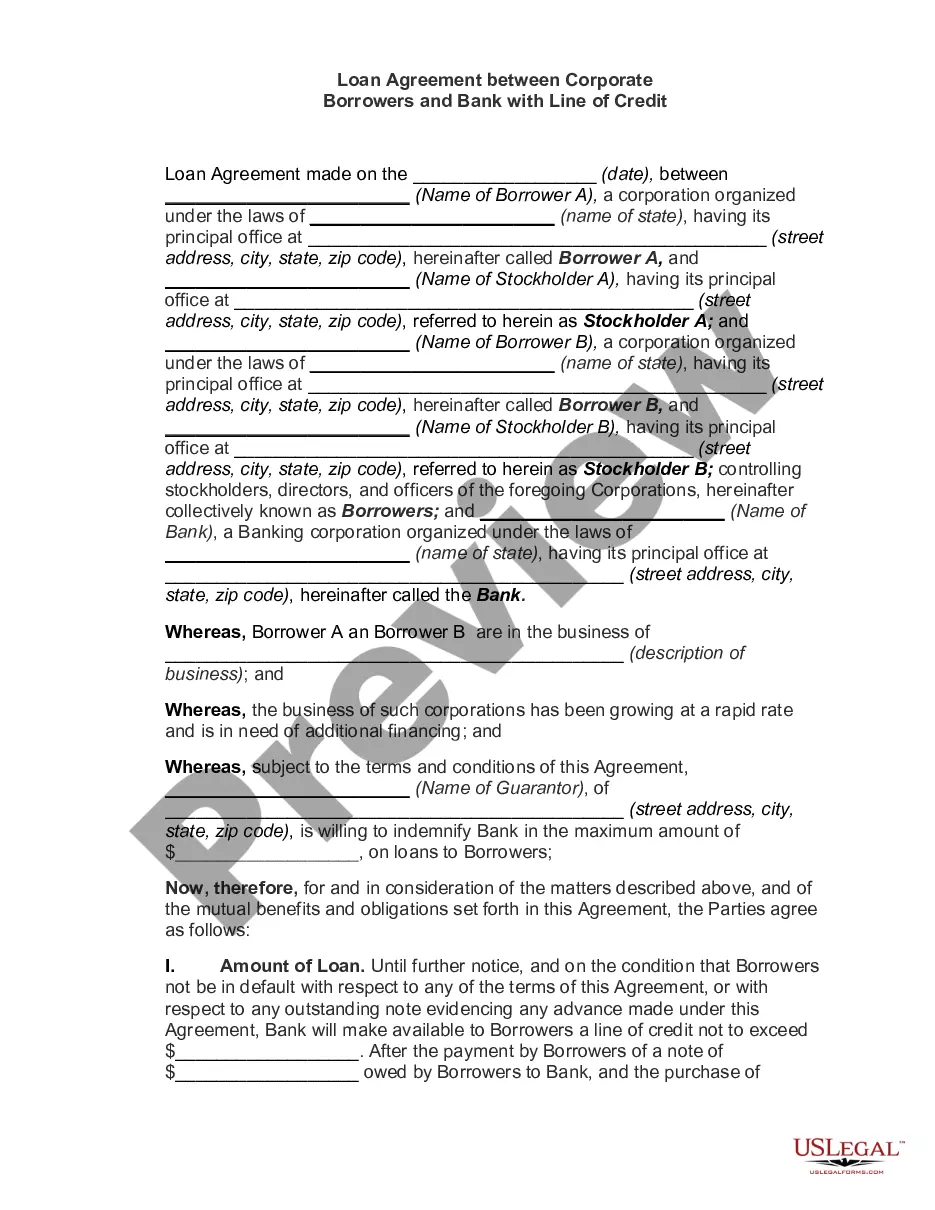

As a general matter, a loan by a bank is the borrowing of money by a person or entity who promises to return it on or before a specific date, with interest, or who pledges collateral as security for the loan and promises to redeem it at a specific later date. Loans are usually made on the basis of applications, together with financial statements submitted by the applicants.

The Federal Truth in Lending Act and the regulations promulgated under the Act apply to certain credit transactions, primarily those involving loans made to a natural person and intended for personal, family, or household purposes and for which a finance charge is made, or loans that are payable in more than four installments. However, said Act and regulations do not apply to a business loan of this type.

Fairfax Virginia Term Loan Agreement between Business or Corporate Borrower and Bank

Category:

State:

Multi-State

County:

Fairfax

Control #:

US-02922BG

Format:

Word;

Rich Text

Instant download

Description

Free preview

How to fill out Term Loan Agreement Between Business Or Corporate Borrower And Bank?

A document routine invariably accompanies any legal endeavor you undertake.

Establishing a business, applying for or accepting a job proposal, transferring ownership, and numerous other life situations require you to prepare formal documents that vary from one state to another.

This is why having everything organized in one location is extremely beneficial.

US Legal Forms is the largest online repository of up-to-date federal and state-specific legal templates.

This is the easiest and most dependable way to acquire legal documents. All the samples provided by our library are professionally crafted and verified for compliance with local laws and regulations. Prepare your documentation and manage your legal matters efficiently with US Legal Forms!

- Here, you can effortlessly find and obtain a document for any personal or corporate purpose used in your locality, including the Fairfax Term Loan Agreement between Business or Corporate Borrower and Bank.

- Finding samples on the platform is incredibly straightforward.

- If you already have a subscription to our service, Log In to your account, locate the sample using the search function, and click Download to save it on your device.

- After that, the Fairfax Term Loan Agreement between Business or Corporate Borrower and Bank will be available for further use in the My documents section of your profile.

- If this is your first time using US Legal Forms, follow this quick guide to acquire the Fairfax Term Loan Agreement between Business or Corporate Borrower and Bank.

- Make sure you have opened the right page with your local form.

- Utilize the Preview mode (if available) and browse through the sample.

- Examine the description (if any) to confirm the form meets your requirements.

- Search for another document using the search feature if the sample doesn't suit you.

- Click Buy Now when you find the template you need.

Form popularity

FAQ

What Are Loan Terms? Loan terms refers to the terms and conditions involved when borrowing money. This can include the loan's repayment period, the interest rate and fees associated with the loan, penalty fees borrowers might be charged, and any other special conditions that may apply.

Loan Terms Definition: Term Length When you take out a loan, you'll pay it back slowly over time through monthly payments. At some point, you'll have repaid the entire loan and you'll be free of the debt. The amount of time the lender gives you to repay your loan is called the term length, or your loan term.

A personal loan contract is a legally binding document regardless of whether the lender is a financial institution or another person. The consequences are the same if you default on the contract. As a borrower, you could be sued by the lender or lose the asset or assets used to secure the loan.

Repayment terms: How long you have to pay back the loan. Loan amounts: Total amount you can borrow from a lender. Interest rates: Amount the lender charges for the loan, usually stated as a percentage Time to funding: Amount of time it will take to receive the actual funds.

Breach or Default If a loan contract is paid off late, the loan is considered in default. The borrower can be liable for a myriad of potential legal damages to compensate the lender for any losses suffered.

Lender has the right to obtain information on Borrower's operations, financial activities, inventory, use of the loan, etc., and request Borrower to provide documents, materials and information such as financial statements. Lender's Rights and Obligations.

Loan agreements, like any contract, reflect an "offer," the "acceptance of the offer," "consideration," and can only involve situations that are "legal" (a term loan agreement involving heroin drug sales is not "legal").

To make out a claim for breach of a loan agreement is simple; you need to plead and prove the following: (a) you lent money to the borrower; (b) the borrower promised to pay you back; and (c) the borrower did not repay you in full.

10 Essential Loan Agreement Provisions Identity of the Parties. The names of the lender and borrower need to be stated.Date of the Agreement.Interest Rate.Repayment Terms.Default provisions.Signatures.Choice of Law.Severability.

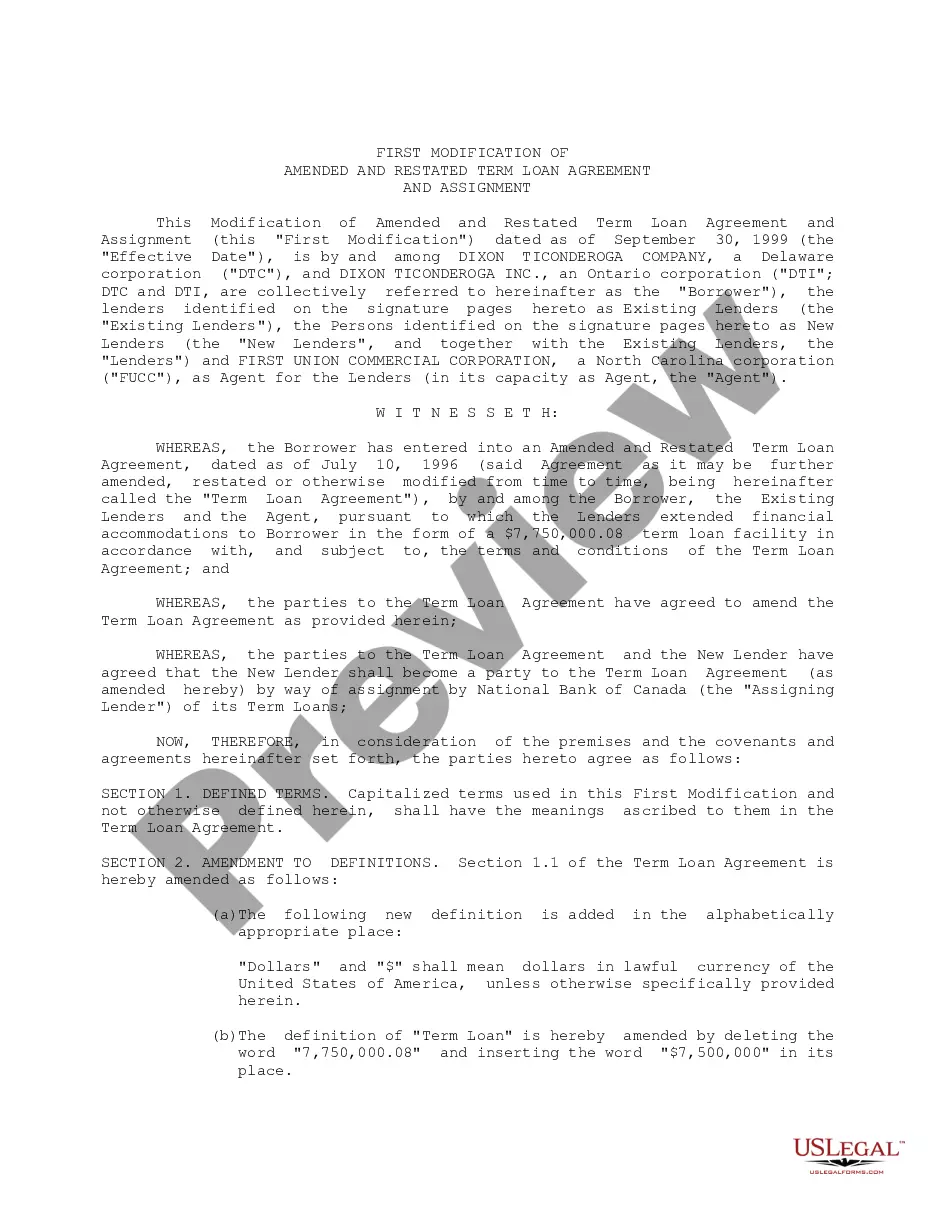

Integrated Agreement; Amendment. This Amendment, together with the Loan Agreement and the Loan Documents, constitutes the entire agreement between Lender and Borrower concerning the subject matter hereof, and may not be altered or amended except by written agreement signed by Lender.