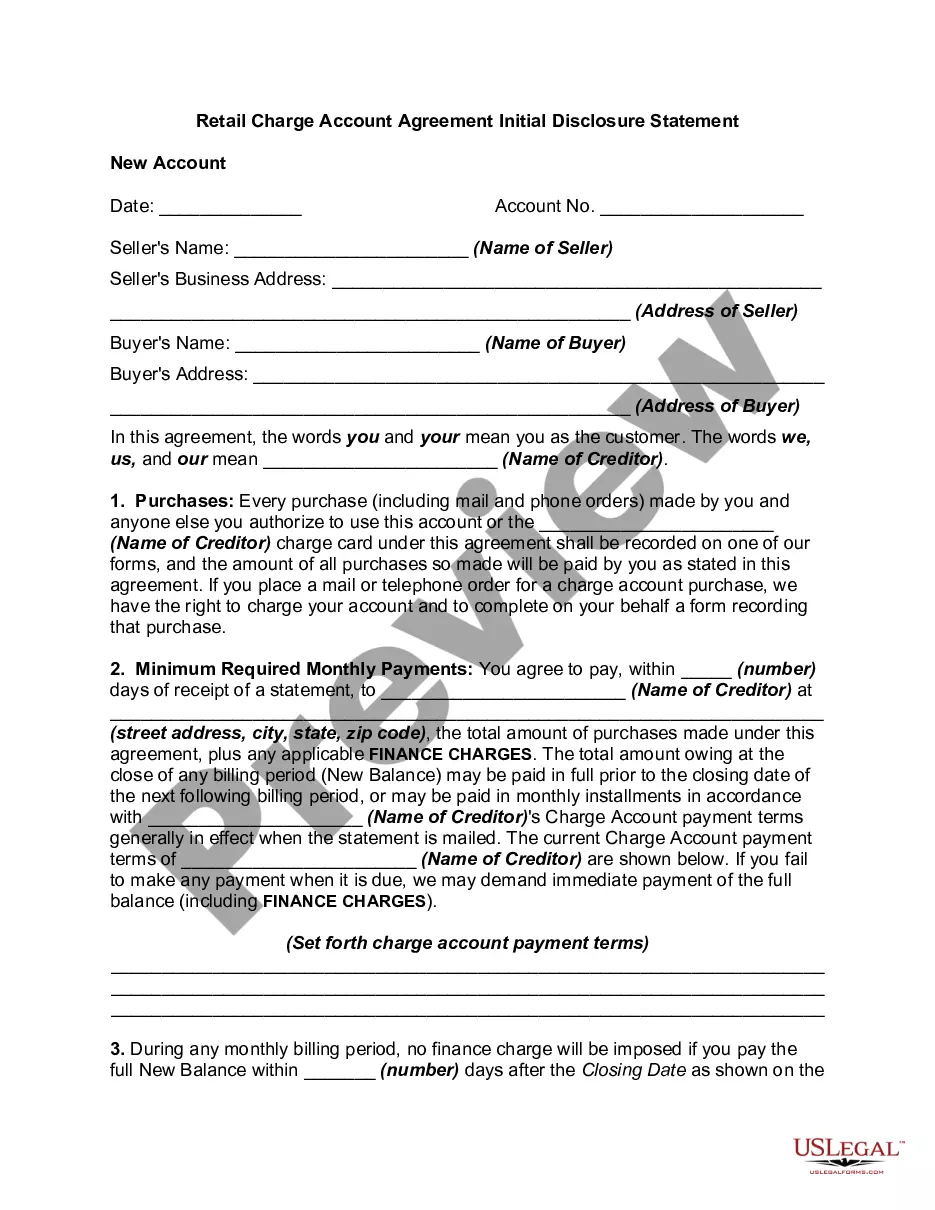

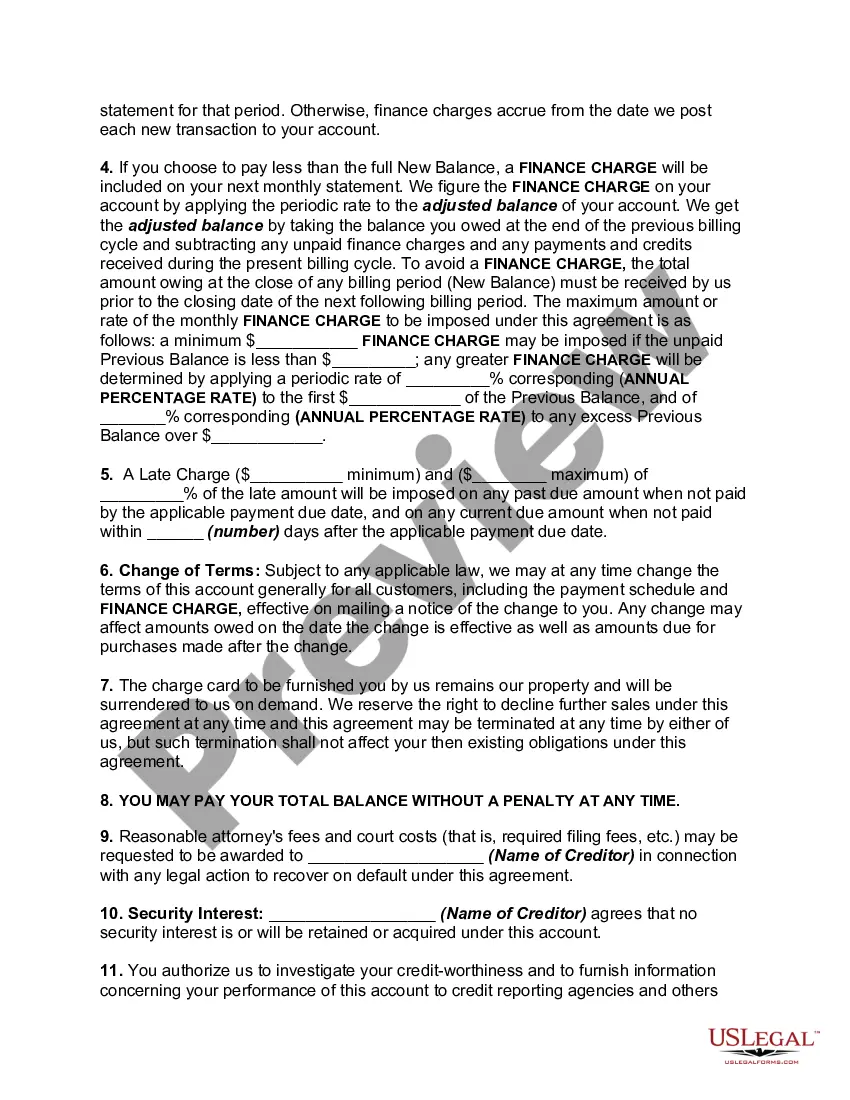

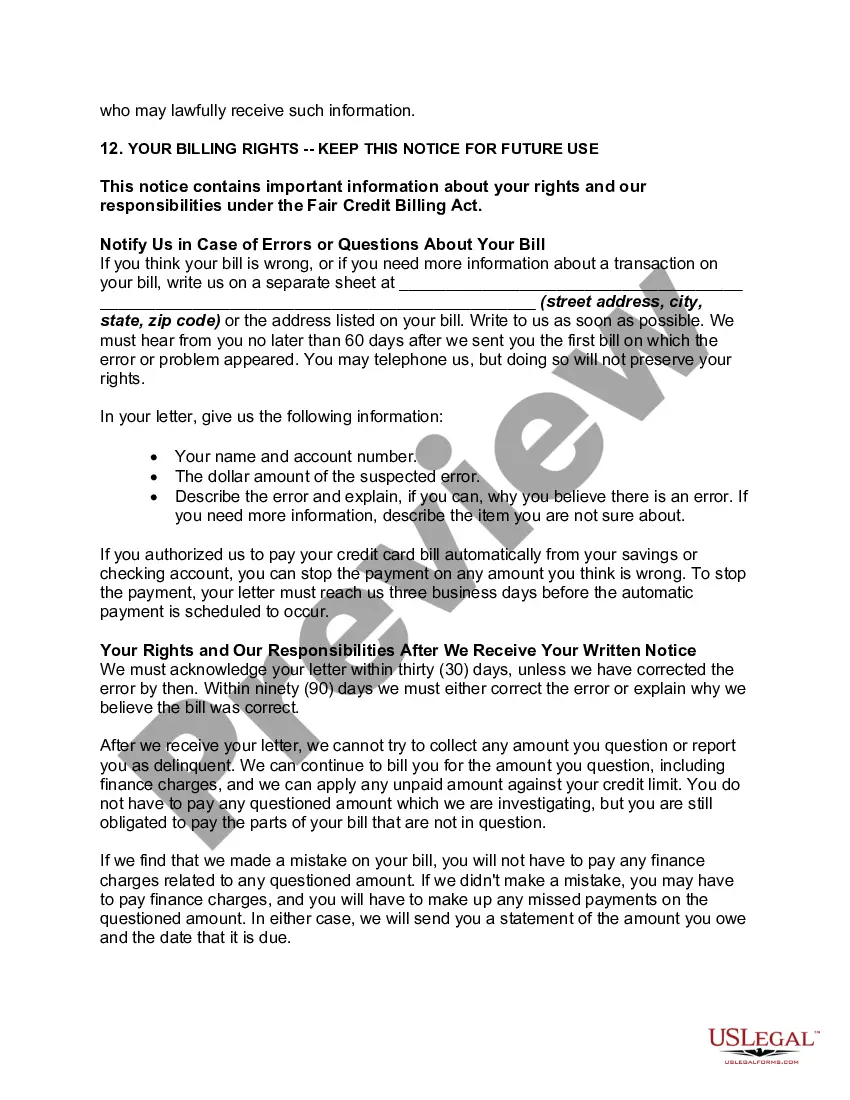

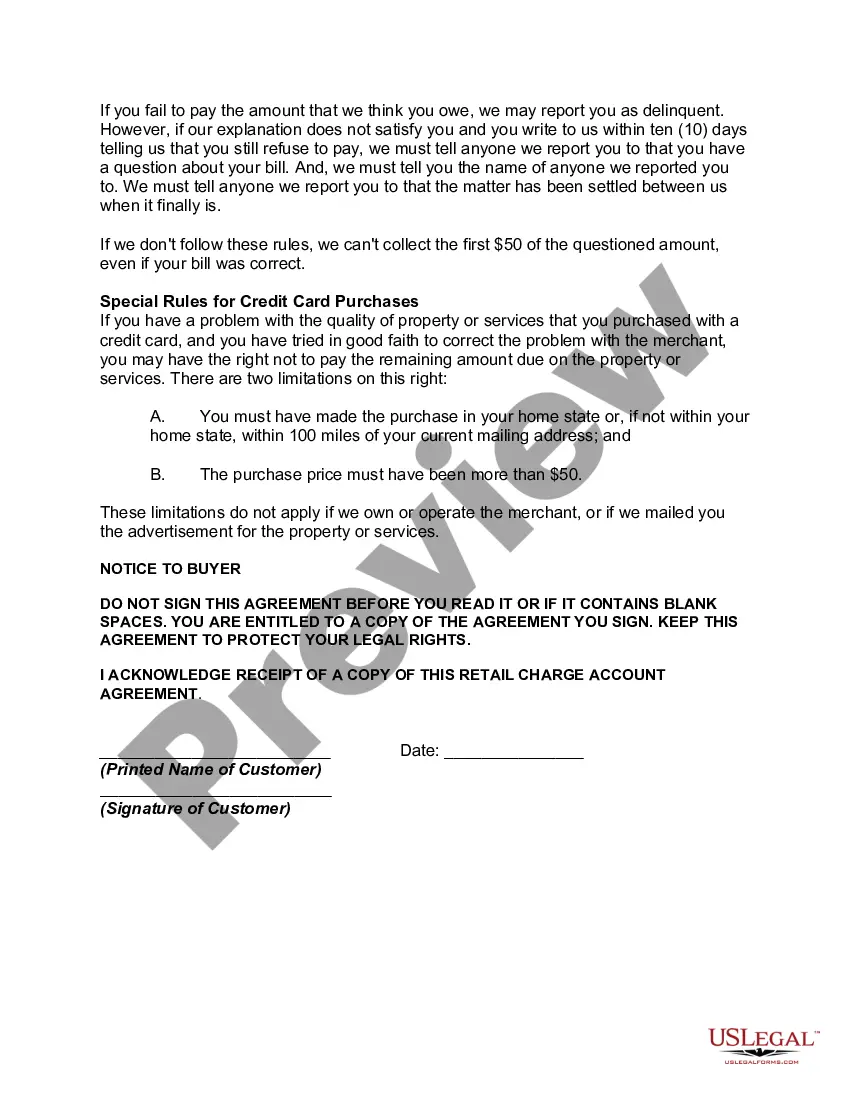

The Chicago, Illinois Retail Charge Account Agreement Initial Disclosure Statement is a legal document that outlines important terms and conditions associated with retail charge accounts in the city of Chicago, Illinois. It serves to inform both the retail account holders and the retailers about their rights and responsibilities when using this financial service. This agreement entails several key aspects to ensure transparency, compliance, and protection for all parties involved. It typically includes information about the parties to the agreement, account opening procedures, account maintenance fees, interest rates, late payment fees, grace periods, and dispute resolution processes. In Chicago, there may be different types of Retail Charge Account Agreement Initial Disclosure Statements, tailor-made to suit specific retail industries or institutions. For example, there could be separate agreements for general retailers, department stores, specialty stores, or online retailers. Each agreement may have specific provisions and disclosures that are relevant to the distinct nature of the particular retail business. Retail charge accounts allow consumers to make purchases on credit, maintaining an ongoing balance that can be paid off over time. The agreement outlines the terms under which this credit is extended to the customer. Key elements often covered in these disclosures include the interest rate charged on the unpaid balance, the minimum payment requirement, and any additional fees that may be incurred. Generally, the disclosure statement provides detailed instructions for customers to understand how to use and manage their charge accounts properly. This may include outlining when payments are due, how interest is calculated, and any penalties or fees associated with delinquency. Additionally, it may also inform customers of their rights regarding disputes, such as the process for reporting errors on their billing statements or unauthorized charges. It's important for both retailers and customers to thoroughly review the Chicago, Illinois Retail Charge Account Agreement Initial Disclosure Statement. Retailers need to ensure compliance with applicable laws and regulations, such as the Truth in Lending Act, while customers need to understand their financial obligations to avoid any potential misunderstandings or adverse financial consequences. In summary, the Chicago, Illinois Retail Charge Account Agreement Initial Disclosure Statement is a comprehensive document that outlines the terms and conditions associated with retail charge accounts in the city. It provides important information about account opening procedures, fees, interest rates, dispute resolution, and other essential details. By familiarizing themselves with the agreement, both retailers and customers can make informed decisions regarding the use and management of retail charge accounts.

Chicago Illinois Retail Charge Account Agreement Initial Disclosure Statement

Description

How to fill out Chicago Illinois Retail Charge Account Agreement Initial Disclosure Statement?

A document routine always accompanies any legal activity you make. Staring a business, applying or accepting a job offer, transferring ownership, and lots of other life situations require you prepare official documentation that varies throughout the country. That's why having it all accumulated in one place is so beneficial.

US Legal Forms is the largest online library of up-to-date federal and state-specific legal templates. On this platform, you can easily find and download a document for any personal or business objective utilized in your county, including the Chicago Retail Charge Account Agreement Initial Disclosure Statement.

Locating forms on the platform is extremely simple. If you already have a subscription to our library, log in to your account, find the sample through the search bar, and click Download to save it on your device. After that, the Chicago Retail Charge Account Agreement Initial Disclosure Statement will be accessible for further use in the My Forms tab of your profile.

If you are dealing with US Legal Forms for the first time, follow this simple guideline to obtain the Chicago Retail Charge Account Agreement Initial Disclosure Statement:

- Make sure you have opened the correct page with your localised form.

- Use the Preview mode (if available) and scroll through the sample.

- Read the description (if any) to ensure the template meets your needs.

- Look for another document via the search option if the sample doesn't fit you.

- Click Buy Now once you locate the necessary template.

- Decide on the suitable subscription plan, then sign in or create an account.

- Select the preferred payment method (with credit card or PayPal) to continue.

- Opt for file format and download the Chicago Retail Charge Account Agreement Initial Disclosure Statement on your device.

- Use it as needed: print it or fill it out electronically, sign it, and send where requested.

This is the simplest and most reliable way to obtain legal paperwork. All the samples available in our library are professionally drafted and checked for correspondence to local laws and regulations. Prepare your paperwork and run your legal affairs effectively with the US Legal Forms!