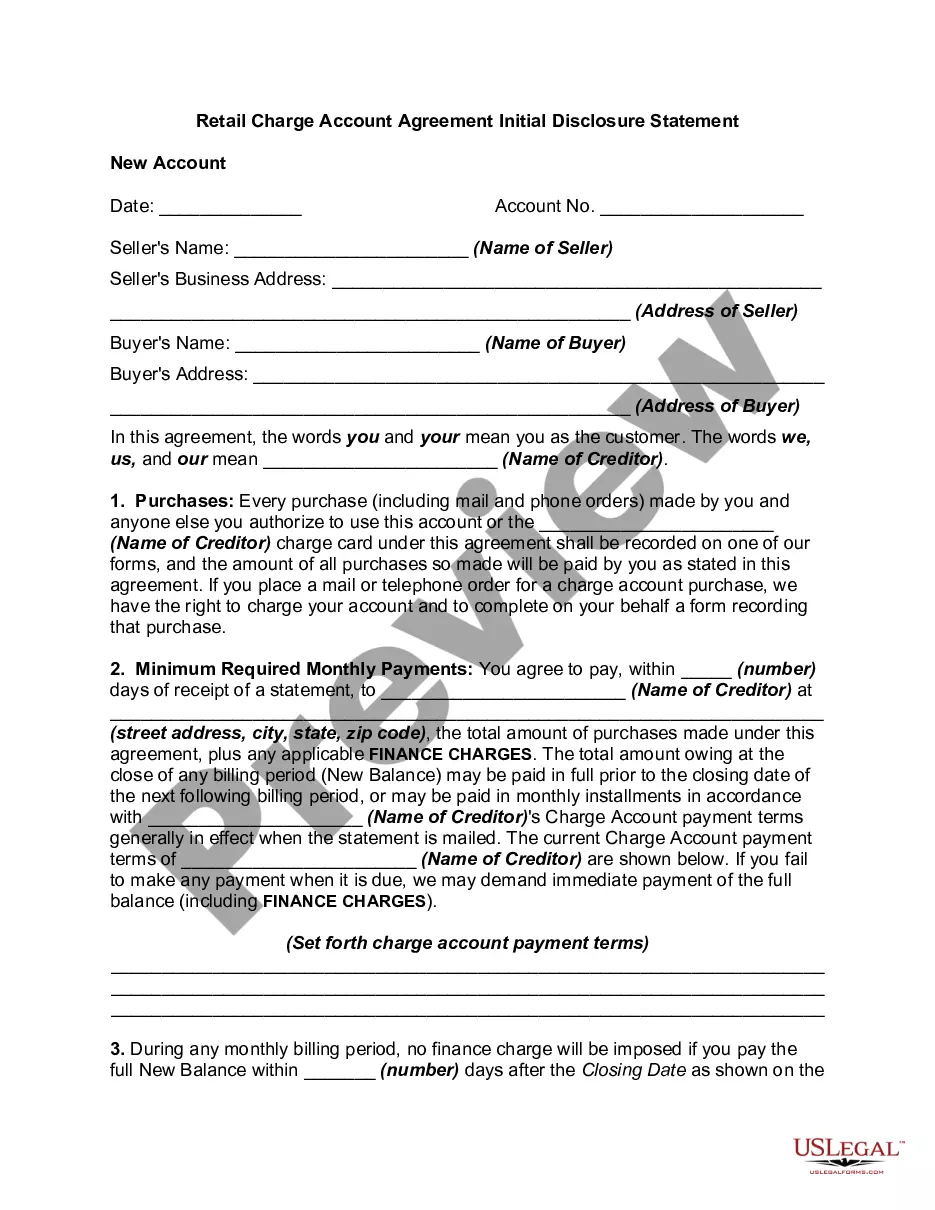

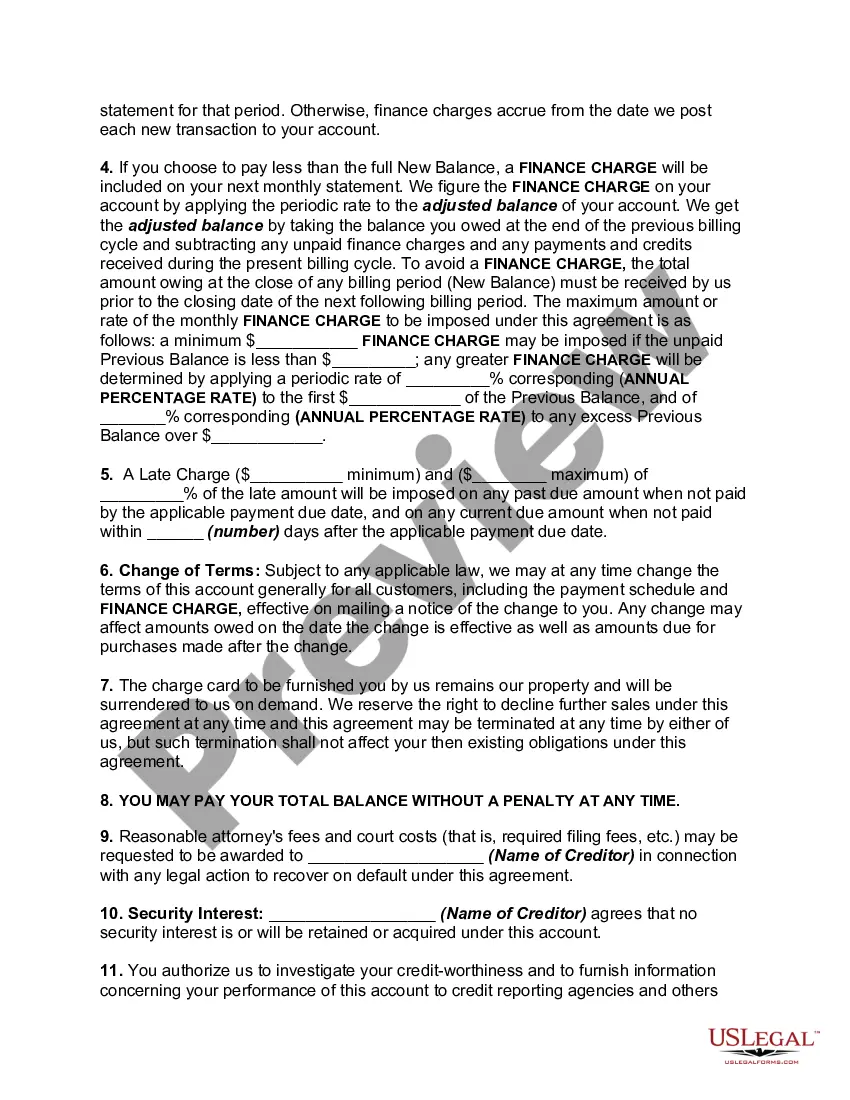

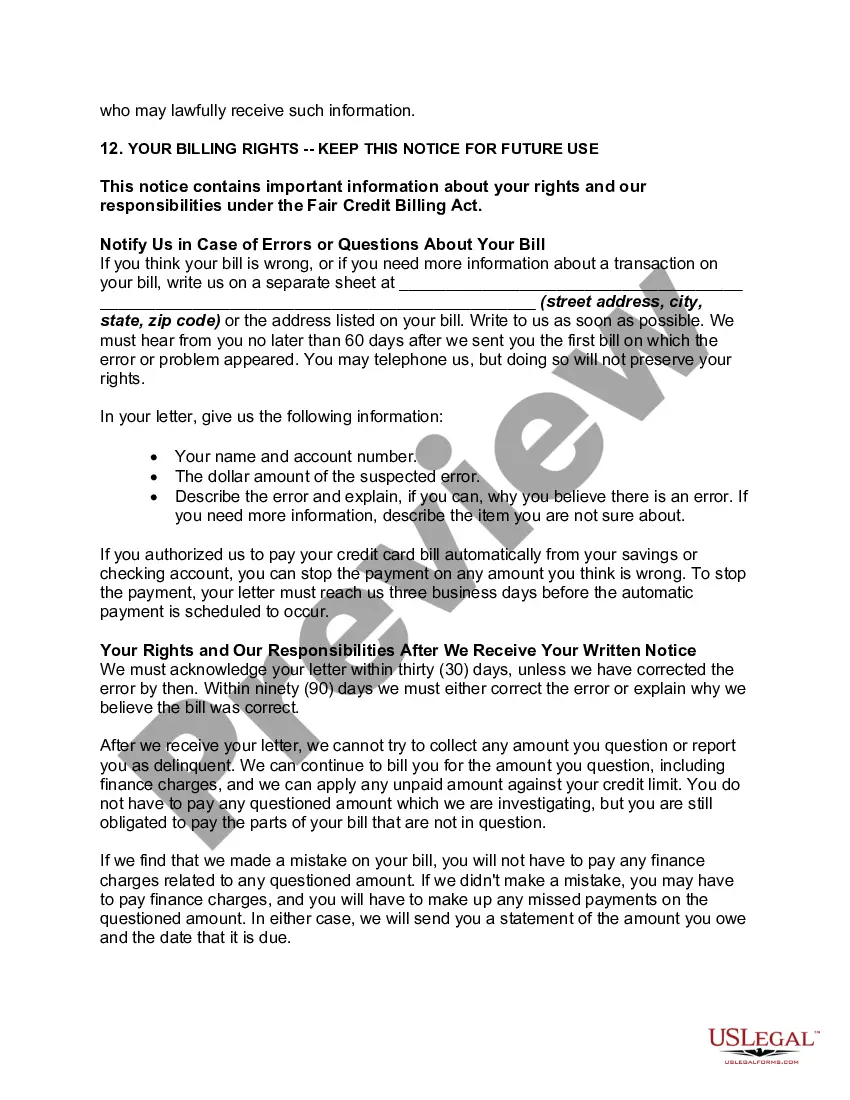

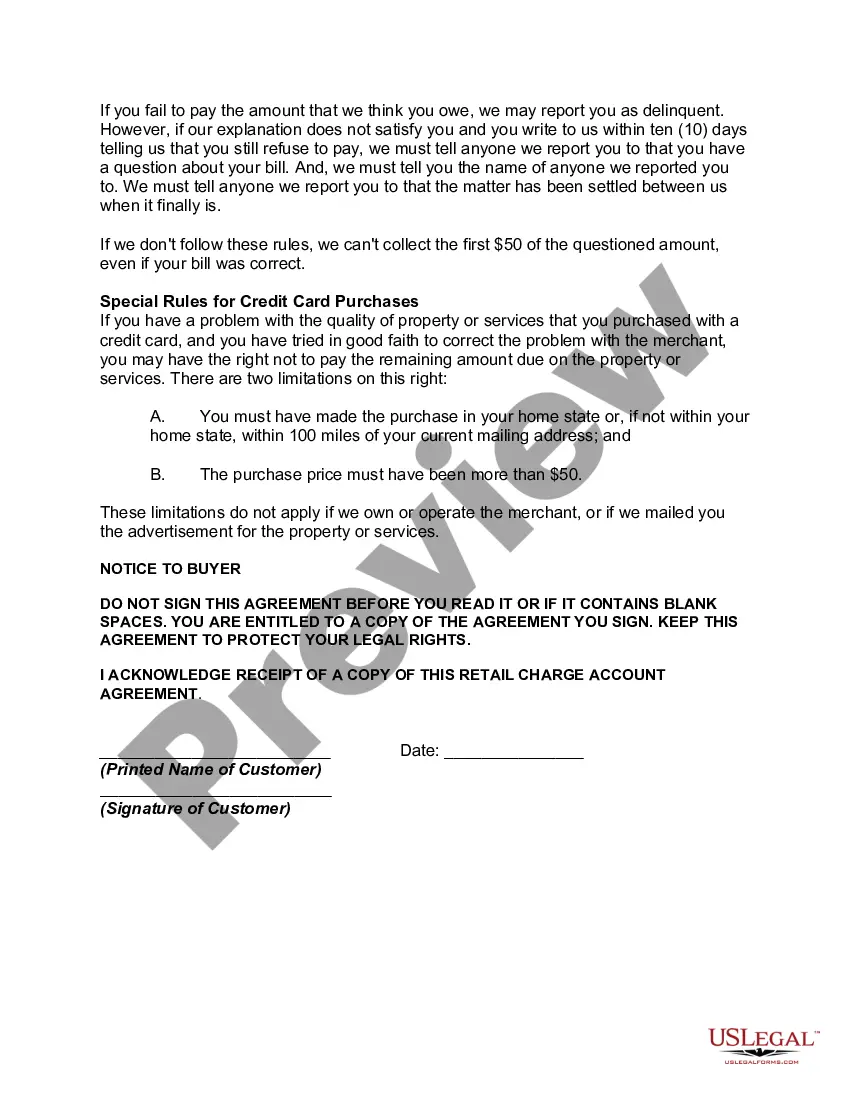

The Collin Texas Retail Charge Account Agreement Initial Disclosure Statement is a document designed to provide detailed information about the terms and conditions associated with a retail charge account in Collin, Texas. This agreement serves as a legally binding contract between the retailer and the customer, outlining the rights and responsibilities of both parties. The Collin Texas Retail Charge Account Agreement Initial Disclosure Statement contains essential information about the account, including the interest rates, fees, and payment terms. It highlights the key features of the charge account, enabling customers to make informed decisions about their purchases and credit obligations. This document typically includes the following: 1. Account Terms and Conditions: This section outlines the general terms and conditions of the retail charge account, such as the minimum age requirement, eligibility criteria, and residency restrictions. 2. Interest Rates: Details about the applicable interest rates for different transaction types, such as purchases, balance transfers, and cash advances, are provided in this section. It specifies whether the interest rates are fixed or variable and the circumstances under which they may change. 3. Fees and Charges: The disclosure statement describes the fees associated with maintaining the retail charge account. Examples may include annual fees, late payment fees, over-limit fees, and transaction fees. The statement explains the circumstances under which these charges are applicable. 4. Payment Terms: This section outlines the payment terms, including the minimum payment due, the due date, and the consequences of late or missed payments. It also provides information on the grace period (if any) before interest is charged on purchases. 5. Billing and Statements: The disclosure statement specifies how billing statements will be delivered, typically indicating whether they will be sent via mail or available online through electronic statements. It also highlights the customer's responsibility to review statements promptly and report any errors or discrepancies. 6. Credit Limit: Details about the credit limit, including how it is determined and the consequences of exceeding it, are discussed in this section. It may also outline the process for requesting a credit limit increase. Different types of Collin Texas Retail Charge Account Agreement Initial Disclosure Statements may differ based on the retailer or financial institution providing the charge account. However, their purpose remains consistent: to inform customers about the terms and conditions governing their retail charge account.

Collin Texas Retail Charge Account Agreement Initial Disclosure Statement

Description

How to fill out Collin Texas Retail Charge Account Agreement Initial Disclosure Statement?

Creating documents, like Collin Retail Charge Account Agreement Initial Disclosure Statement, to manage your legal affairs is a tough and time-consumming process. A lot of circumstances require an attorney’s involvement, which also makes this task not really affordable. Nevertheless, you can acquire your legal affairs into your own hands and take care of them yourself. US Legal Forms is here to the rescue. Our website comes with more than 85,000 legal documents crafted for different scenarios and life situations. We make sure each document is in adherence with the regulations of each state, so you don’t have to be concerned about potential legal problems associated with compliance.

If you're already aware of our services and have a subscription with US, you know how easy it is to get the Collin Retail Charge Account Agreement Initial Disclosure Statement form. Go ahead and log in to your account, download the form, and customize it to your needs. Have you lost your document? No worries. You can find it in the My Forms folder in your account - on desktop or mobile.

The onboarding process of new users is fairly simple! Here’s what you need to do before getting Collin Retail Charge Account Agreement Initial Disclosure Statement:

- Ensure that your template is specific to your state/county since the regulations for writing legal documents may differ from one state another.

- Find out more about the form by previewing it or going through a brief description. If the Collin Retail Charge Account Agreement Initial Disclosure Statement isn’t something you were hoping to find, then take advantage of the search bar in the header to find another one.

- Log in or create an account to start using our website and get the document.

- Everything looks great on your side? Hit the Buy now button and select the subscription plan.

- Pick the payment gateway and enter your payment details.

- Your template is ready to go. You can try and download it.

It’s easy to locate and buy the appropriate template with US Legal Forms. Thousands of organizations and individuals are already taking advantage of our extensive collection. Sign up for it now if you want to check what other advantages you can get with US Legal Forms!

Form popularity

FAQ

As part of the required disclosures under Texas Rules of Civil Procedure 194.2, you need to give the other party or parties the correct names and addresses of parties to the lawsuityour name and contact information, including your mailing address and phone number, and contact information for anyone else involved.

Initial disclosures are the preliminary disclosures that must be acknowledged and signed in order to move forward with your loan application. These disclosures outline the initial terms of the mortgage application and also include federal and state required mortgage disclosures.

Unless the court in which the case is pending has local filing rules approved by the Supreme Court that require the filing of a certificate of written discovery, no such filing is required.

Initial disclosures now required under Rule 194 Under amended Rule 194, disclosures are due within 30 days after the first answer is filed. Further, a party cannot serve discovery until after the initial disclosures are due, unless otherwise agreed to by the parties or ordered by the court.

Initial disclosures now required under Rule 194 Further, a party cannot serve discovery until after the initial disclosures are due, unless otherwise agreed to by the parties or ordered by the court.

Failing To Respond To Discovery Can Lead To A Dismissal Of Your Case With Prejudice. In the practice of law, the discovery phase can be your best friend or your worst nightmare. Interrogatories, requests for documents, and depositions can make or break your case.

Texas court rules require every party in a lawsuit to send certain information about their claims or defenses to the other parties at the beginning of the case. These are called initial disclosures.

Under Level 1, the discovery period continues for 180 days from the date the initial disclosures are due. Under Level 2, the discovery period continues until the earlier of 30 days before the date set for trial or nine months after the initial disclosures are due.

3 The primary objective of the initial disclosure obligation is to accelerate the exchange of basic information about the case and to eliminate the paper work involved in requesting such information.

200bIn a unique move, that mimics the rules of Federal Procedure, The Texas Supreme Court has made some of the biggest discovery changes to occur in Texas State trial courts in the past two decades.