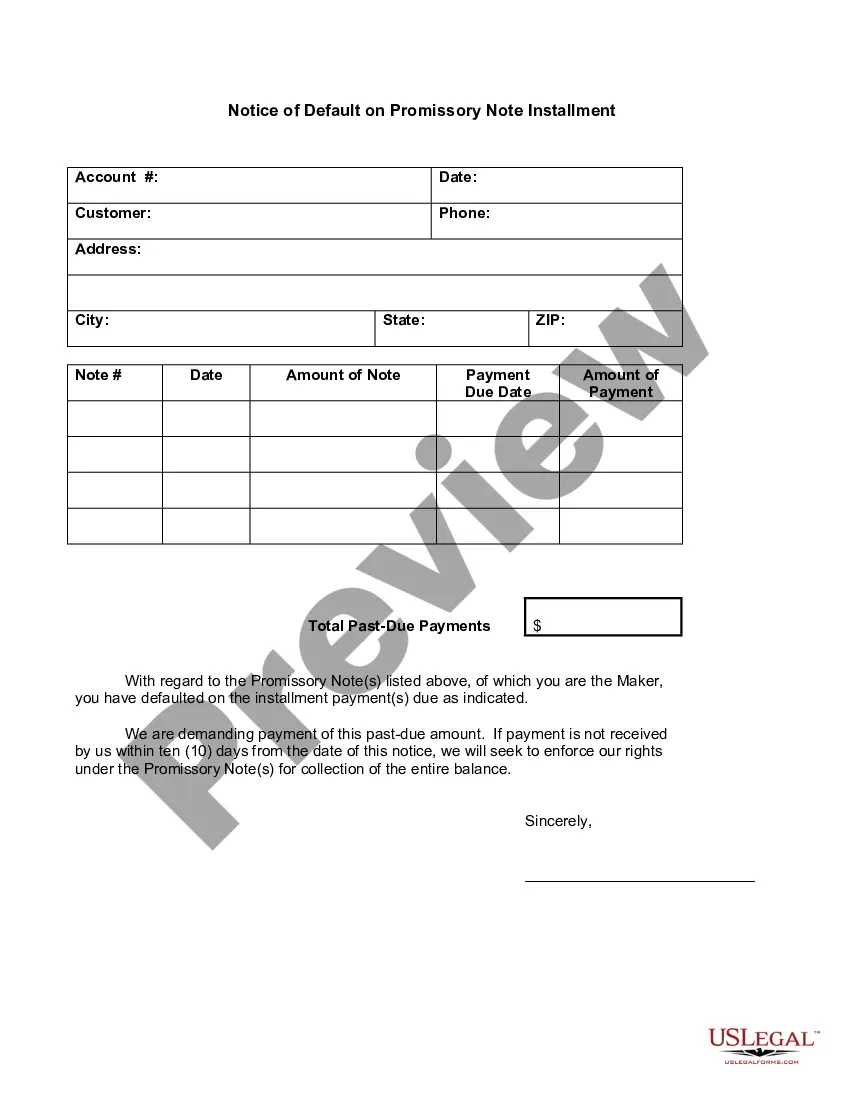

Fulton County, Georgia is located in the state of Georgia and is home to several cities, including Atlanta. The Fulton County Superior Court handles various legal matters, including the issuance of notices of default on promissory note installments. A Fulton Georgia Notice of Default on Promissory Note Installment is a legal document that is typically sent to a borrower who has failed to make their installment payments on a promissory note. This notice serves as a formal communication from the lender, informing the borrower of their default and the actions that may be taken if the default is not rectified. There are different types of Fulton Georgia Notices of Default on Promissory Note Installment, which may vary depending on the specific circumstances and the type of loan agreement. Some common types may include: 1. Residential Mortgage Notice of Default: This type of notice is issued when a borrower defaults on their mortgage loan for a residential property in Fulton County. The lender typically outlines the outstanding amount, the missed payments, and the consequences of continued default. 2. Commercial Loan Notice of Default: This notice is sent to a borrower who has defaulted on their commercial loan in Fulton County. It details the amount owed, the missed payments, and the potential legal actions that the lender may take if the default is not resolved. 3. Auto Loan Notice of Default: In cases where a borrower has failed to make their installment payments on an auto loan in Fulton County, this notice is issued. It includes information regarding the outstanding balance, missed payments, and the next steps the lender may take. 4. Personal Loan Notice of Default: This notice is applicable when a borrower has defaulted on a personal loan in Fulton County. It outlines the amount due, the missed payments, and informs the borrower about the potential legal consequences of continued default. It is important for borrowers to understand the implications of a Fulton Georgia Notice of Default on Promissory Note Installment. They should carefully review the notice, seek legal advice if necessary, and promptly communicate with the lender to explore potential solutions or negotiate alternative payment arrangements to avoid further legal actions.

Fulton Georgia Notice of Default on Promissory Note Installment

Description

How to fill out Fulton Georgia Notice Of Default On Promissory Note Installment?

Draftwing documents, like Fulton Notice of Default on Promissory Note Installment, to take care of your legal matters is a challenging and time-consumming process. A lot of cases require an attorney’s participation, which also makes this task not really affordable. However, you can acquire your legal issues into your own hands and handle them yourself. US Legal Forms is here to save the day. Our website comes with more than 85,000 legal documents created for a variety of cases and life situations. We make sure each document is in adherence with the regulations of each state, so you don’t have to worry about potential legal issues associated with compliance.

If you're already aware of our services and have a subscription with US, you know how easy it is to get the Fulton Notice of Default on Promissory Note Installment form. Simply log in to your account, download the template, and personalize it to your needs. Have you lost your document? Don’t worry. You can get it in the My Forms folder in your account - on desktop or mobile.

The onboarding process of new customers is just as simple! Here’s what you need to do before downloading Fulton Notice of Default on Promissory Note Installment:

- Ensure that your form is specific to your state/county since the rules for writing legal papers may vary from one state another.

- Discover more information about the form by previewing it or going through a brief intro. If the Fulton Notice of Default on Promissory Note Installment isn’t something you were looking for, then use the header to find another one.

- Log in or create an account to begin using our service and get the document.

- Everything looks good on your side? Click the Buy now button and select the subscription plan.

- Select the payment gateway and type in your payment details.

- Your form is ready to go. You can go ahead and download it.

It’s easy to locate and purchase the appropriate document with US Legal Forms. Thousands of businesses and individuals are already taking advantage of our extensive collection. Subscribe to it now if you want to check what other advantages you can get with US Legal Forms!