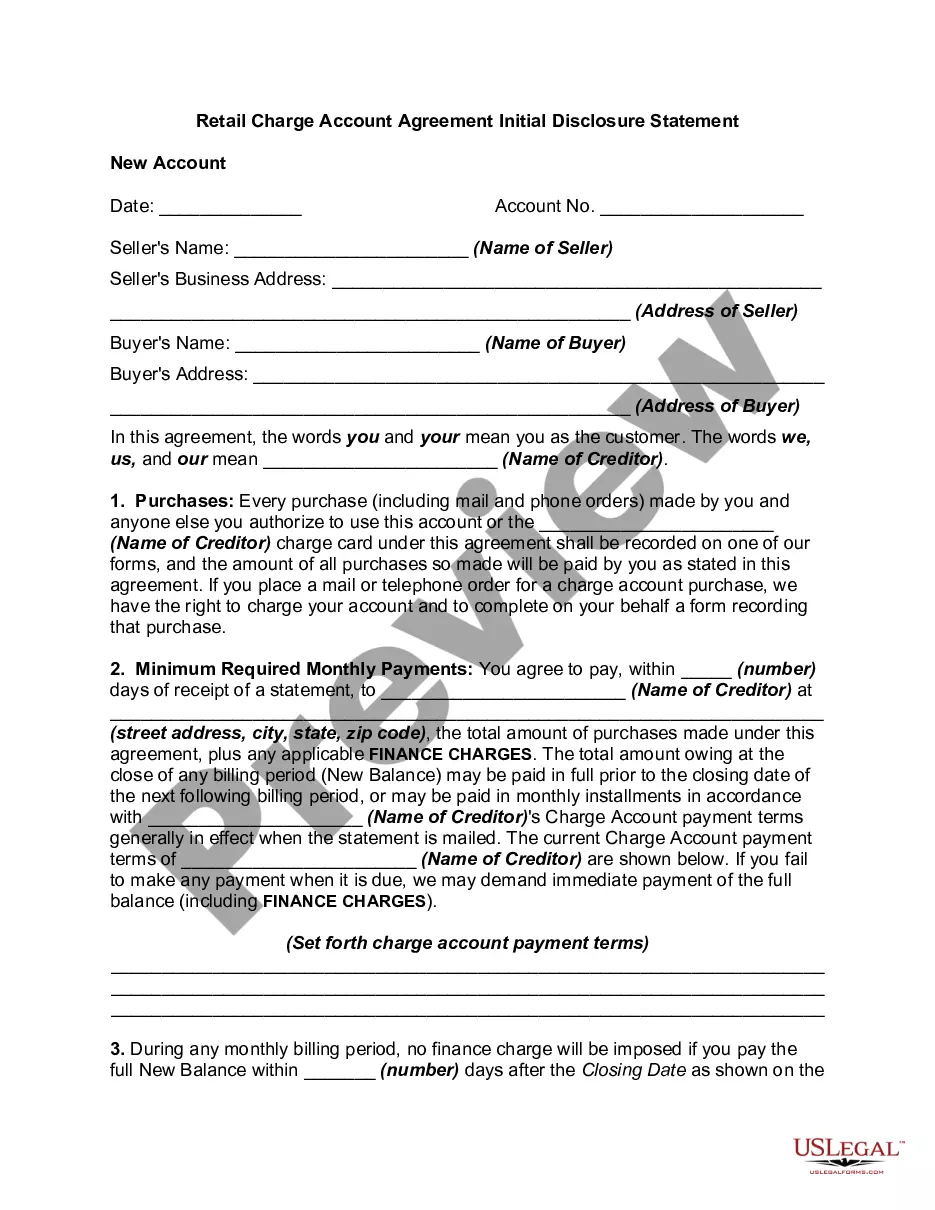

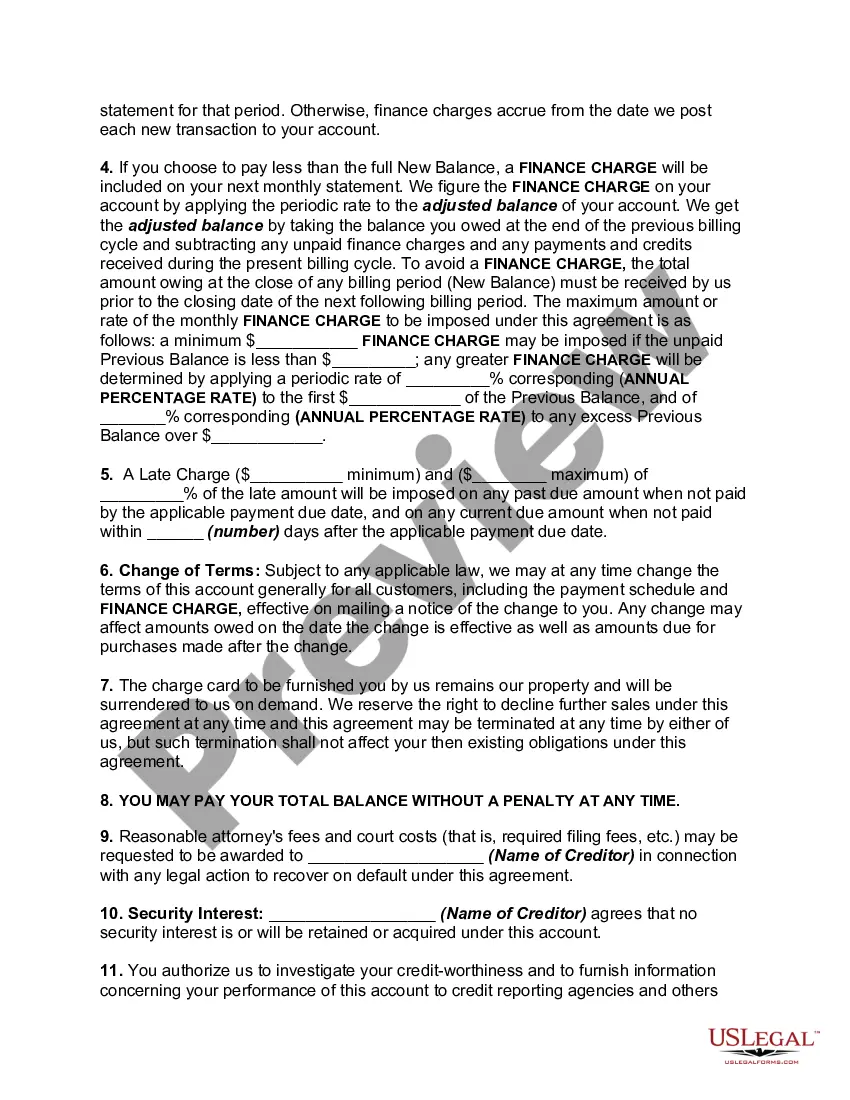

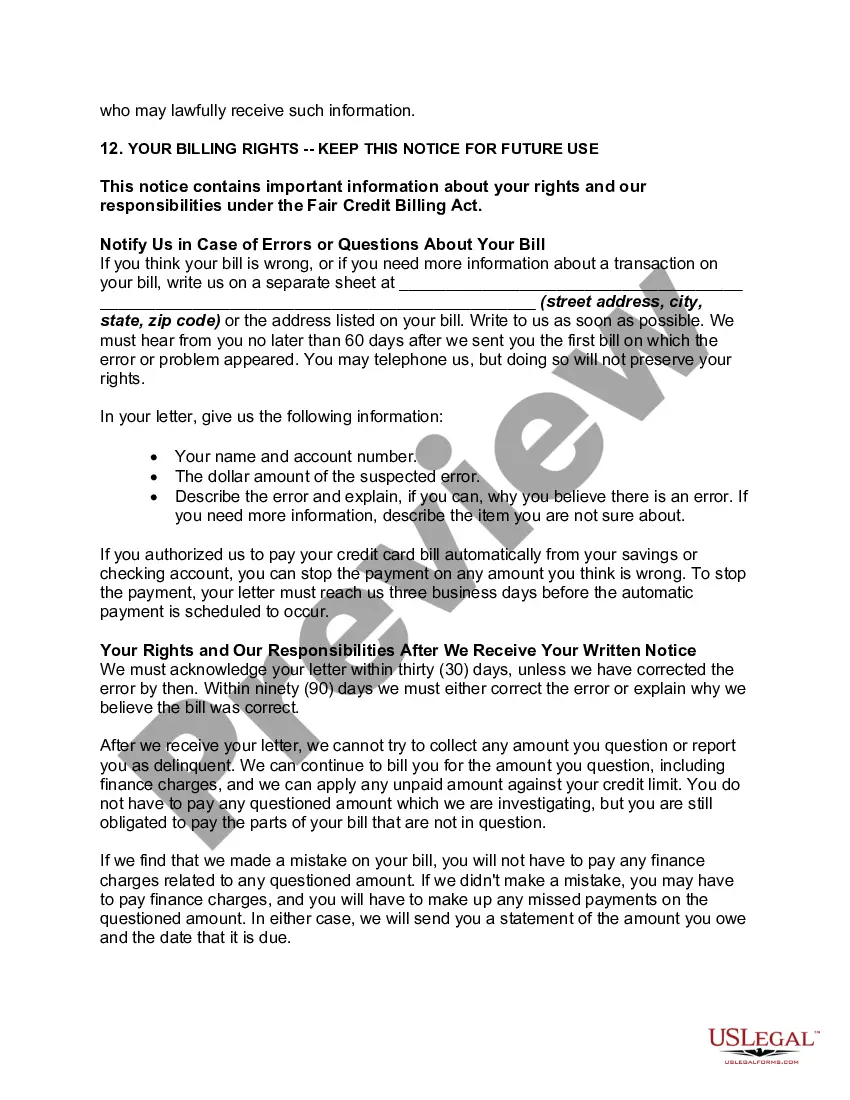

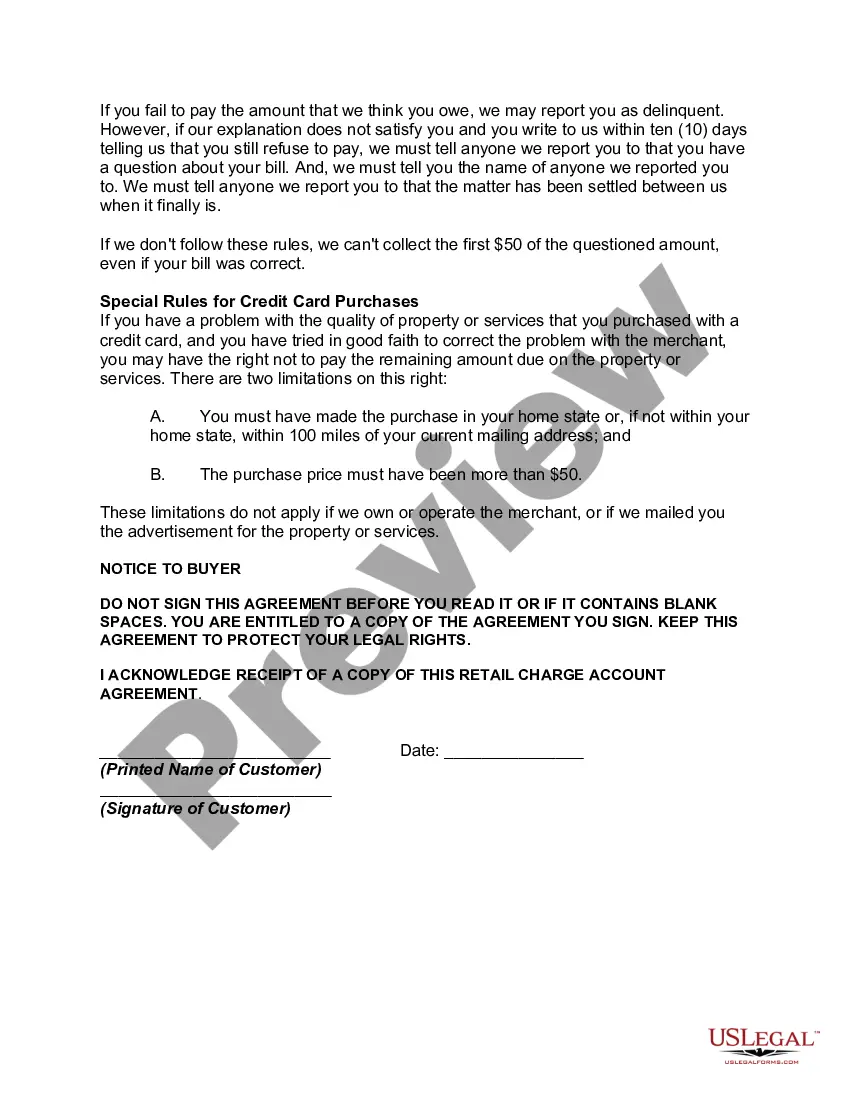

The Cook Illinois Retail Charge Account Agreement Initial Disclosure Statement is an important document that outlines the terms and conditions associated with opening and using a retail charge account provided by Cook Illinois. This agreement serves as a formal contract between the cardholder and Cook Illinois, governing the usage of the retail charge account for making purchases. The initial disclosure statement provides detailed information about the account, ensuring transparency for the cardholder. It covers various aspects such as interest rates, fees, payment terms, and billing cycles. By familiarizing themselves with this agreement, customers can make informed decisions regarding their financial obligations and privileges associated with Cook Illinois retail charge accounts. Key terms and provisions described in the Cook Illinois Retail Charge Account Agreement Initial Disclosure Statement may include the following: 1. Retail charge account: The customer is issued a retail charge account by Cook Illinois that can be used for purchasing goods and services at approved merchants. It acts as a line of credit specifically for retail purchases. 2. Terms and Conditions: This section outlines the terms of the agreement, indicating the rights and responsibilities of the cardholder and Cook Illinois. It includes provisions related to payments, interest rates, fees, dispute resolutions, and account closure. 3. Interest rates: The statement specifies the Annual Percentage Rate (APR) applicable to the retail charge account. It may vary depending on the customer's creditworthiness and market conditions. This information helps the cardholder understand the cost of borrowing and interest charged on outstanding balances. 4. Fees and charges: Cook Illinois may impose various fees related to late payments, returned payments, cash advances, and annual account maintenance. The disclosure statement provides a comprehensive list of all applicable fees, ensuring transparency to the cardholder regarding potential expenses. 5. Grace period: The agreement determines the length of time, if any, during which the cardholder can pay the outstanding balance without incurring interest charges. This grace period allows customers to avoid interest on purchases if the entire statement balance is paid in full by the due date. 6. Billing and payment: The disclosure statement details the billing cycle, due dates, and accepted payment methods. It also highlights any penalties for late or missed payments, emphasizing the importance of timely payments for maintaining a good credit score. It is essential to note that there may be different types or versions of Cook Illinois Retail Charge Account Agreement Initial Disclosure Statements depending on factors such as the cardholder's creditworthiness, the specific Cook Illinois product, or state regulations. These differences may include varying APR's, fees, or additional provisions tailored to meet different customer needs or legal requirements. It is crucial for customers to carefully review and understand the specific terms outlined in their agreement.

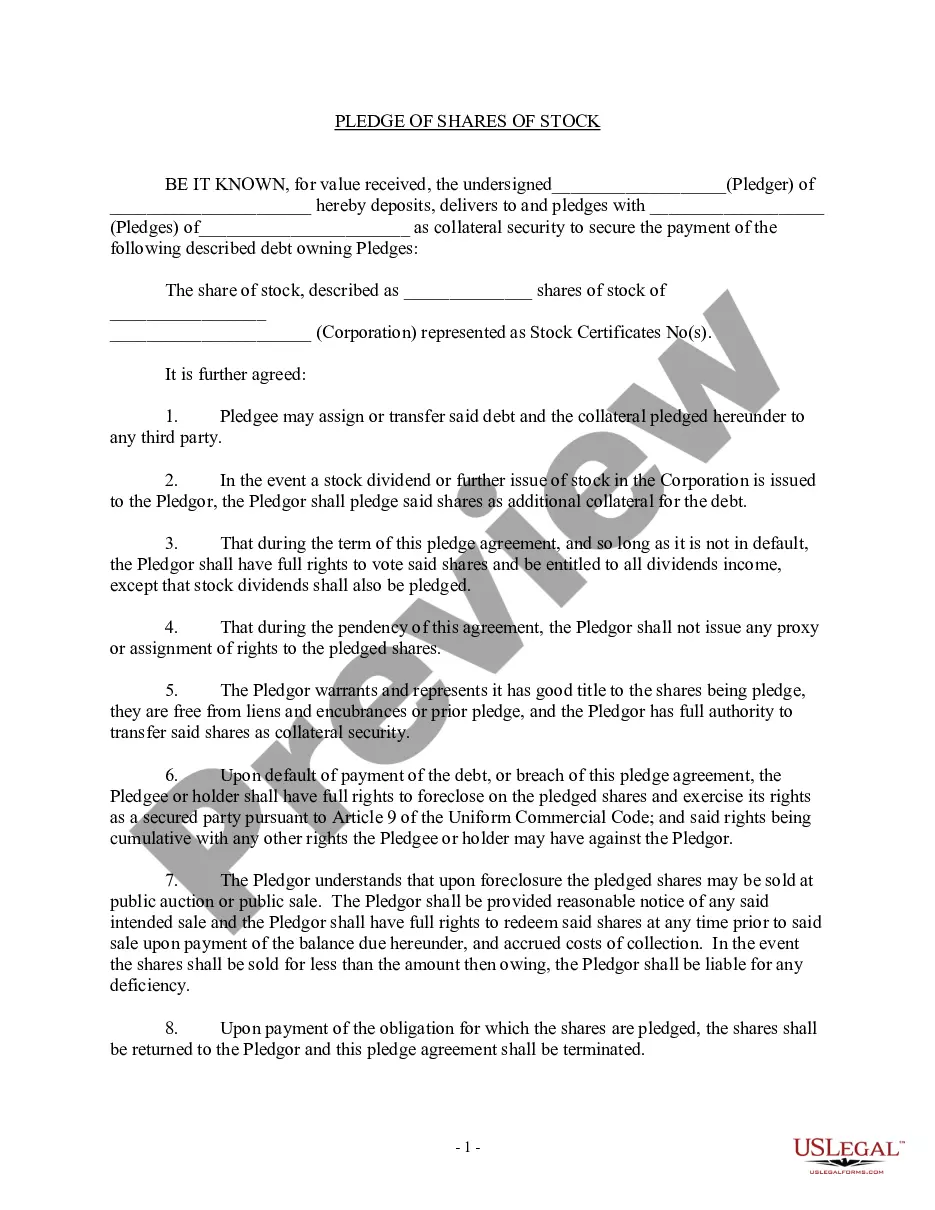

Cook Illinois Retail Charge Account Agreement Initial Disclosure Statement

Description

How to fill out Cook Illinois Retail Charge Account Agreement Initial Disclosure Statement?

Whether you intend to start your business, enter into a deal, apply for your ID update, or resolve family-related legal issues, you need to prepare certain documentation meeting your local laws and regulations. Finding the right papers may take a lot of time and effort unless you use the US Legal Forms library.

The service provides users with more than 85,000 expertly drafted and verified legal documents for any personal or business occurrence. All files are collected by state and area of use, so picking a copy like Cook Retail Charge Account Agreement Initial Disclosure Statement is quick and easy.

The US Legal Forms library users only need to log in to their account and click the Download key next to the required form. If you are new to the service, it will take you a couple of more steps to obtain the Cook Retail Charge Account Agreement Initial Disclosure Statement. Adhere to the guidelines below:

- Make sure the sample meets your individual needs and state law regulations.

- Read the form description and check the Preview if available on the page.

- Use the search tab providing your state above to find another template.

- Click Buy Now to obtain the file when you find the right one.

- Choose the subscription plan that suits you most to continue.

- Sign in to your account and pay the service with a credit card or PayPal.

- Download the Cook Retail Charge Account Agreement Initial Disclosure Statement in the file format you prefer.

- Print the copy or complete it and sign it electronically via an online editor to save time.

Forms provided by our library are multi-usable. Having an active subscription, you are able to access all of your previously purchased paperwork at any time in the My Forms tab of your profile. Stop wasting time on a constant search for up-to-date formal documentation. Join the US Legal Forms platform and keep your paperwork in order with the most extensive online form collection!

Form popularity

FAQ

Loan costs must be disclosed under Truth in Lending and Regulation Z. Title charges are closing costs disclosed under RESPA and Regulation X.

When you make an offer on a home, one of the first pieces of paperwork you'll get is a seller's property disclosure. Also known as a property disclosure statement, home disclosure and real estate disclosure form, this document contains a list of known problems with the home.

Regulation Z also requires mortgage lenders to provide borrowers with a written disclosure of rates, fees and other finance charges. Plus, if you have an adjustable-rate mortgage, they're required to let you know in advance if your rate will be changing.

To comply with the TILA-RESPA Integrated Disclosures rule, both the buyer and seller must receive Closing Disclosures that provide details of the transaction.

Lenders must provide a Truth in Lending (TIL) disclosure statement that includes information about the amount of your loan, the annual percentage rate (APR), finance charges (including application fees, late charges, prepayment penalties), a payment schedule and the total repayment amount over the lifetime of the loan.

The seller of a one-to-four unit residential property completes and delivers to a prospective buyer a statutory form called a Transfer Disclosure Statement (TDS), more generically called a Condition of Property Disclosure Statement.

In California, sellers must provide a Transfer Disclosure Statement (TDS) to any potential buyer whose offer has been accepted. This form asks specific questions about defects or malfunctions the seller may be aware of.

Here are eight common real estate seller disclosures to be aware of, whether you're on the buyer's side or the seller's side. Death in the Home.Neighborhood Nuisances.Hazards.Homeowners' Association Information.Repairs.Water Damage.Missing Items.Other Possible Disclosures.

The bank must disclose information such as the following: Interest rates. Crediting and compounding policies. Service fees. Balance computation method. Minimum balance requirements. Transaction limitations. Time requirements (if applicable)

Lenders must provide a Truth in Lending (TIL) disclosure statement that includes information about the amount of your loan, the annual percentage rate (APR), finance charges (including application fees, late charges, prepayment penalties), a payment schedule and the total repayment amount over the lifetime of the loan.