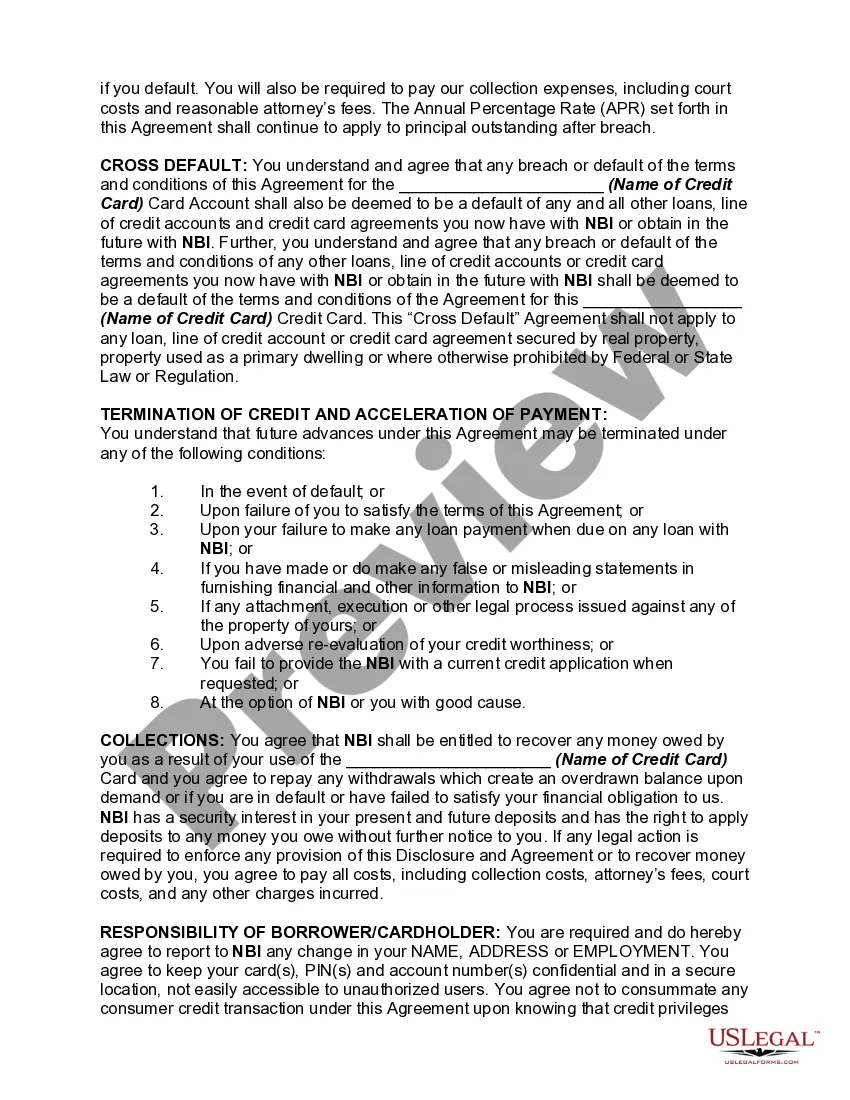

Oakland Michigan Credit Card Agreement and Disclosure Statement is an important legal document that outlines the terms and conditions of using credit cards issued by financial institutions operating in Oakland, Michigan. These agreements are designed to protect both the credit card issuer and the cardholder by clearly defining their rights and responsibilities. The Oakland Michigan Credit Card Agreement and Disclosure Statement typically covers various aspects related to credit card usage, including interest rates, fees, payment terms, credit limits, dispute resolution procedures, and important legal disclosures. It is crucial for cardholders to carefully review and understand these terms before using their credit cards to avoid any misunderstandings or potential financial liabilities. While the specific terms and conditions may differ among different financial institutions, the Oakland Michigan Credit Card Agreements and Disclosure Statements generally share common elements. Some essential keywords that may be found within these agreements include: 1. Interest Rates: This section outlines the interest rates charged on outstanding balances and any applicable promotional rates for balance transfers or cash advances. It may also specify how and when interest rates may change. 2. Fees: This section enumerates various fees associated with credit card usage, such as annual fees, late payment fees, over-limit fees, foreign transaction fees, and cash advance fees. 3. Payment Terms: This section includes information about minimum payment requirements, due dates, and acceptable payment methods. It may also disclose how payments are applied to different balances, such as purchases, balance transfers, or cash advances. 4. Credit Limit: This segment outlines the maximum amount of credit available to the cardholder. It may specify that the credit limit is subject to change based on factors like creditworthiness and account activity. 5. Billing Statements: This section explains how and when the credit card issuer will provide monthly billing statements, either electronically or via mail. It may also clarify the required actions if the cardholder notices any discrepancies or unauthorized charges on the statement. 6. Dispute Resolution: This part outlines the process for resolving disputes or discrepancies between the cardholder and the credit card issuer. It may describe how to file a formal complaint and the subsequent steps involved. 7. Legal Disclosures: This segment includes important legal information, such as the cardholder's liability for unauthorized charges, the right to opt-out of certain marketing communications, and any special disclosures required by state or federal laws. It is important to note that different financial institutions may have their own credit card agreements and disclosure statements, so it's advisable to review the specific terms and conditions of a particular institution before applying for or using their credit card. By understanding and adhering to the terms laid out in the Oakland Michigan Credit Card Agreement and Disclosure Statement, cardholders can navigate their credit card usage responsibly and avoid any potential pitfalls or misunderstandings.

Oakland Michigan Credit Card Agreement and Disclosure Statement

Description

How to fill out Oakland Michigan Credit Card Agreement And Disclosure Statement?

Drafting paperwork for the business or individual demands is always a huge responsibility. When creating a contract, a public service request, or a power of attorney, it's essential to take into account all federal and state laws and regulations of the particular area. Nevertheless, small counties and even cities also have legislative provisions that you need to consider. All these aspects make it stressful and time-consuming to generate Oakland Credit Card Agreement and Disclosure Statement without expert help.

It's easy to avoid wasting money on attorneys drafting your documentation and create a legally valid Oakland Credit Card Agreement and Disclosure Statement by yourself, using the US Legal Forms online library. It is the most extensive online catalog of state-specific legal documents that are professionally verified, so you can be sure of their validity when choosing a sample for your county. Earlier subscribed users only need to log in to their accounts to download the necessary form.

In case you still don't have a subscription, follow the step-by-step guide below to get the Oakland Credit Card Agreement and Disclosure Statement:

- Look through the page you've opened and verify if it has the document you need.

- To accomplish this, use the form description and preview if these options are presented.

- To locate the one that fits your requirements, utilize the search tab in the page header.

- Double-check that the template complies with juridical standards and click Buy Now.

- Select the subscription plan, then log in or register for an account with the US Legal Forms.

- Use your credit card or PayPal account to pay for your subscription.

- Download the selected document in the preferred format, print it, or fill it out electronically.

The exceptional thing about the US Legal Forms library is that all the documentation you've ever obtained never gets lost - you can access it in your profile within the My Forms tab at any time. Join the platform and easily obtain verified legal forms for any situation with just a couple of clicks!