This form is a type of asset-financing arrangement in which a company uses its receivables (money owed by customers) as collateral in a financing agreement. The company receives an amount that is equal to a reduced value of the receivables pledged. The age of the receivables have a large effect on the amount a company will receive. The older the receivables, the less the company can expect.

This type of financing helps companies free up capital that is stuck in accounts receivables. Accounts receivable financing transfers the default risk associated with the accounts receivables to the financing company. This transfer of risk can help the company using the financing to shift focus from trying to collect receivables to current business activities.

This form is a generic example that may be referred to when preparing such a form for your particular state. It is for illustrative purposes only. Local laws should be consulted to determine any specific requirements for such a form in a particular jurisdiction.

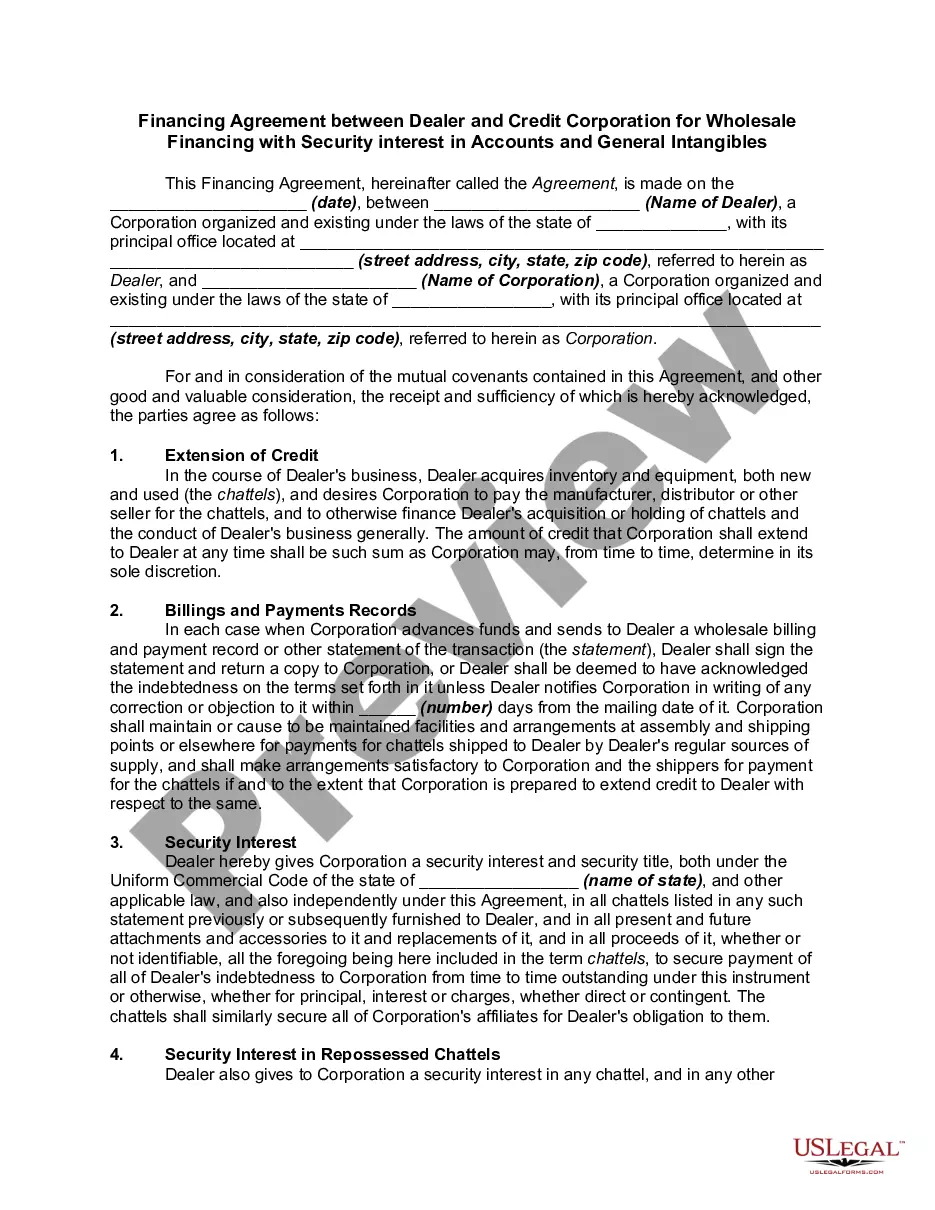

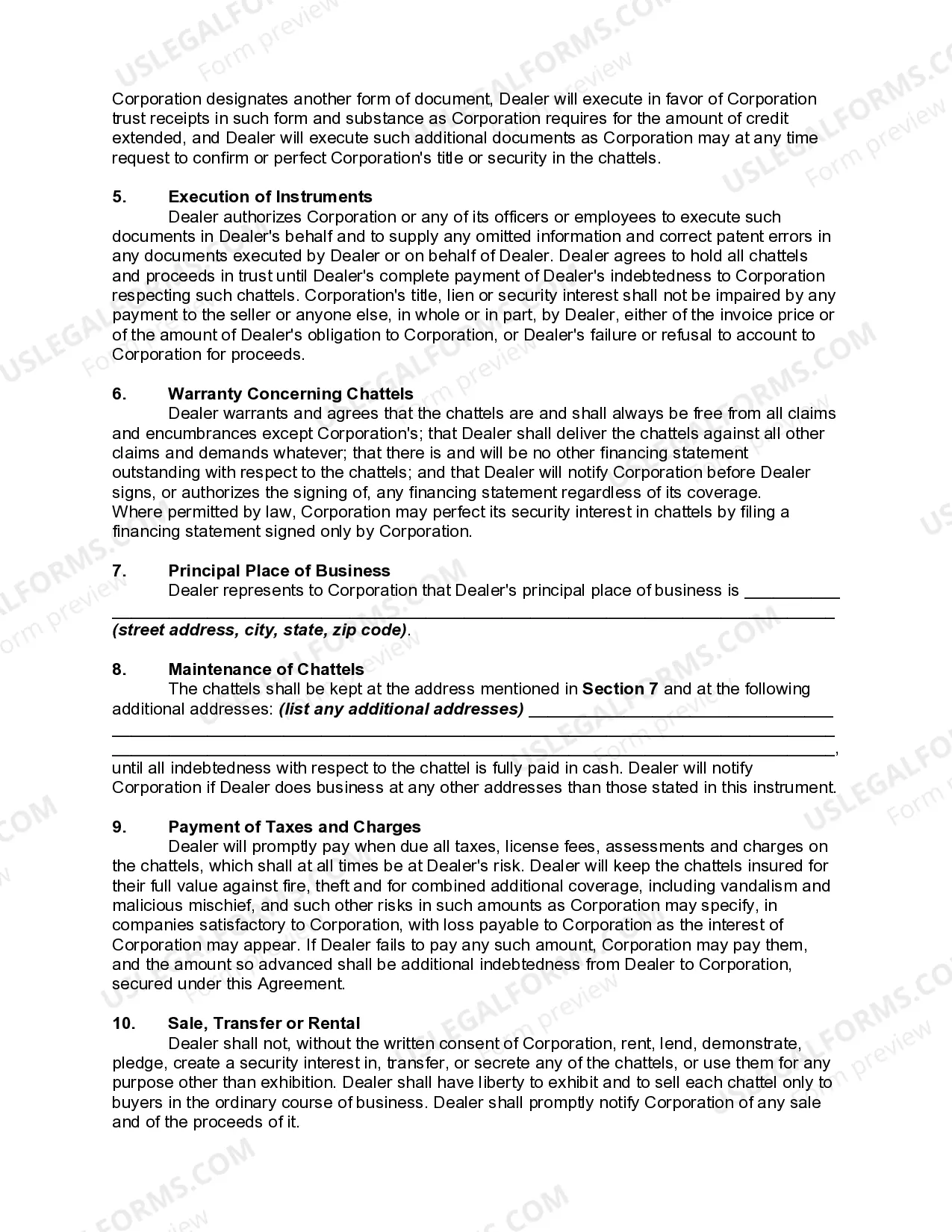

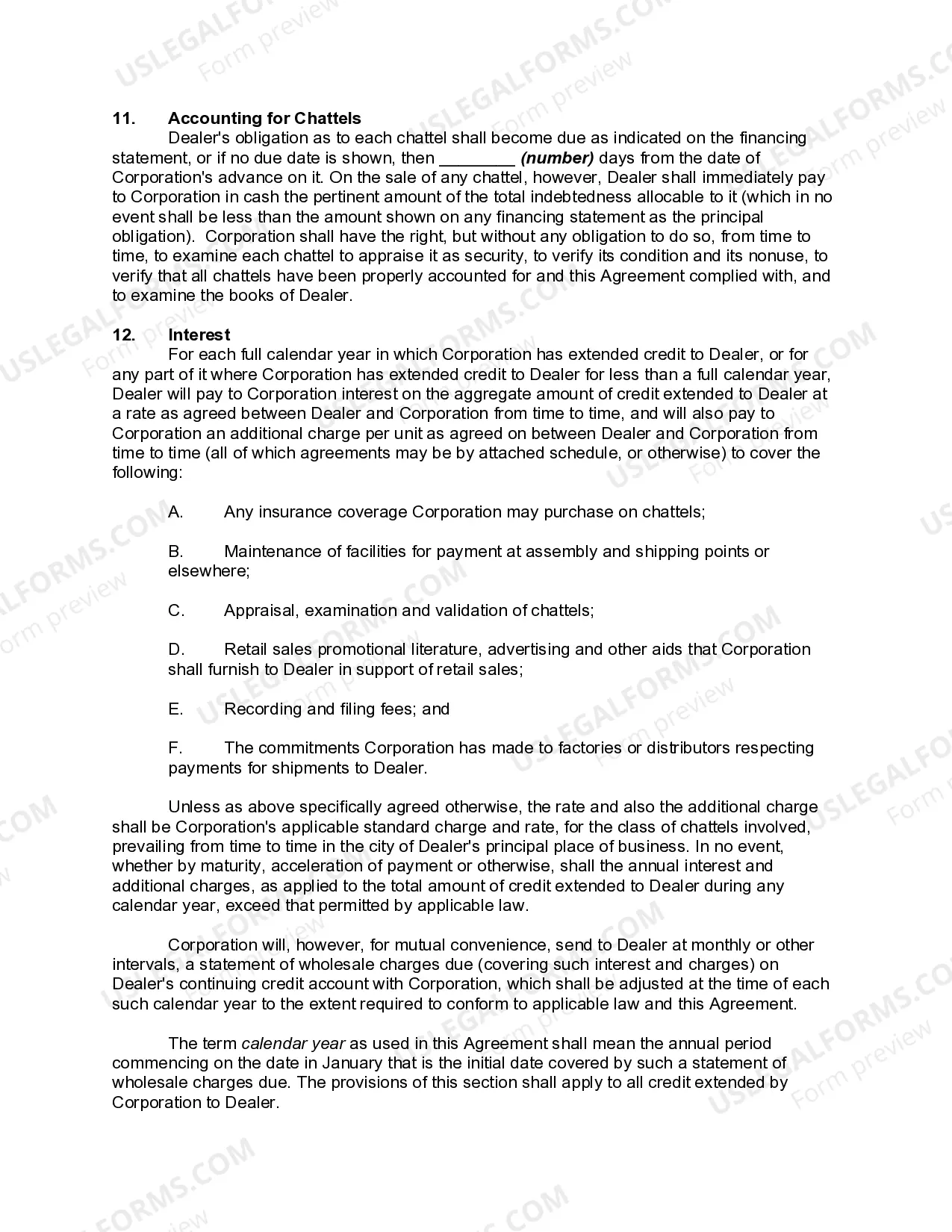

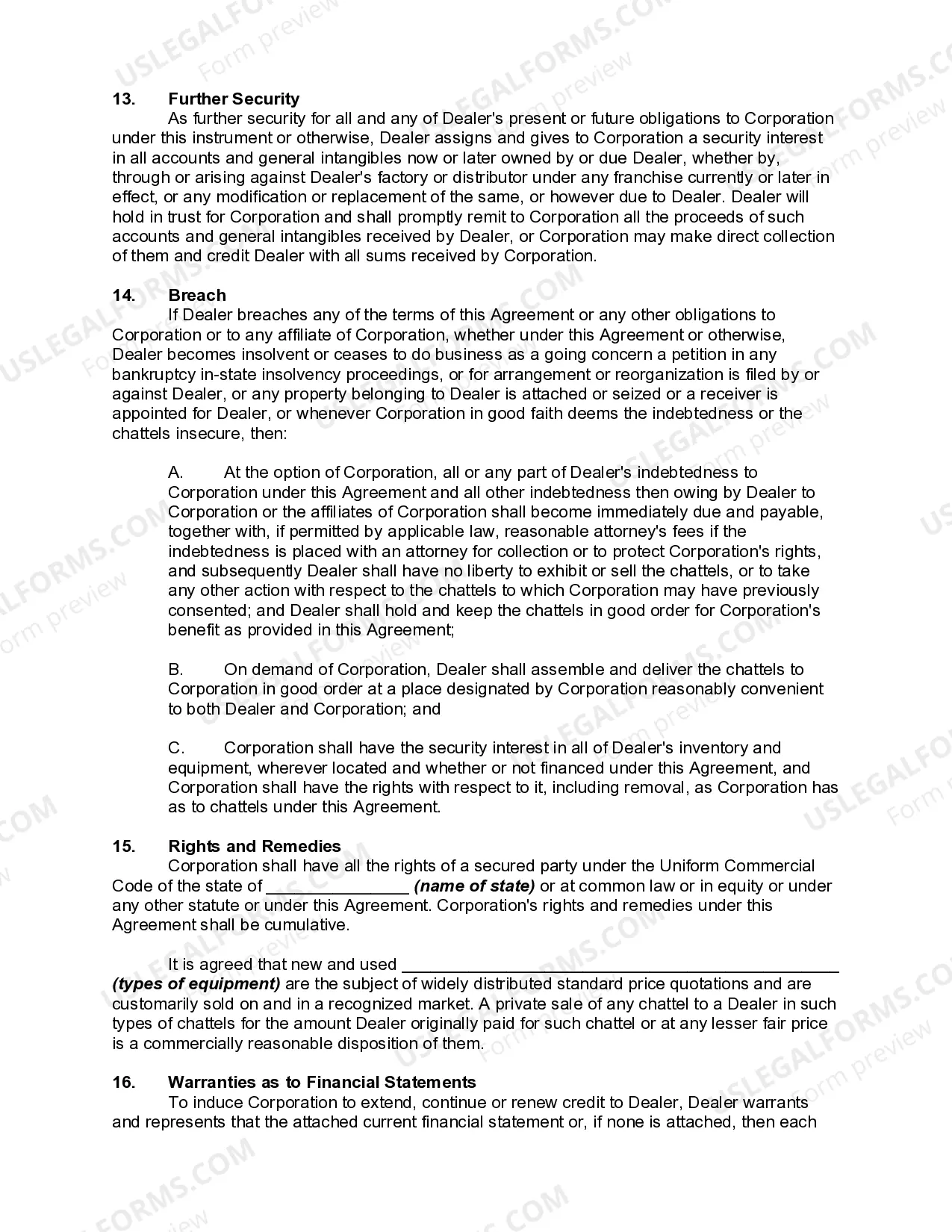

The Bexar Texas Financing Agreement between Dealer and Credit Corporation for Wholesale Financing with Security interest in Accounts and General Intangibles is a legal document that outlines the terms and conditions of a financial arrangement between a dealer and a credit corporation. This agreement is specific to the state of Texas and pertains to wholesale financing, where the credit corporation provides funds to the dealer for purchasing inventory or other assets. The primary purpose of this agreement is to establish a secure and mutually beneficial relationship between the dealer and the credit corporation. It ensures that the dealer has access to the necessary capital to maintain and expand their inventory, while the credit corporation maintains security by retaining an interest in the dealer's accounts and general intangibles. The specific terms of the financing agreement may vary depending on the parties involved and their individual requirements. However, some common elements are typically included. These may include: 1. Loan Terms: The agreement will clearly state the amount of funds provided by the credit corporation, the interest rate, and any additional fees or charges that may apply. It may also outline the repayment schedule and any penalties for early repayment or default. 2. Security Interest: The agreement will establish the credit corporation's security interest in the dealer's accounts and general intangibles. This means that the credit corporation has the right to reclaim these assets in the event of default or non-payment. 3. Collateral: In addition to the security interest, the agreement may specify additional collateral that the dealer must provide to secure the loan. This could include inventory, equipment, or other assets that have an established value. 4. Reporting Requirements: The dealer may be required to provide regular reports to the credit corporation, such as financial statements or inventory updates. This ensures that both parties have up-to-date information about the dealer's financial status and inventory levels. There may be different types of Bexar Texas Financing Agreements between Dealer and Credit Corporation for Wholesale Financing with Security interest in Accounts and General Intangibles, depending on the specific nature of the transaction or the parties involved. These may include variations based on loan amount, term duration, or specific industry requirements. It is important for both parties to carefully review and understand the terms and conditions of the agreement before signing. Seeking legal counsel or consulting with financial professionals is advised to ensure that the agreement protects the interests of both the dealer and the credit corporation.The Bexar Texas Financing Agreement between Dealer and Credit Corporation for Wholesale Financing with Security interest in Accounts and General Intangibles is a legal document that outlines the terms and conditions of a financial arrangement between a dealer and a credit corporation. This agreement is specific to the state of Texas and pertains to wholesale financing, where the credit corporation provides funds to the dealer for purchasing inventory or other assets. The primary purpose of this agreement is to establish a secure and mutually beneficial relationship between the dealer and the credit corporation. It ensures that the dealer has access to the necessary capital to maintain and expand their inventory, while the credit corporation maintains security by retaining an interest in the dealer's accounts and general intangibles. The specific terms of the financing agreement may vary depending on the parties involved and their individual requirements. However, some common elements are typically included. These may include: 1. Loan Terms: The agreement will clearly state the amount of funds provided by the credit corporation, the interest rate, and any additional fees or charges that may apply. It may also outline the repayment schedule and any penalties for early repayment or default. 2. Security Interest: The agreement will establish the credit corporation's security interest in the dealer's accounts and general intangibles. This means that the credit corporation has the right to reclaim these assets in the event of default or non-payment. 3. Collateral: In addition to the security interest, the agreement may specify additional collateral that the dealer must provide to secure the loan. This could include inventory, equipment, or other assets that have an established value. 4. Reporting Requirements: The dealer may be required to provide regular reports to the credit corporation, such as financial statements or inventory updates. This ensures that both parties have up-to-date information about the dealer's financial status and inventory levels. There may be different types of Bexar Texas Financing Agreements between Dealer and Credit Corporation for Wholesale Financing with Security interest in Accounts and General Intangibles, depending on the specific nature of the transaction or the parties involved. These may include variations based on loan amount, term duration, or specific industry requirements. It is important for both parties to carefully review and understand the terms and conditions of the agreement before signing. Seeking legal counsel or consulting with financial professionals is advised to ensure that the agreement protects the interests of both the dealer and the credit corporation.