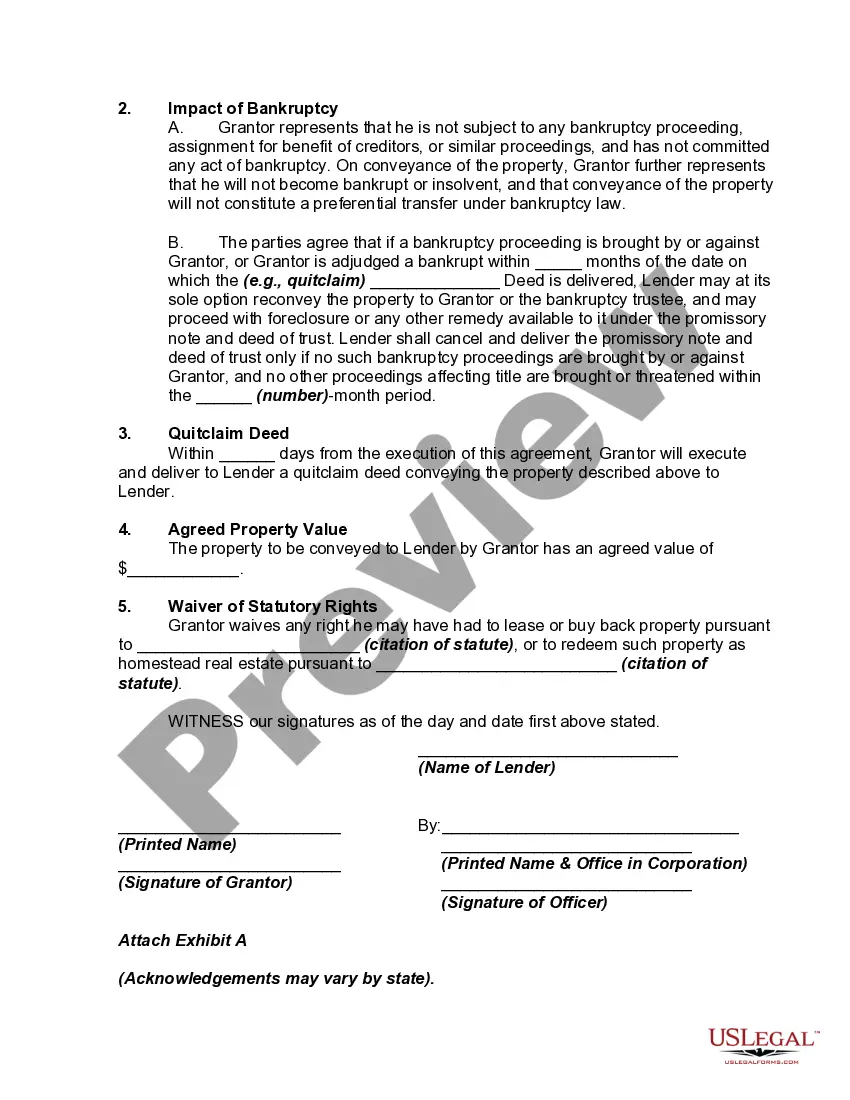

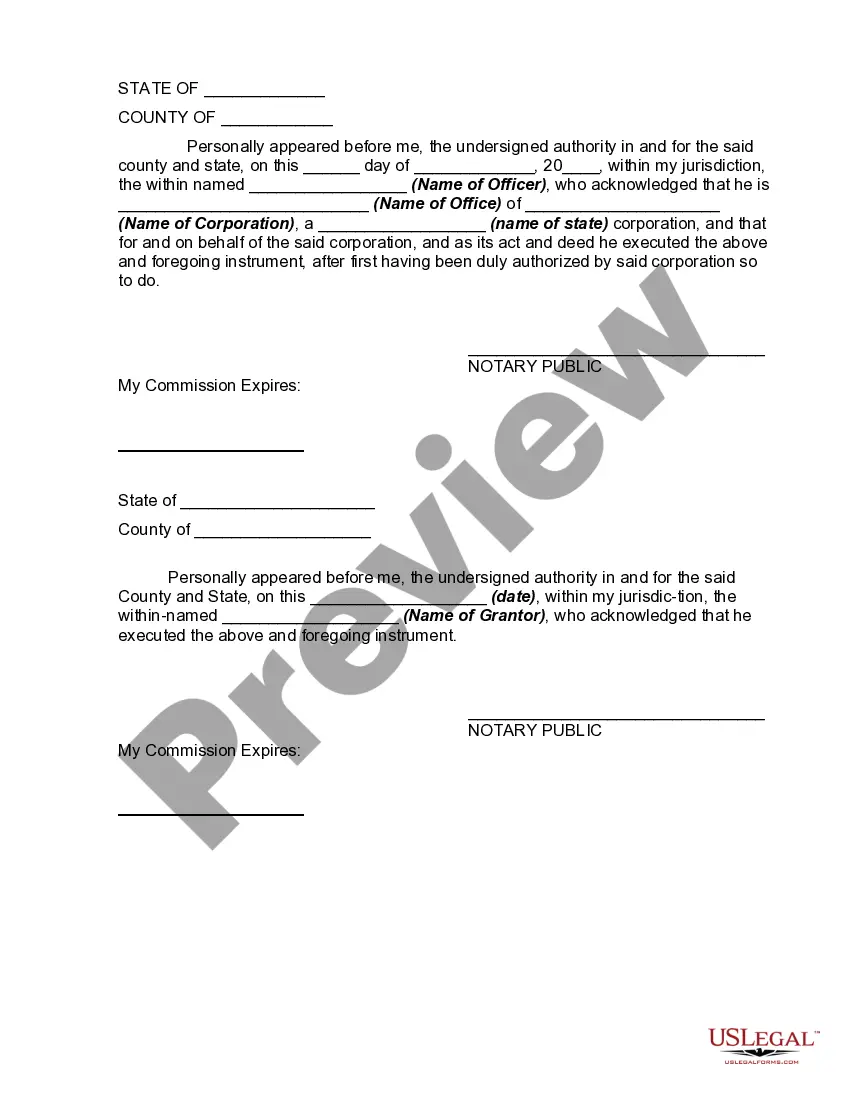

Lima Arizona conveyance of deed to lender in lieu of foreclosure is a legal process where a borrower transfers ownership of their property to the lender to avoid foreclosure. This arrangement, also known as a deed in lieu of foreclosure, can be a viable option for borrowers who are unable to meet their mortgage obligations. In Lima, Arizona, there are different types of conveyance of deed to lender in lieu of foreclosure, including: 1. Traditional Conveyance: This is the standard process where the borrower voluntarily offers the deed to the lender, usually with the intention of satisfying their outstanding loan balance. It is important to note that the lender must agree to accept the deed, and any remaining debt may be forgiven or become the borrower's responsibility depending on the negotiated terms. 2. Deed in Lieu with Cash for Keys: In this scenario, the lender may offer the borrower a cash incentive to vacate the property and leave it in good condition. This arrangement provides financial assistance to the borrower while allowing the lender to avoid the potentially costly and lengthy foreclosure process. 3. Assumption of Liabilities: With this type of conveyance, the borrower transfers the property's ownership to the lender and also assumes responsibility for certain liabilities, such as unpaid taxes or outstanding HOA fees. This option may be suitable for borrowers who are willing to bear some financial burden to expedite the process. 4. Partial Release of Liability: In some cases, the lender and borrower may agree to a partial release of liability, where the borrower transfers the deed for only a portion of the property, such as a specific parcel or an individual residential unit. This arrangement allows the borrower to retain ownership of a portion of their property while relieving the lender of responsibility for the conveyed portion. The conveyance of deed to lender in lieu of foreclosure offers a potential solution for distressed borrowers facing financial challenges in Lima, Arizona. However, it is crucial for borrowers to consult with legal and financial professionals to understand the implications and negotiate favorable terms. This process can help borrowers avoid more detrimental consequences typically associated with foreclosure and provide lenders with an alternative method to mitigate losses.

Pima Arizona Conveyance of Deed to Lender in Lieu of Foreclosure

Description

How to fill out Pima Arizona Conveyance Of Deed To Lender In Lieu Of Foreclosure?

Are you looking to quickly draft a legally-binding Pima Conveyance of Deed to Lender in Lieu of Foreclosure or probably any other document to take control of your own or corporate matters? You can go with two options: contact a legal advisor to draft a valid document for you or draft it completely on your own. The good news is, there's an alternative solution - US Legal Forms. It will help you get professionally written legal documents without having to pay unreasonable fees for legal services.

US Legal Forms offers a rich collection of over 85,000 state-compliant document templates, including Pima Conveyance of Deed to Lender in Lieu of Foreclosure and form packages. We offer documents for an array of life circumstances: from divorce papers to real estate document templates. We've been on the market for more than 25 years and got a rock-solid reputation among our clients. Here's how you can become one of them and get the necessary document without extra hassles.

- First and foremost, double-check if the Pima Conveyance of Deed to Lender in Lieu of Foreclosure is adapted to your state's or county's regulations.

- If the document includes a desciption, make sure to verify what it's suitable for.

- Start the searching process over if the template isn’t what you were hoping to find by utilizing the search bar in the header.

- Select the subscription that best suits your needs and move forward to the payment.

- Select the format you would like to get your document in and download it.

- Print it out, complete it, and sign on the dotted line.

If you've already registered an account, you can easily log in to it, locate the Pima Conveyance of Deed to Lender in Lieu of Foreclosure template, and download it. To re-download the form, simply head to the My Forms tab.

It's effortless to buy and download legal forms if you use our catalog. In addition, the paperwork we offer are reviewed by industry experts, which gives you greater peace of mind when dealing with legal matters. Try US Legal Forms now and see for yourself!