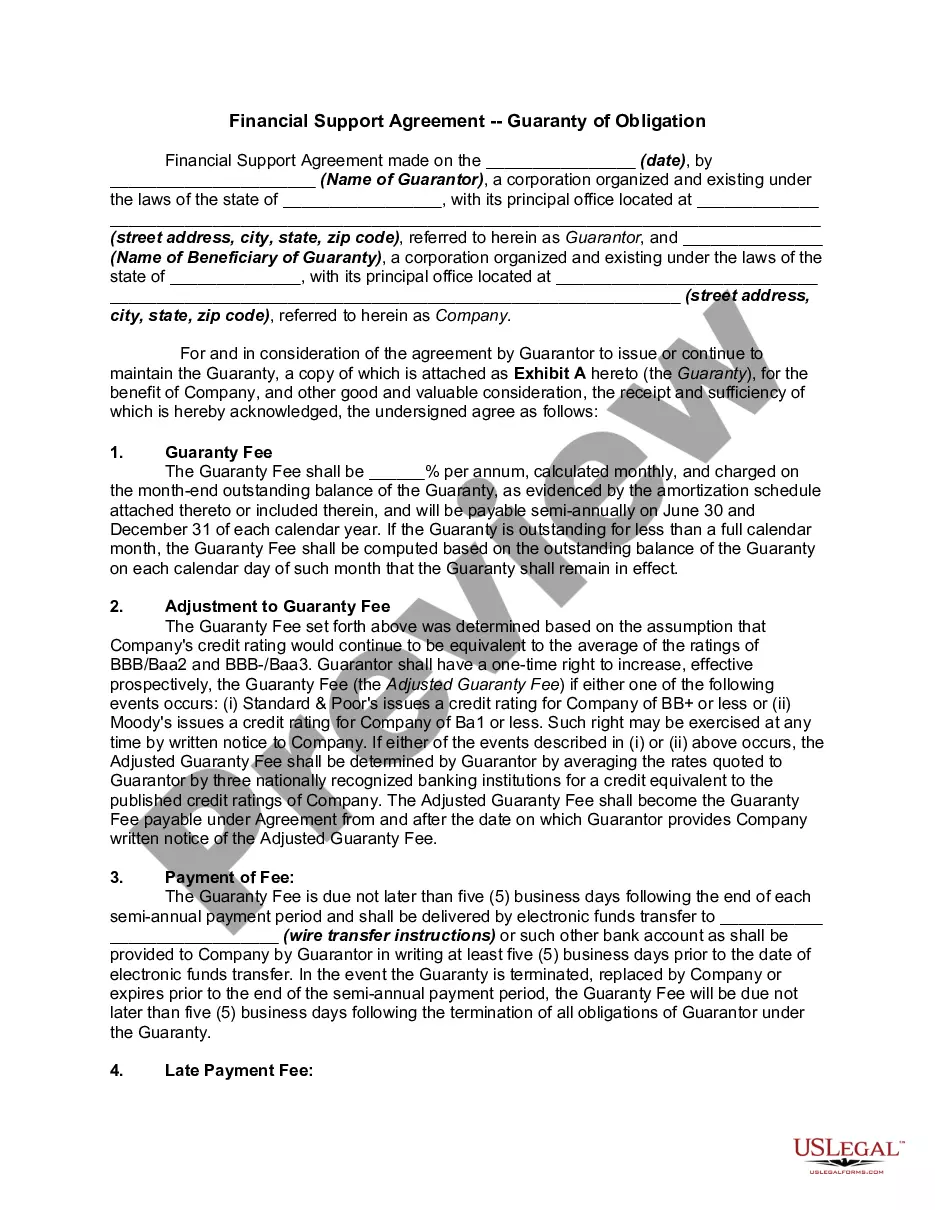

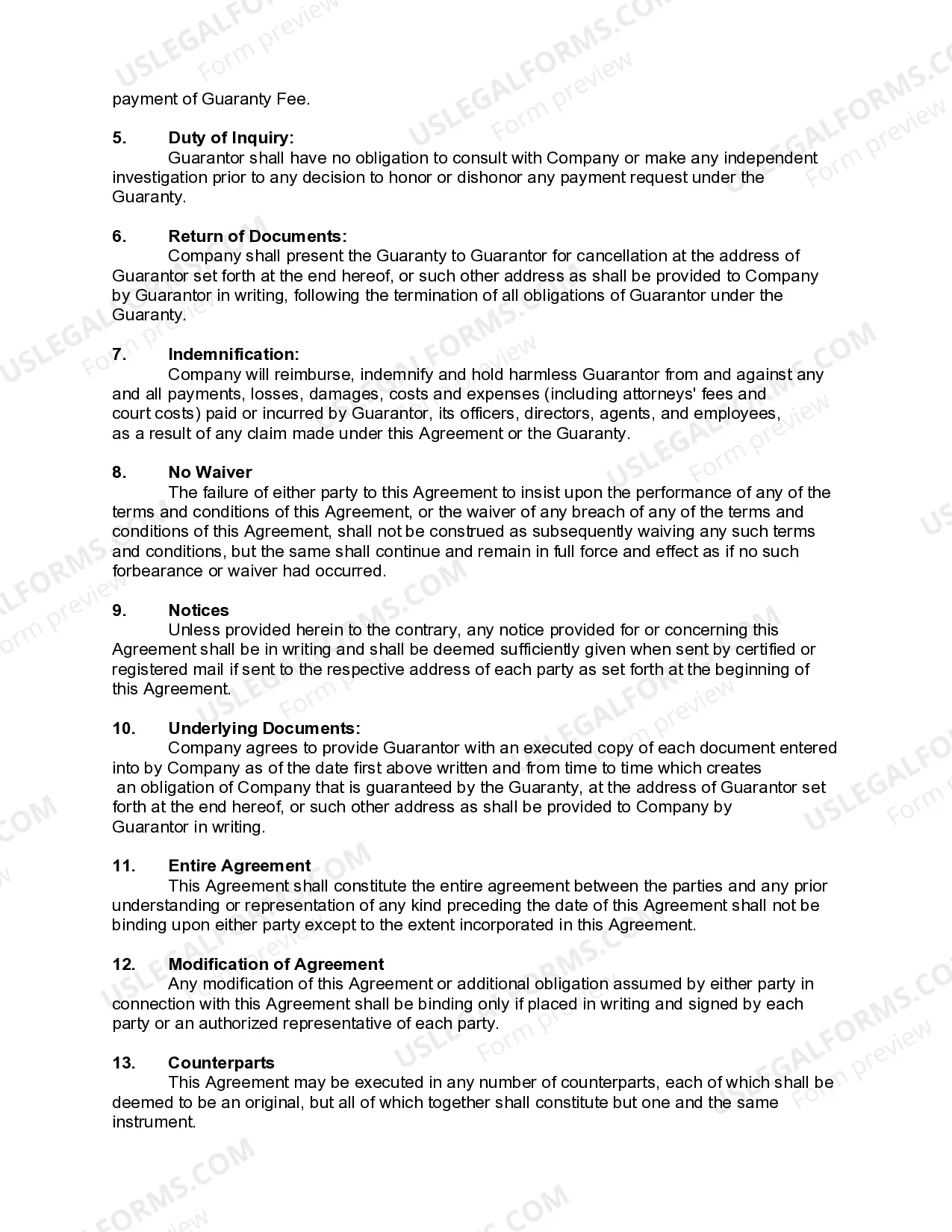

In this agreement, one corporation (the Guarantor) is providing financial assistance to another Corporation (the Corporation) by guaranteeing certain indebtedness for the Company in exchange for a guaranty fee.

This form is a generic example that may be referred to when preparing such a form for your particular state. It is for illustrative purposes only. Local laws should be consulted to determine any specific requirements for such a form in a particular jurisdiction.

Fairfax Virginia Financial Support Agreement — Guaranty of Obligation is a legal contract that provides a framework for obtaining financial support and ensuring the fulfillment of obligations. This agreement is commonly used in business transactions, partnerships, and loan agreements to establish a guarantee of financial backing. The Fairfax Virginia Financial Support Agreement — Guaranty of Obligation safeguards the interests of parties involved by outlining the terms and conditions under which a guarantor agrees to support the financial obligations of another party. The guarantor, usually an individual or business entity, undertakes the responsibility of repaying the debts or obligations in situations where the primary debtor fails to fulfill their financial commitments. This agreement serves as a form of security for the lender or recipient of financial support. Depending on the specific requirements of the parties involved, there can be various types of Fairfax Virginia Financial Support Agreement — Guaranty of Obligation. Some common variations may include: 1. Personal Guaranty: In this type of agreement, an individual guarantees the financial obligations of another party. This is commonly seen in loan agreements where a personal guarantor promises to repay the loan if the borrower defaults. 2. Corporate Guaranty: This agreement is used when a corporation or business entity guarantees the financial obligations of another entity. It provides a level of assurance to lenders or creditors that they will receive payment even if the primary debtor fails to meet their obligations. 3. Limited Guaranty: A limited guaranty agreement specifies the scope and extent of the guarantor's obligations. Unlike a general guaranty, where the guarantor undertakes complete responsibility for the debt, a limited guaranty restricts the guarantor's liability to a specific amount or timeframe. 4. Continuing Guaranty: This type of agreement remains in effect until formally terminated or revoked. It covers any existing or future financial obligations that may arise between the primary debtor and the lender or creditor. 5. Absolute Guaranty: An absolute guaranty is an unconditional commitment by the guarantor to fulfill the financial obligations of the primary debtor. It does not require any specific conditions to be met before the guarantor's liability is triggered. The Fairfax Virginia Financial Support Agreement — Guaranty of Obligation is a crucial legal instrument that provides security and assurance to all parties involved in financial transactions. By clearly defining the responsibilities and liabilities of the guarantor, this agreement helps mitigate risks and enables smooth business operations.Fairfax Virginia Financial Support Agreement — Guaranty of Obligation is a legal contract that provides a framework for obtaining financial support and ensuring the fulfillment of obligations. This agreement is commonly used in business transactions, partnerships, and loan agreements to establish a guarantee of financial backing. The Fairfax Virginia Financial Support Agreement — Guaranty of Obligation safeguards the interests of parties involved by outlining the terms and conditions under which a guarantor agrees to support the financial obligations of another party. The guarantor, usually an individual or business entity, undertakes the responsibility of repaying the debts or obligations in situations where the primary debtor fails to fulfill their financial commitments. This agreement serves as a form of security for the lender or recipient of financial support. Depending on the specific requirements of the parties involved, there can be various types of Fairfax Virginia Financial Support Agreement — Guaranty of Obligation. Some common variations may include: 1. Personal Guaranty: In this type of agreement, an individual guarantees the financial obligations of another party. This is commonly seen in loan agreements where a personal guarantor promises to repay the loan if the borrower defaults. 2. Corporate Guaranty: This agreement is used when a corporation or business entity guarantees the financial obligations of another entity. It provides a level of assurance to lenders or creditors that they will receive payment even if the primary debtor fails to meet their obligations. 3. Limited Guaranty: A limited guaranty agreement specifies the scope and extent of the guarantor's obligations. Unlike a general guaranty, where the guarantor undertakes complete responsibility for the debt, a limited guaranty restricts the guarantor's liability to a specific amount or timeframe. 4. Continuing Guaranty: This type of agreement remains in effect until formally terminated or revoked. It covers any existing or future financial obligations that may arise between the primary debtor and the lender or creditor. 5. Absolute Guaranty: An absolute guaranty is an unconditional commitment by the guarantor to fulfill the financial obligations of the primary debtor. It does not require any specific conditions to be met before the guarantor's liability is triggered. The Fairfax Virginia Financial Support Agreement — Guaranty of Obligation is a crucial legal instrument that provides security and assurance to all parties involved in financial transactions. By clearly defining the responsibilities and liabilities of the guarantor, this agreement helps mitigate risks and enables smooth business operations.