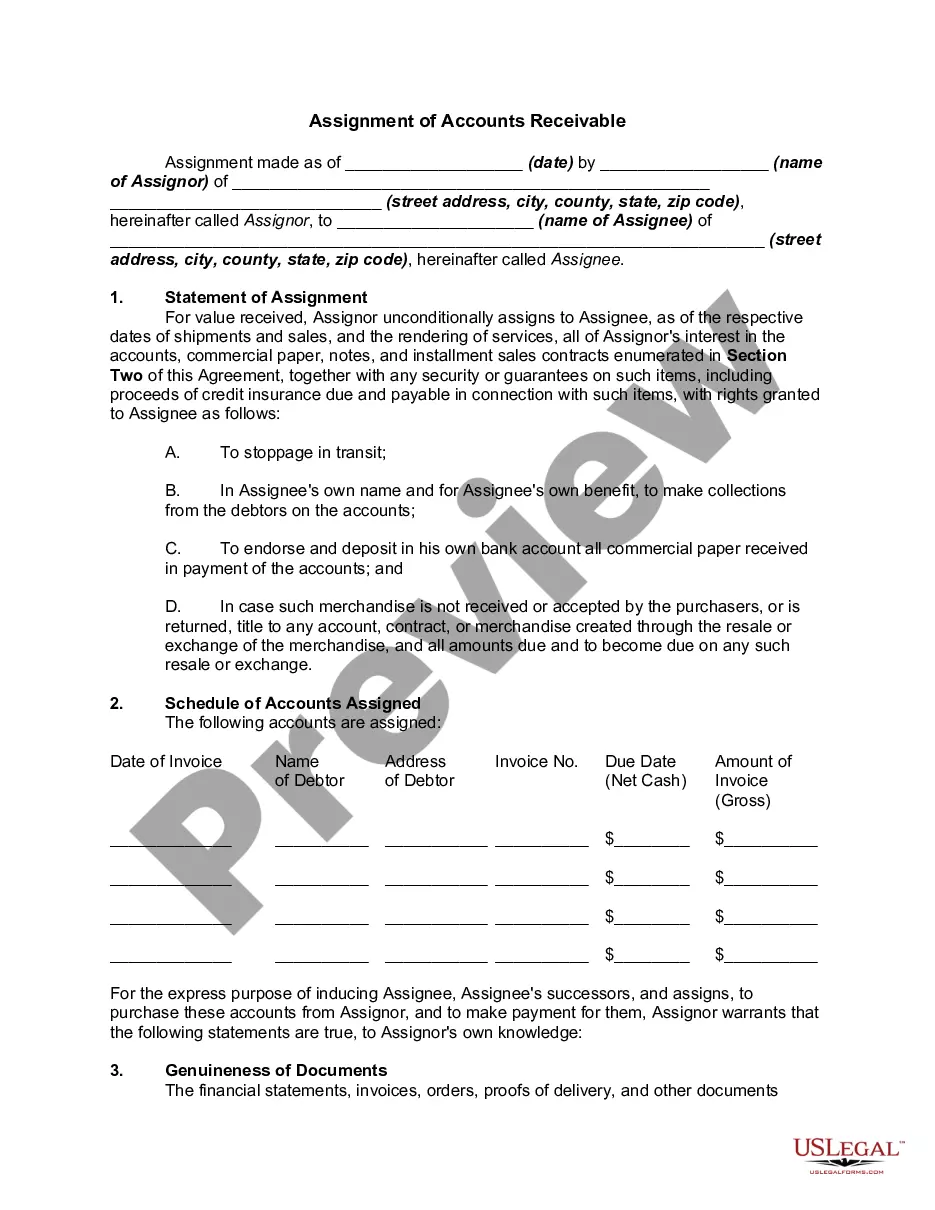

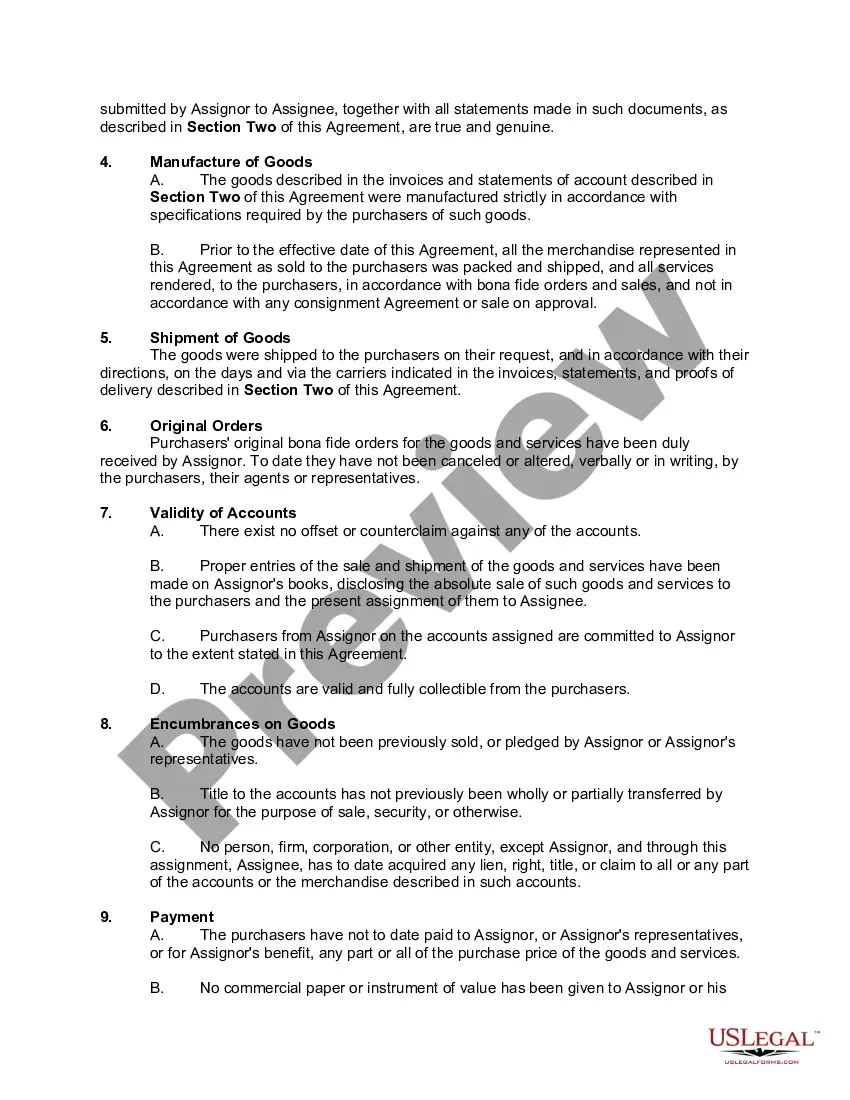

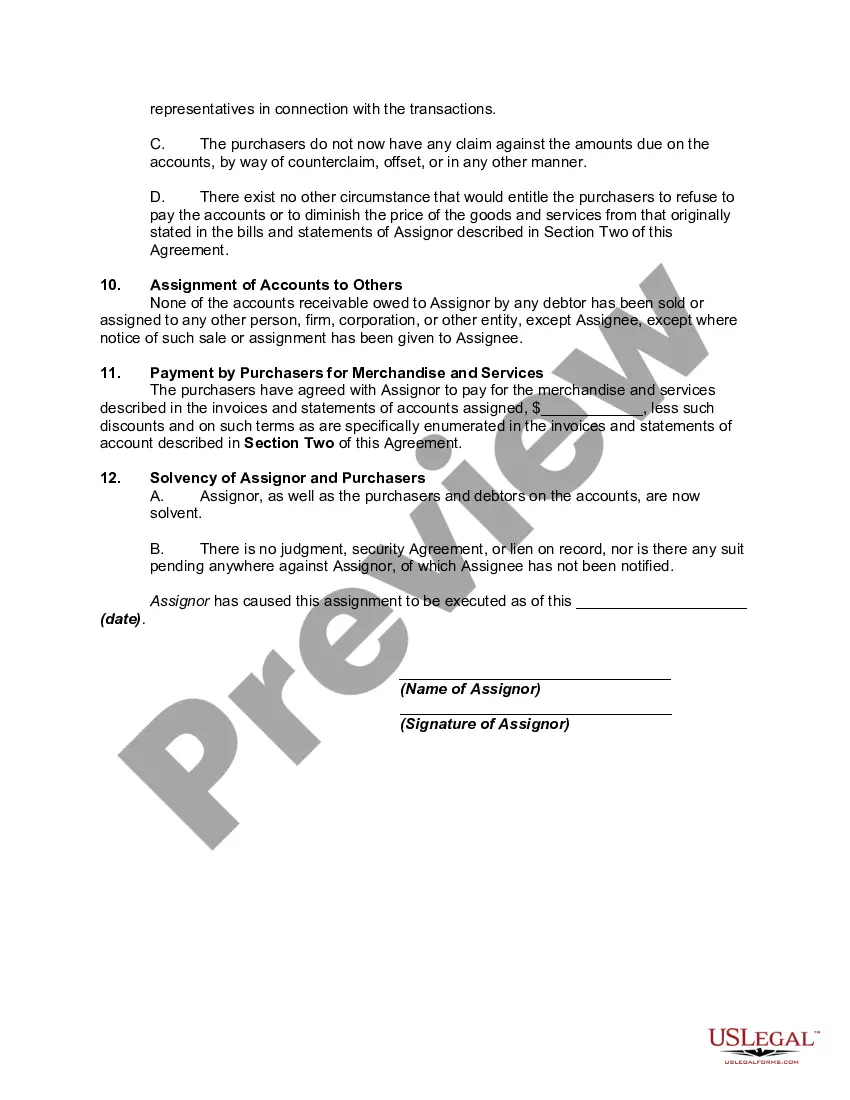

Hennepin Minnesota Assignment of Accounts Receivable is a legal document that allows a business or individual to transfer their unpaid invoices or accounts receivable to another party, known as the assignee. This assignment is commonly used as a financing tool to access immediate funds by selling the right to collect the outstanding balances to the assignee. The primary purpose of Hennepin Minnesota Assignment of Accounts Receivable is to provide a way for businesses to improve their cash flow and maintain financial stability. By assigning their accounts receivable, businesses can convert their unpaid invoices into liquid assets, enabling them to pay operational expenses, invest in growth opportunities, or meet other financial obligations in a timely manner. There are two main types of Hennepin Minnesota Assignment of Accounts Receivable: 1. Recourse Assignment: In this type of assignment, the assignor (the business or individual transferring the receivables) remains liable for any uncollected or disputed amounts. If the assignee is unable to collect the assigned receivables, the assignor must repurchase them and take responsibility for the outstanding balances. 2. Non-Recourse Assignment: With a non-recourse assignment, the assignor assumes no liability for uncollected amounts. If the assigned receivables cannot be collected by the assignee, they bear the loss, and the assignor is not obligated to repurchase the accounts receivable. The Hennepin Minnesota Assignment of Accounts Receivable typically includes various key elements, such as: — Identification of the assignor and assignee: The legal names and contact information of both parties involved in the assignment process. — Description of assigned accounts: A detailed list or description of the accounts receivable being assigned, including invoice numbers, customer names, outstanding balances, and payment terms. — Consideration: The agreed-upon price or value at which the assignor transfers the accounts receivable to the assignee. — Representations and warranties: Statements made by the assignor about the validity, accuracy, and collect ability of the assigned receivables. — Term and termination: The duration of the assignment or any conditions under which it can be terminated by either party. — Governing law and jurisdiction: The specific laws and regulations of Hennepin County, Minnesota, that apply to the assignment, along with the designated courts or arbitration forums for resolving disputes. — Signatures and dates: Both parties' signatures, along with the date of execution, to indicate their consent and agreement to the terms stated in the assignment. Understanding the Hennepin Minnesota Assignment of Accounts Receivable is crucial for businesses seeking to leverage their outstanding invoices to improve their financial position. By effectively utilizing this financial tool, businesses can enhance their liquidity, manage cash flow, and optimize their operational performance.

Hennepin Minnesota Assignment of Accounts Receivable

Description

How to fill out Hennepin Minnesota Assignment Of Accounts Receivable?

Whether you intend to start your business, enter into a deal, apply for your ID update, or resolve family-related legal issues, you need to prepare certain documentation meeting your local laws and regulations. Finding the right papers may take a lot of time and effort unless you use the US Legal Forms library.

The service provides users with more than 85,000 expertly drafted and verified legal templates for any personal or business occasion. All files are grouped by state and area of use, so picking a copy like Hennepin Assignment of Accounts Receivable is quick and simple.

The US Legal Forms library users only need to log in to their account and click the Download button next to the required template. If you are new to the service, it will take you a couple of additional steps to get the Hennepin Assignment of Accounts Receivable. Follow the guide below:

- Make sure the sample meets your personal needs and state law requirements.

- Look through the form description and check the Preview if available on the page.

- Make use of the search tab specifying your state above to locate another template.

- Click Buy Now to get the sample once you find the correct one.

- Select the subscription plan that suits you most to proceed.

- Sign in to your account and pay the service with a credit card or PayPal.

- Download the Hennepin Assignment of Accounts Receivable in the file format you require.

- Print the copy or complete it and sign it electronically via an online editor to save time.

Forms provided by our library are reusable. Having an active subscription, you can access all of your previously purchased paperwork at any time in the My Forms tab of your profile. Stop wasting time on a endless search for up-to-date formal documentation. Sign up for the US Legal Forms platform and keep your paperwork in order with the most extensive online form library!