This form is a type of asset-financing arrangement in which a company uses its receivables (money owed by customers) as collateral in a financing agreement. The company receives an amount that is equal to a reduced value of the receivables pledged. The age of the receivables have a large effect on the amount a company will receive. The older the receivables, the less the company can expect.

This type of financing helps companies free up capital that is stuck in accounts receivables. Accounts receivable financing transfers the default risk associated with the accounts receivables to the financing company. This transfer of risk can help the company using the financing to shift focus from trying to collect receivables to current business activities.

This form is a generic example that may be referred to when preparing such a form for your particular state. It is for illustrative purposes only. Local laws should be consulted to determine any specific requirements for such a form in a particular jurisdiction.

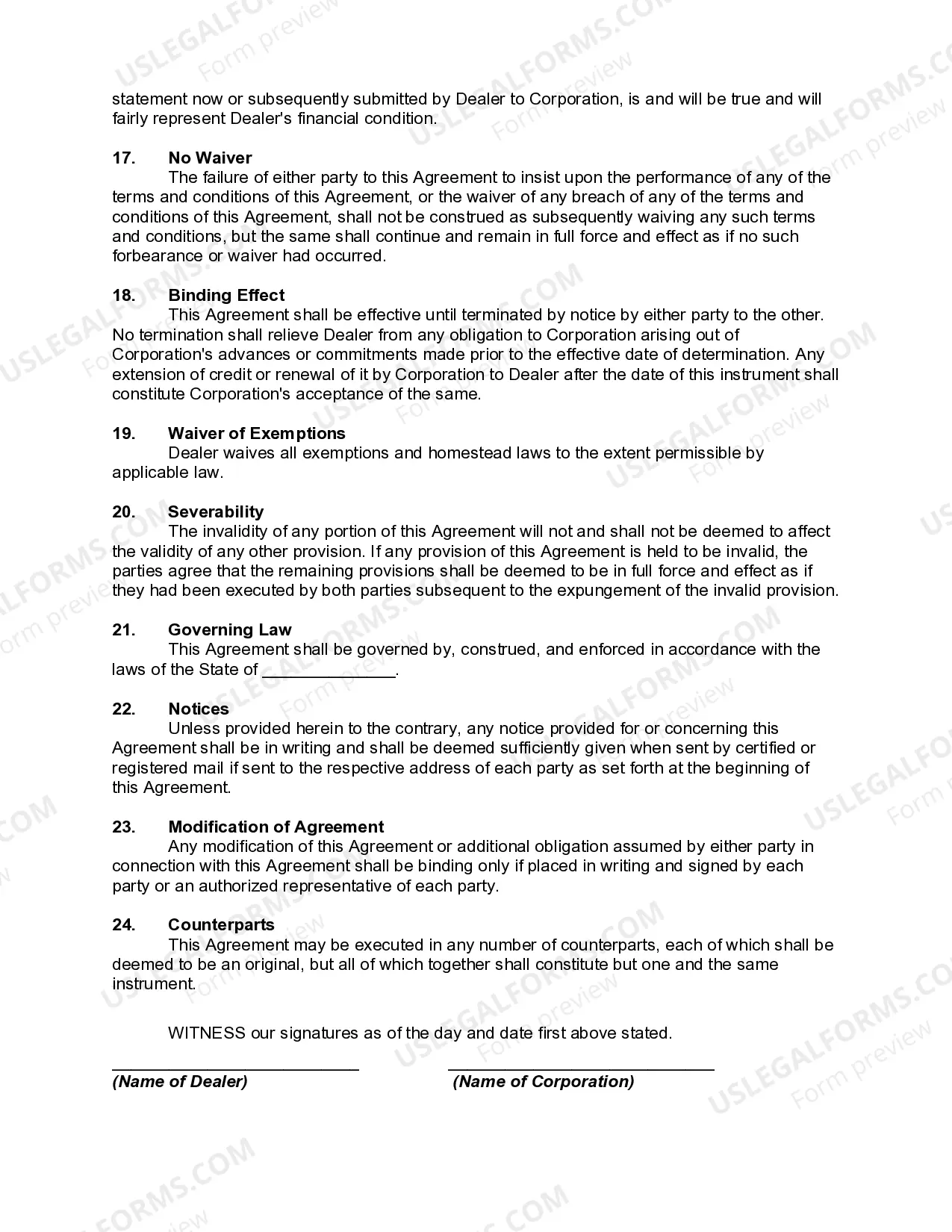

Contra Costa California Financing Agreement between Dealer and Credit Corporation for Wholesale Financing with Security interest in Accounts and General Intangibles is a legal contract that establishes the terms and conditions under which a dealer and a credit corporation engage in wholesale financing transactions. This agreement outlines the obligations, rights, and responsibilities of both parties involved in the financing arrangement. The financing agreement enables dealers to obtain financial assistance to acquire inventory or expand their wholesale business operations. By partnering with a credit corporation, dealers can access the necessary capital to purchase goods and services, which they can then sell to their customers. Under this agreement, the credit corporation provides financing to the dealer, allowing for the acquisition of various assets such as vehicles, equipment, or other merchandise. In return, the dealer pledges a security interest in their accounts and general intangibles, ensuring that the credit corporation has a legal claim over these assets if the dealer defaults on their payment obligations. The security interest granted by the dealer enhances the credit corporation's ability to recover any outstanding debts in the event of default. This provides a level of protection and reduces the credit risk faced by the financing institution. Additionally, the financing agreement defines the terms of the loan, including the principal amount, interest rates, payment frequency, repayment schedule, and any associated fees or charges. It may also specify any collateral requirements, insurance obligations, and conditions for the release of the security interest. Different types of Contra Costa California Financing Agreement between Dealer and Credit Corporation for Wholesale Financing with Security interest in Accounts and General Intangibles might include variations based on the industry or specific assets involved. For instance, there could be agreements tailored for automobile dealerships, heavy machinery dealers, or even wholesalers in the technology sector. In summary, the Contra Costa California Financing Agreement between Dealer and Credit Corporation for Wholesale Financing with Security interest in Accounts and General Intangibles serves as the legal framework that governs the financial relationship between a dealer and a credit corporation. It outlines the obligations and rights of both parties, enabling dealers to secure necessary capital for their wholesale operations while offering credit corporations protection through pledged security interests.