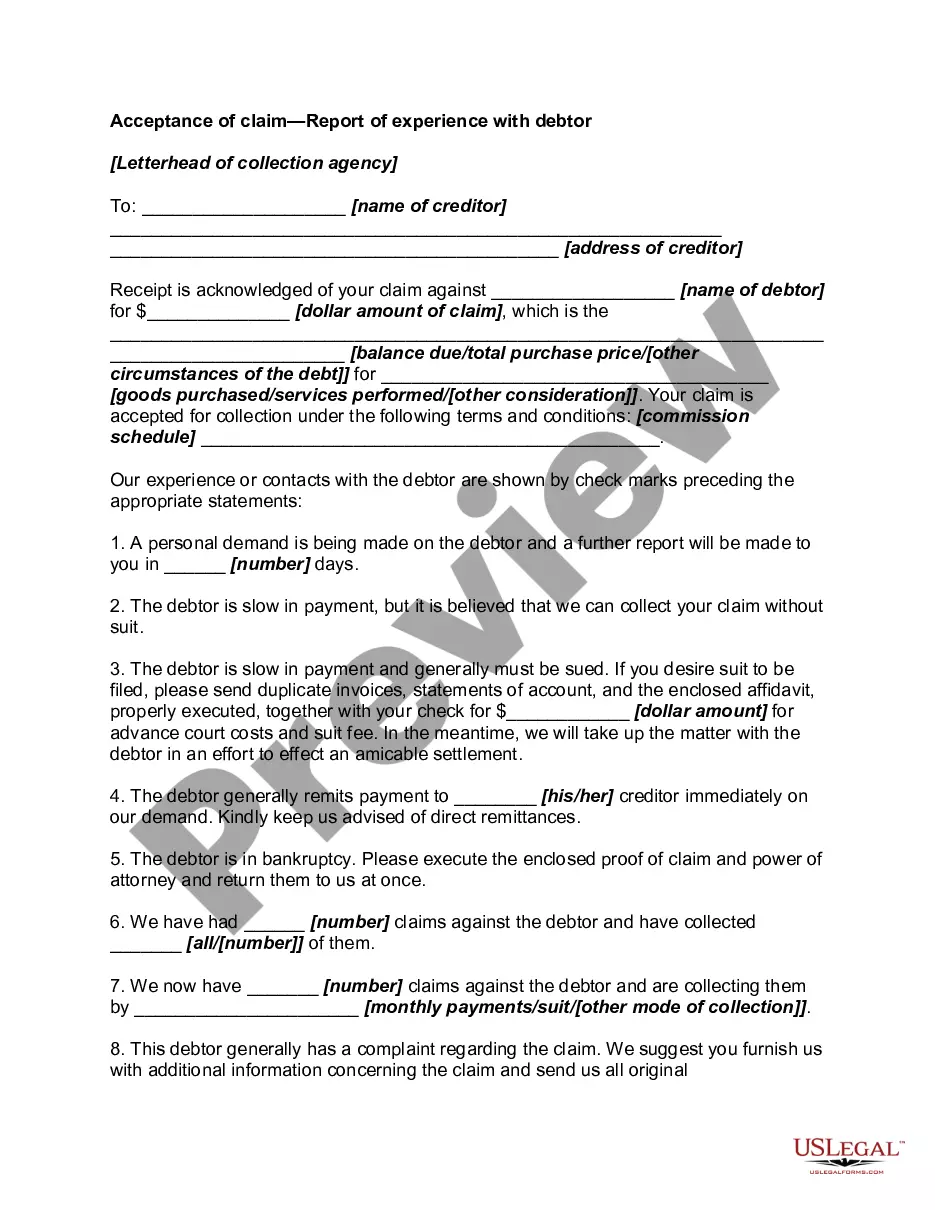

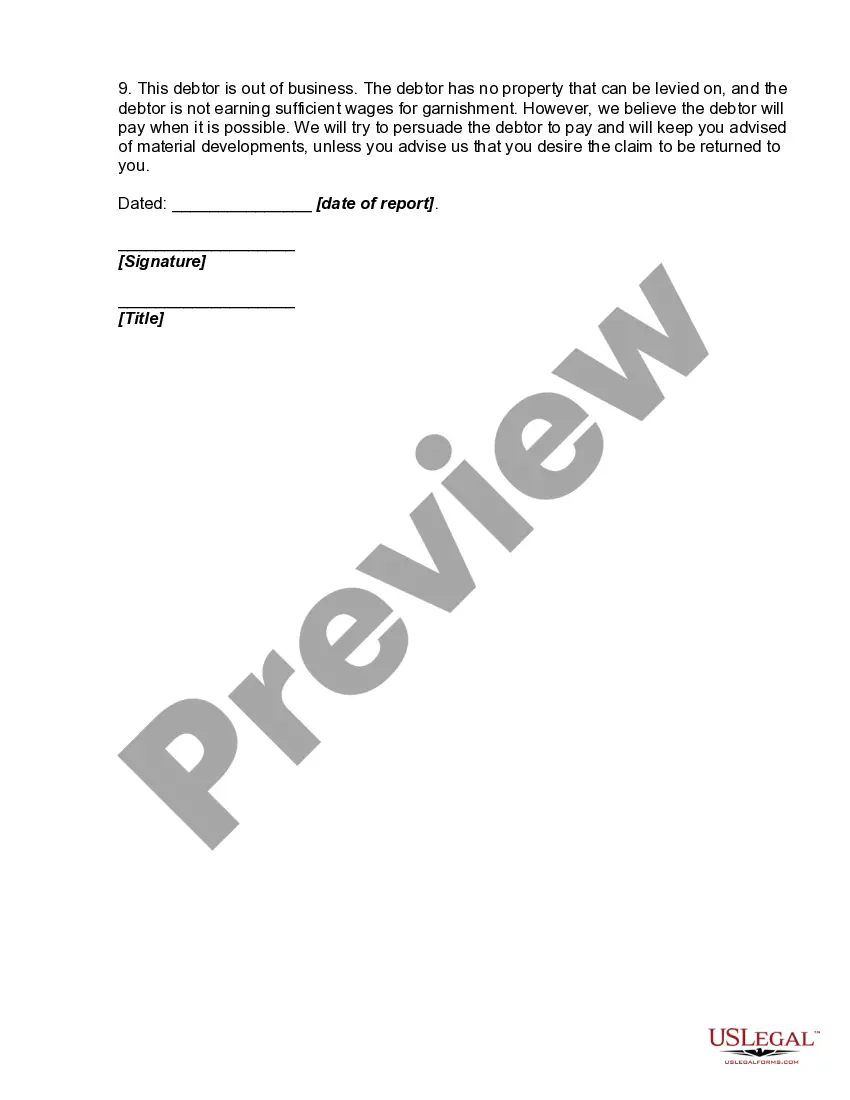

Alameda California Acceptance of Claim by Collection Agency and Report of Experience with Debtor

Description

How to fill out Alameda California Acceptance Of Claim By Collection Agency And Report Of Experience With Debtor?

Laws and regulations in every area vary throughout the country. If you're not a lawyer, it's easy to get lost in a variety of norms when it comes to drafting legal documents. To avoid pricey legal assistance when preparing the Alameda Acceptance of Claim by Collection Agency and Report of Experience with Debtor, you need a verified template valid for your county. That's when using the US Legal Forms platform is so beneficial.

US Legal Forms is a trusted by millions web catalog of more than 85,000 state-specific legal forms. It's a perfect solution for professionals and individuals searching for do-it-yourself templates for various life and business occasions. All the forms can be used many times: once you obtain a sample, it remains available in your profile for further use. Therefore, when you have an account with a valid subscription, you can simply log in and re-download the Alameda Acceptance of Claim by Collection Agency and Report of Experience with Debtor from the My Forms tab.

For new users, it's necessary to make several more steps to get the Alameda Acceptance of Claim by Collection Agency and Report of Experience with Debtor:

- Take a look at the page content to ensure you found the appropriate sample.

- Use the Preview option or read the form description if available.

- Look for another doc if there are inconsistencies with any of your criteria.

- Use the Buy Now button to obtain the template when you find the correct one.

- Opt for one of the subscription plans and log in or sign up for an account.

- Select how you prefer to pay for your subscription (with a credit card or PayPal).

- Select the format you want to save the document in and click Download.

- Fill out and sign the template on paper after printing it or do it all electronically.

That's the simplest and most cost-effective way to get up-to-date templates for any legal scenarios. Locate them all in clicks and keep your paperwork in order with the US Legal Forms!

Form popularity

FAQ

Like the credit bureaus, the collection agency has 30 days to investigate and respond to your dispute. Most disputes dealing with removing inaccurate information get resolved smoothly. Make sure you follow the steps and provide all the necessary documentation to back your claim.

Ask CFPB Who you're talking to (get the person's name) The name of the debt collection company they work for. The company's address and phone number. The name of the original creditor. The amount owed. How you can dispute the debt or ensure that the debt is yours.

You should not ignore a debt collection letter as not responding to them in time (or at all) can lead to the collection agency filing a lawsuit against you. Not only will this result in you being responsible for additional fees, but it can allow them to take legal action to get the funds from you in other ways.

Ask CFPB Who you're talking to (get the person's name) The name of the debt collection company they work for. The company's address and phone number. The name of the original creditor. The amount owed. How you can dispute the debt or ensure that the debt is yours.

Within 30 days of receiving the written notice of debt, send a written dispute to the debt collection agency. You can use this sample dispute letter (PDF) as a model. Once you dispute the debt, the debt collector must stop all debt collection activities until it sends you verification of the debt.

Once you dispute the debt, the debt collector can't call or contact you to collect the debt or the disputed part of the debt until the debt collector has provided verification of the debt in writing to you.

According to federal credit law spelled out in the Fair Credit Reporting Act (FCRA), a credit bureau is required to respond to you and complete their investigation within 30 days. If they do not respond within this time frame, they must remove the negative listing disputed.

Failing to respond to a Debt Validation Letter while continuing to collect on the debt is a direct violation of the FDCPA. You can report a debt collector's failure to respond to your state's attorney general, the Consumer Financial Protection Bureau (CFPB), or the FTC.

Federal law says that after receiving written notice of a debt, consumers have a 30-day window to respond with a debt dispute letter.

Collection accounts remain on your credit report for seven years. If a debt collector can get a 10-year-old debt back on your credit report, they know this may prompt you to pay or settle to have it removed. However, they cannot, by law, provide misleading information to a credit bureau.