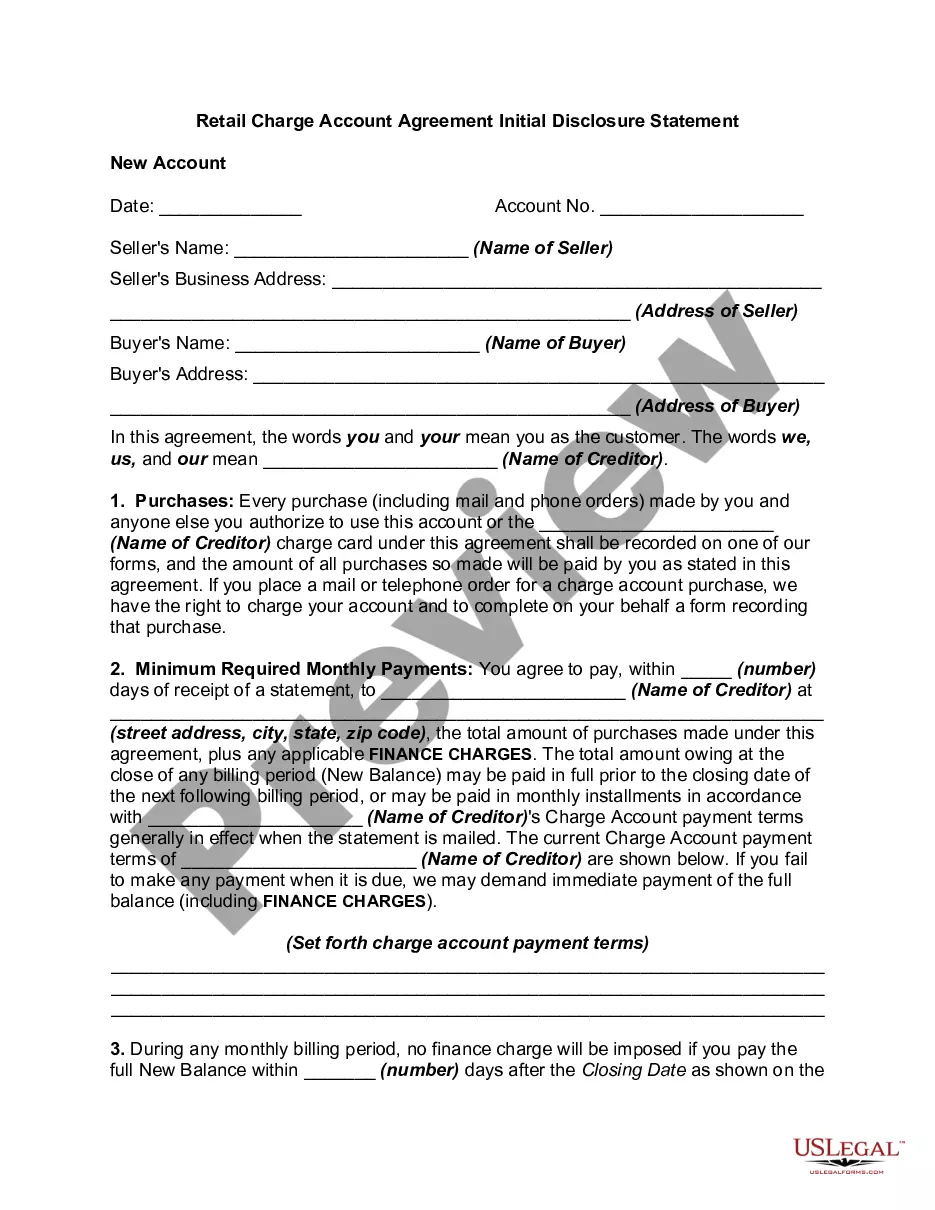

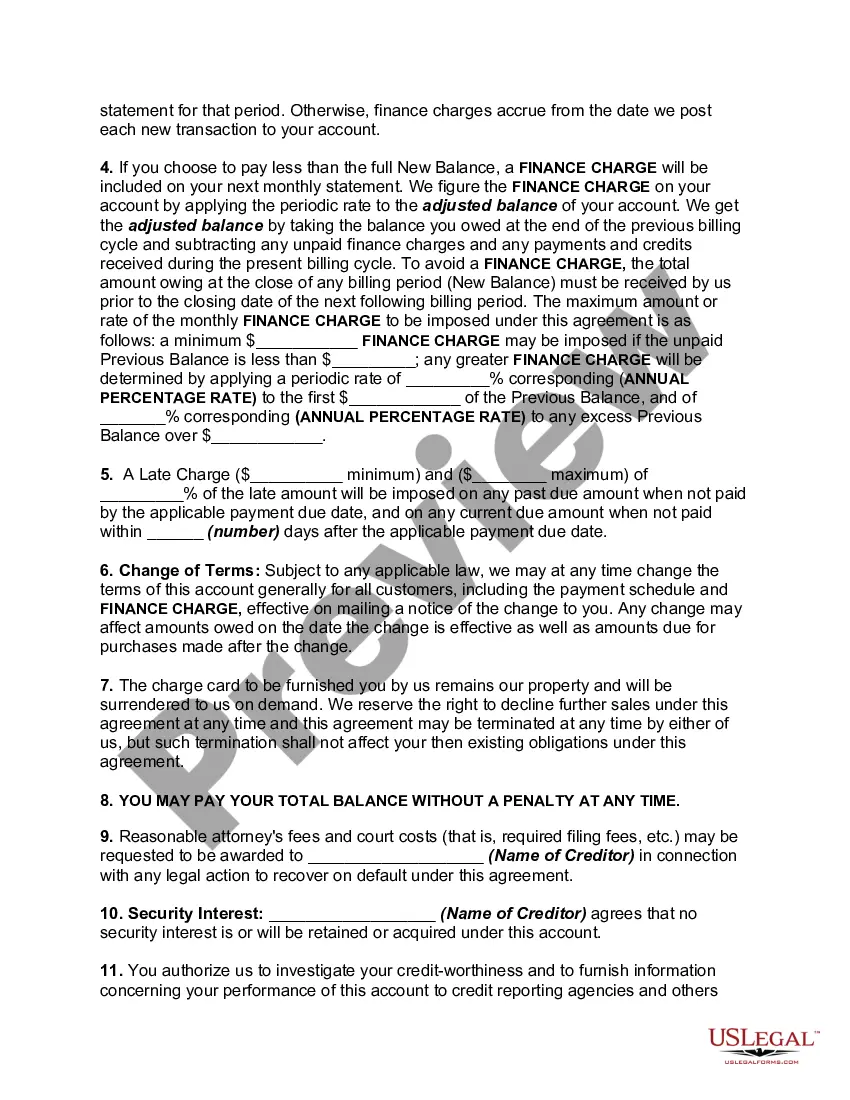

Montgomery Maryland Retail Charge Account Agreement Initial Disclosure Statement is a legal document that outlines the terms and conditions between the creditor (the retailer or merchant) and the customer (the borrower or cardholder) regarding the use of a retail charge account. This agreement serves as a binding contract, governing the customer's use of the credit facility provided by the retailer. The Montgomery Maryland Retail Charge Account Agreement Initial Disclosure Statement provides a comprehensive overview of key information, including interest rates, fees, payment terms, and other important details related to the retail charge account. It is designed to ensure transparency and clarity between the parties involved, promoting responsible credit usage and minimizing potential disputes or misunderstandings. The agreement typically includes the following elements: 1. Introduction: The opening section provides an overview of the agreement, its purpose, and the parties involved. 2. Account Terms: This section outlines the terms and conditions of the retail charge account, including the account holder's rights and obligations, as well as the retailer's responsibilities. It covers topics such as credit limits, card usage, and the availability of additional cardholders. 3. Interest Rates and Fees: The agreement discloses the annual percentage rate (APR) charged on the account balance, as well as any applicable fees such as late payment fees, over-limit fees, or returned payment fees. 4. Billing and Payment: This section explains the customer's billing cycle, the due date for payments, acceptable payment methods, and penalties for late or missed payments. 5. Credit Limit and Available Credit: The agreement specifies the initial credit limit extended to the cardholder and describes how available credit is determined and adjusted. 6. Cardholder Rewards and Benefits: If applicable, this part outlines any rewards programs, cashback offers, or other benefits associated with the retail charge account. 7. Dispute Resolution: The agreement usually includes provisions for resolving disputes between the parties, including arbitration or mediation procedures. 8. Privacy and Data Security: To protect the customer's personal information, the agreement addresses how data will be collected, used, and stored in compliance with applicable privacy laws. Different variations of the Montgomery Maryland Retail Charge Account Agreement Initial Disclosure Statement may exist, tailored for specific retailers or service providers. Examples can include agreements for department stores, gas stations, online retailers, or specialty stores. The content and specific terms of the agreement may vary slightly depending on the nature of the business and the retailer's policies. In conclusion, the Montgomery Maryland Retail Charge Account Agreement Initial Disclosure Statement is a crucial document for both retailers and customers engaging in retail credit transactions. It clarifies the terms and conditions of the retail charge account, ensuring that both parties are aware of their rights and responsibilities.

Montgomery Maryland Retail Charge Account Agreement Initial Disclosure Statement

Description

How to fill out Montgomery Maryland Retail Charge Account Agreement Initial Disclosure Statement?

Draftwing documents, like Montgomery Retail Charge Account Agreement Initial Disclosure Statement, to manage your legal affairs is a tough and time-consumming process. A lot of cases require an attorney’s participation, which also makes this task expensive. However, you can get your legal matters into your own hands and handle them yourself. US Legal Forms is here to the rescue. Our website comes with over 85,000 legal forms crafted for various scenarios and life situations. We make sure each document is in adherence with the regulations of each state, so you don’t have to be concerned about potential legal issues compliance-wise.

If you're already aware of our services and have a subscription with US, you know how effortless it is to get the Montgomery Retail Charge Account Agreement Initial Disclosure Statement template. Simply log in to your account, download the template, and customize it to your needs. Have you lost your document? No worries. You can get it in the My Forms folder in your account - on desktop or mobile.

The onboarding process of new customers is just as simple! Here’s what you need to do before downloading Montgomery Retail Charge Account Agreement Initial Disclosure Statement:

- Make sure that your template is specific to your state/county since the rules for creating legal documents may differ from one state another.

- Discover more information about the form by previewing it or going through a quick intro. If the Montgomery Retail Charge Account Agreement Initial Disclosure Statement isn’t something you were hoping to find, then use the header to find another one.

- Log in or register an account to start utilizing our service and download the form.

- Everything looks great on your end? Click the Buy now button and select the subscription plan.

- Pick the payment gateway and type in your payment information.

- Your template is ready to go. You can try and download it.

It’s an easy task to locate and purchase the needed document with US Legal Forms. Thousands of organizations and individuals are already benefiting from our rich collection. Subscribe to it now if you want to check what other perks you can get with US Legal Forms!

Form popularity

FAQ

The Electronic Fund Transfer Act and Regulation E require institutions to provide certain information to customers regarding electronic fund transfers (EFTs). This disclosure applies to any EFT service you receive from us related to an account established primarily for personal, family or household purposes.

Lenders must provide a Truth in Lending (TIL) disclosure statement that includes information about the amount of your loan, the annual percentage rate (APR), finance charges (including application fees, late charges, prepayment penalties), a payment schedule and the total repayment amount over the lifetime of the loan.

Financial institutions must make the required disclosures at the time a consumer contracts for an electronic fund transfer service or before the first electronic fund transfer is made involving the consumer's account (12 CFR 1005.7(a)).

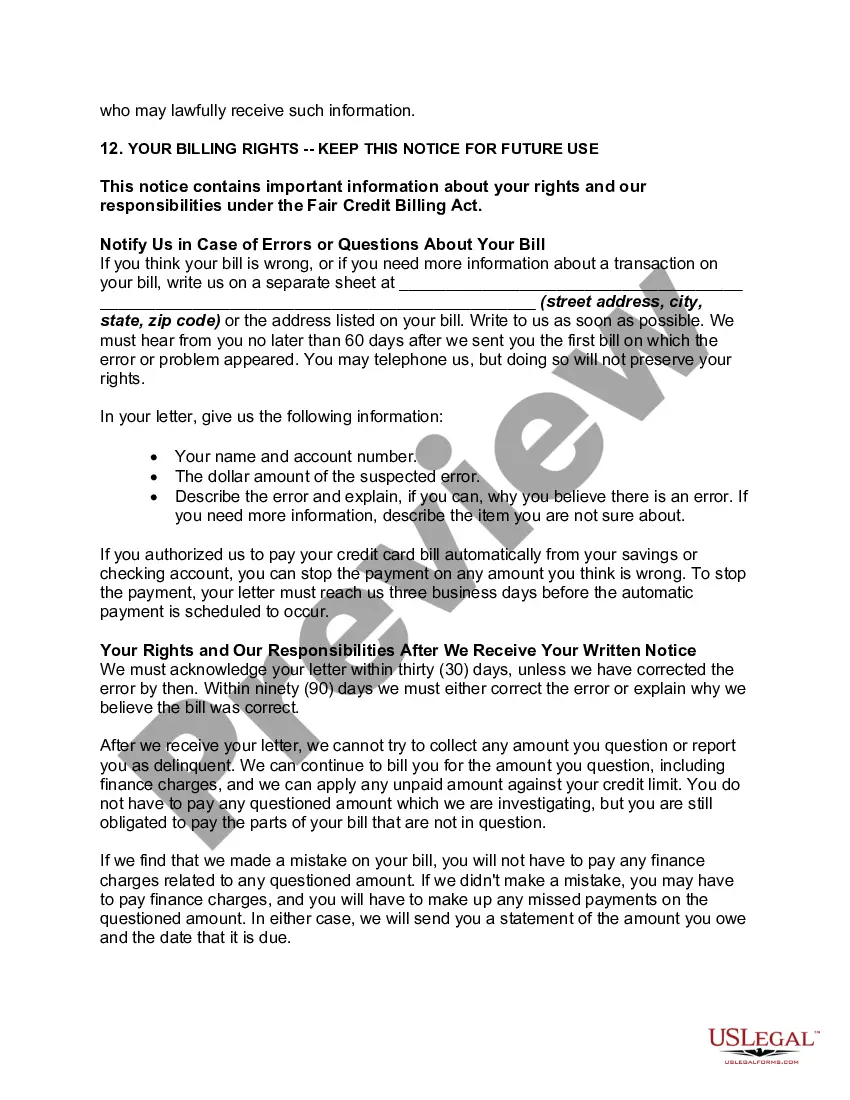

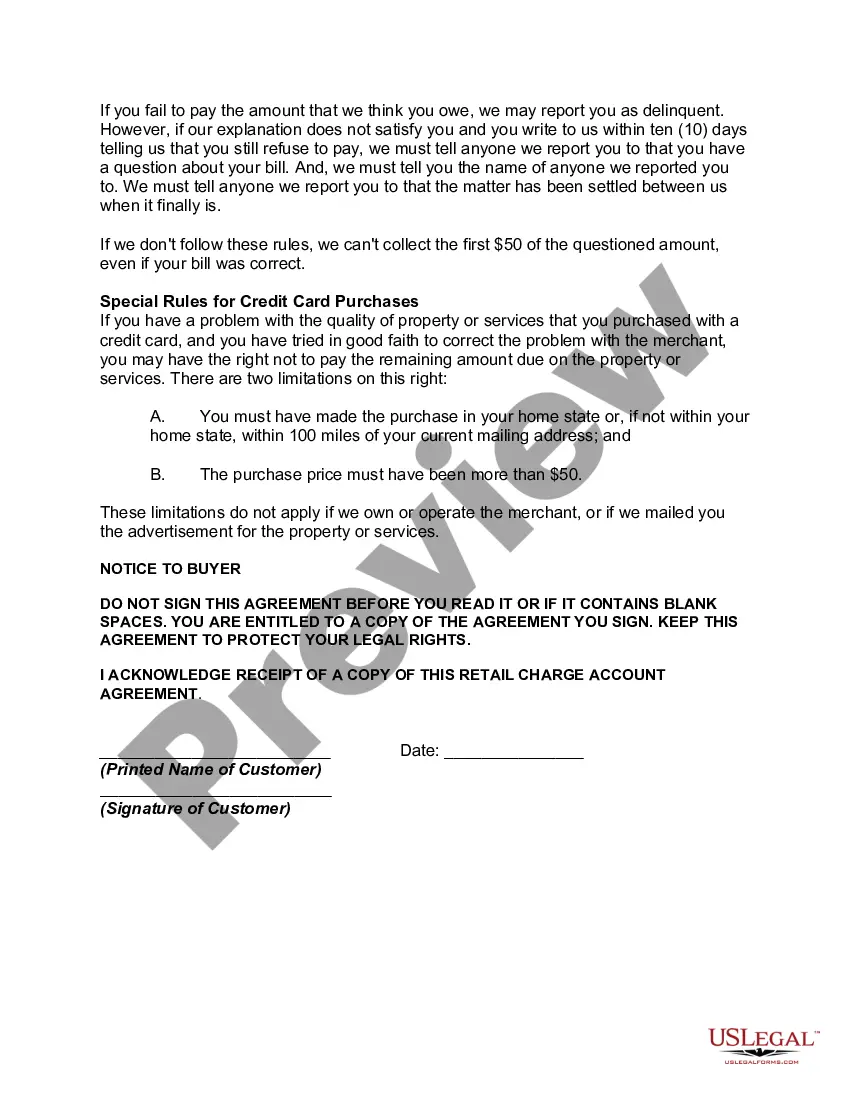

The Truth in Lending Act (TILA) protects you against inaccurate and unfair credit billing and credit card practices. It requires lenders to provide you with loan cost information so that you can comparison shop for certain types of loans.

To make an EFT payment, the sender must know the recipient's bank account information. If you're making an EFT payment, you must authorize the funds transfer. Then, the money is taken from your account and deposited into the recipient's account. There might be a fee for some EFT transactions.

These requirements include keeping track of consumer agreements, providing periodic statements, error resolution, reimbursement of fees incorrectly charged to the consumer, providing access to account information, disclosing a telephone number that the consumer can use to contact the financial institution, and so on.

Regulation Z also requires mortgage lenders to provide borrowers with a written disclosure of rates, fees and other finance charges. Plus, if you have an adjustable-rate mortgage, they're required to let you know in advance if your rate will be changing.

1. Disclosure of EFT fees. An institution is required to disclose all fees for EFTs or the right to make them. Others fees (for example, minimum-balance fees, stop-payment fees, or account overdrafts) may, but need not, be disclosed.

The bank must disclose information such as the following: Interest rates. Crediting and compounding policies. Service fees. Balance computation method. Minimum balance requirements. Transaction limitations. Time requirements (if applicable)