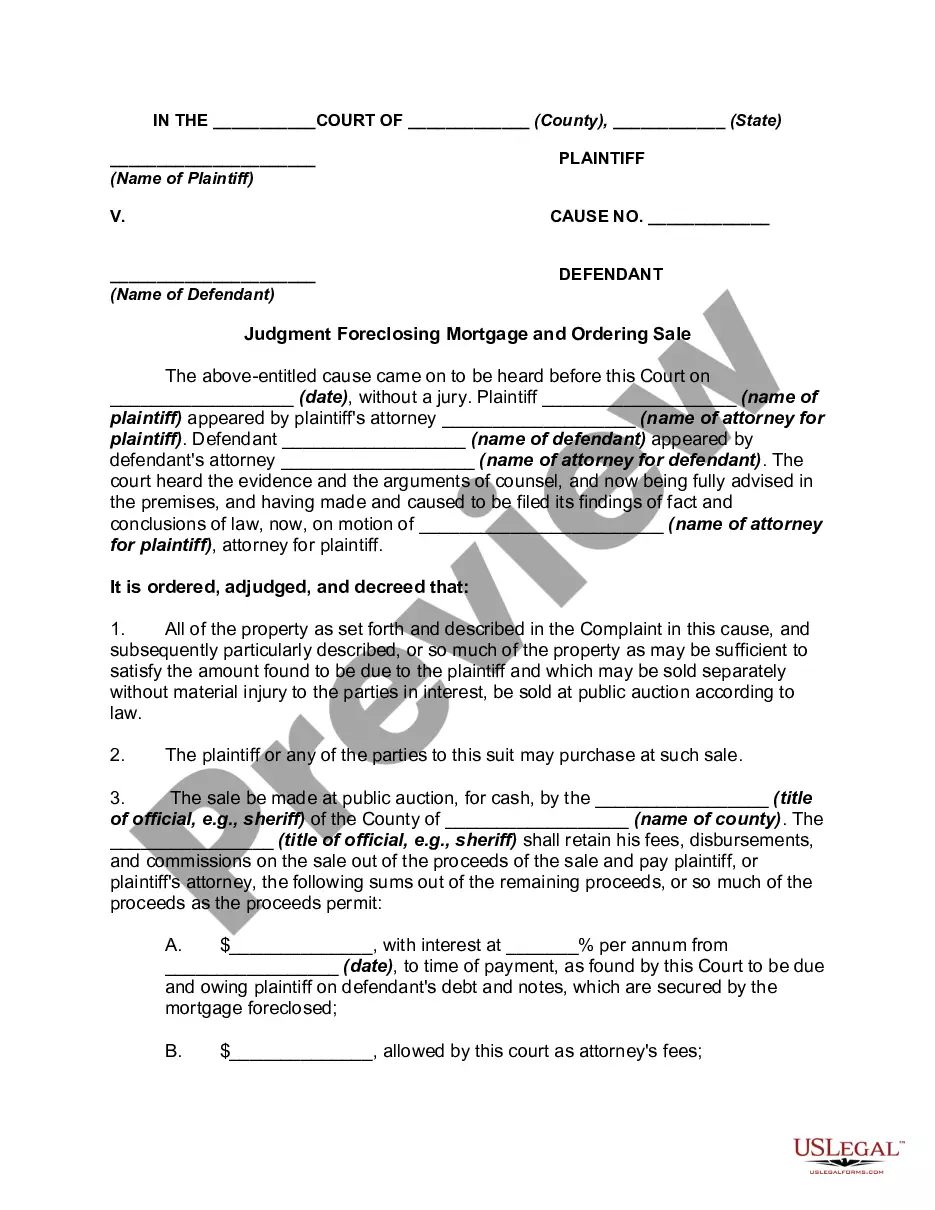

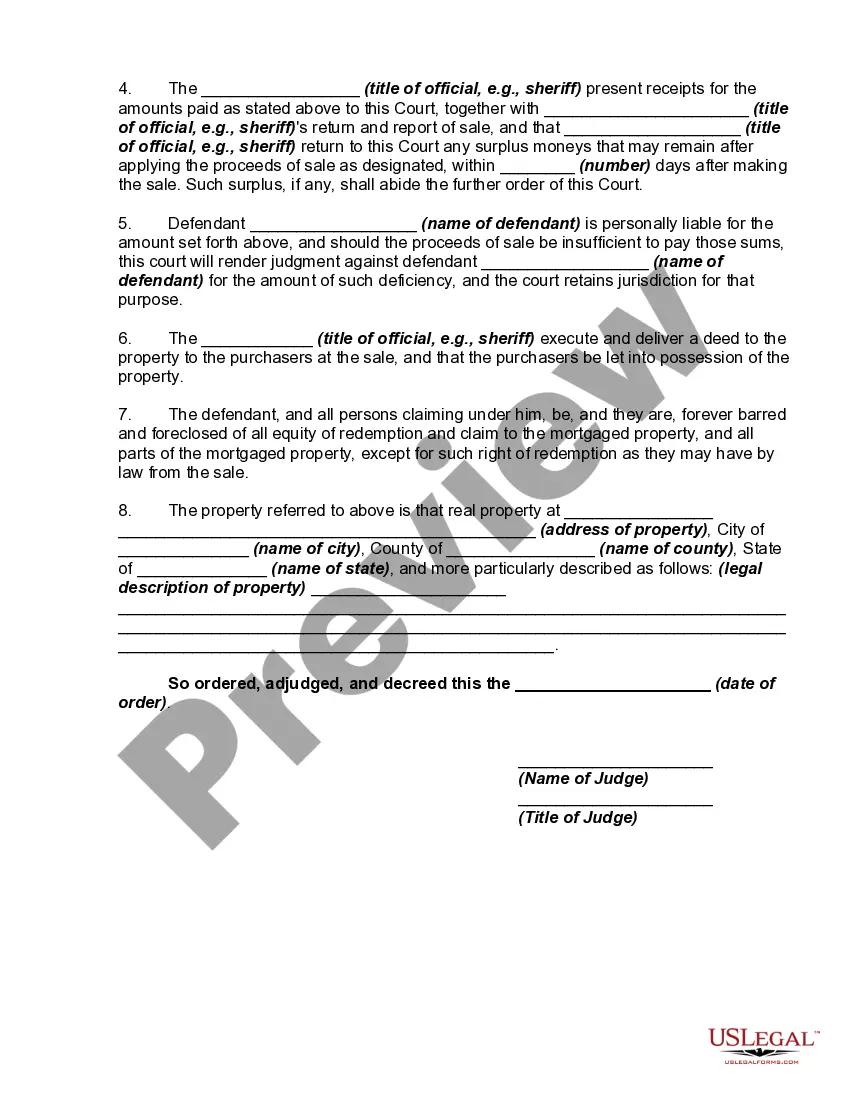

Bexar Texas Judgment Foreclosing Mortgage and Ordering Sale is a legal process initiated by a lender or mortgage holder to enforce their right to foreclose on a property due to delinquent mortgage payments. This legal action is taken when the borrower fails to honor their financial obligations in accordance with the terms and conditions of the mortgage agreement. In Bexar County, Texas, a judgment of foreclosure is obtained through a lawsuit filed by the mortgage holder or a representative. The court examines the evidence presented, including the mortgage agreement and the borrower's payment history, and if it determines that the borrower has defaulted on their payments, a judgment will be issued against them. This judgment allows the lender to initiate the foreclosure process and seek a sale of the property to recover the outstanding loan balance. There are different types of Bexar Texas Judgment Foreclosing Mortgage and Ordering Sale, including: 1. Judicial Foreclosure: This type of foreclosure involves a court proceeding in which the lender files a lawsuit against the borrower to obtain a judgment. The court then orders the sale of the property to satisfy the outstanding debt. 2. Non-judicial Foreclosure: In some cases, the mortgage agreement may include a power of sale clause, which allows the lender to foreclose on the property without court involvement. A Notice of Sale is issued, and the property is sold at a public auction to repay the debt. 3. Deficiency Judgment: If the sale of the foreclosed property does not generate enough funds to cover the outstanding loan balance, the lender may seek a deficiency judgment against the borrower. This judgment allows the lender to pursue the borrower for the remaining debt through other means, such as wage garnishment or seizing other assets. It is essential for borrowers facing the possibility of a Bexar Texas Judgment Foreclosing Mortgage and Ordering Sale to consult with legal counsel to understand their rights and options. They may be able to negotiate alternatives, such as loan modifications, short sales, or deeds in lieu of foreclosure. However, if the foreclosure process proceeds, it is crucial for the borrower to comply with court orders and seek professional advice to protect their interests.

Bexar Texas Judgment Foreclosing Mortgage and Ordering Sale

Description

How to fill out Bexar Texas Judgment Foreclosing Mortgage And Ordering Sale?

Preparing legal paperwork can be burdensome. Besides, if you decide to ask a legal professional to write a commercial agreement, papers for ownership transfer, pre-marital agreement, divorce paperwork, or the Bexar Judgment Foreclosing Mortgage and Ordering Sale, it may cost you a lot of money. So what is the most reasonable way to save time and money and draft legitimate documents in total compliance with your state and local laws and regulations? US Legal Forms is a great solution, whether you're searching for templates for your personal or business needs.

US Legal Forms is biggest online library of state-specific legal documents, providing users with the up-to-date and professionally verified forms for any scenario collected all in one place. Consequently, if you need the recent version of the Bexar Judgment Foreclosing Mortgage and Ordering Sale, you can easily find it on our platform. Obtaining the papers requires a minimum of time. Those who already have an account should check their subscription to be valid, log in, and pick the sample using the Download button. If you haven't subscribed yet, here's how you can get the Bexar Judgment Foreclosing Mortgage and Ordering Sale:

- Look through the page and verify there is a sample for your region.

- Check the form description and use the Preview option, if available, to make sure it's the sample you need.

- Don't worry if the form doesn't satisfy your requirements - search for the right one in the header.

- Click Buy Now when you find the required sample and pick the best suitable subscription.

- Log in or register for an account to pay for your subscription.

- Make a payment with a credit card or through PayPal.

- Choose the file format for your Bexar Judgment Foreclosing Mortgage and Ordering Sale and save it.

When finished, you can print it out and complete it on paper or import the template to an online editor for a faster and more practical fill-out. US Legal Forms enables you to use all the paperwork ever acquired many times - you can find your templates in the My Forms tab in your profile. Give it a try now!