This form is a type of asset-financing arrangement in which a company uses its receivables (money owed by customers) as collateral in a financing agreement. The company receives an amount that is equal to a reduced value of the receivables pledged. The age of the receivables have a large effect on the amount a company will receive. The older the receivables, the less the company can expect.

This type of financing helps companies free up capital that is stuck in accounts receivables. Accounts receivable financing transfers the default risk associated with the accounts receivables to the financing company. This transfer of risk can help the company using the financing to shift focus from trying to collect receivables to current business activities.

This form is a generic example that may be referred to when preparing such a form for your particular state. It is for illustrative purposes only. Local laws should be consulted to determine any specific requirements for such a form in a particular jurisdiction.

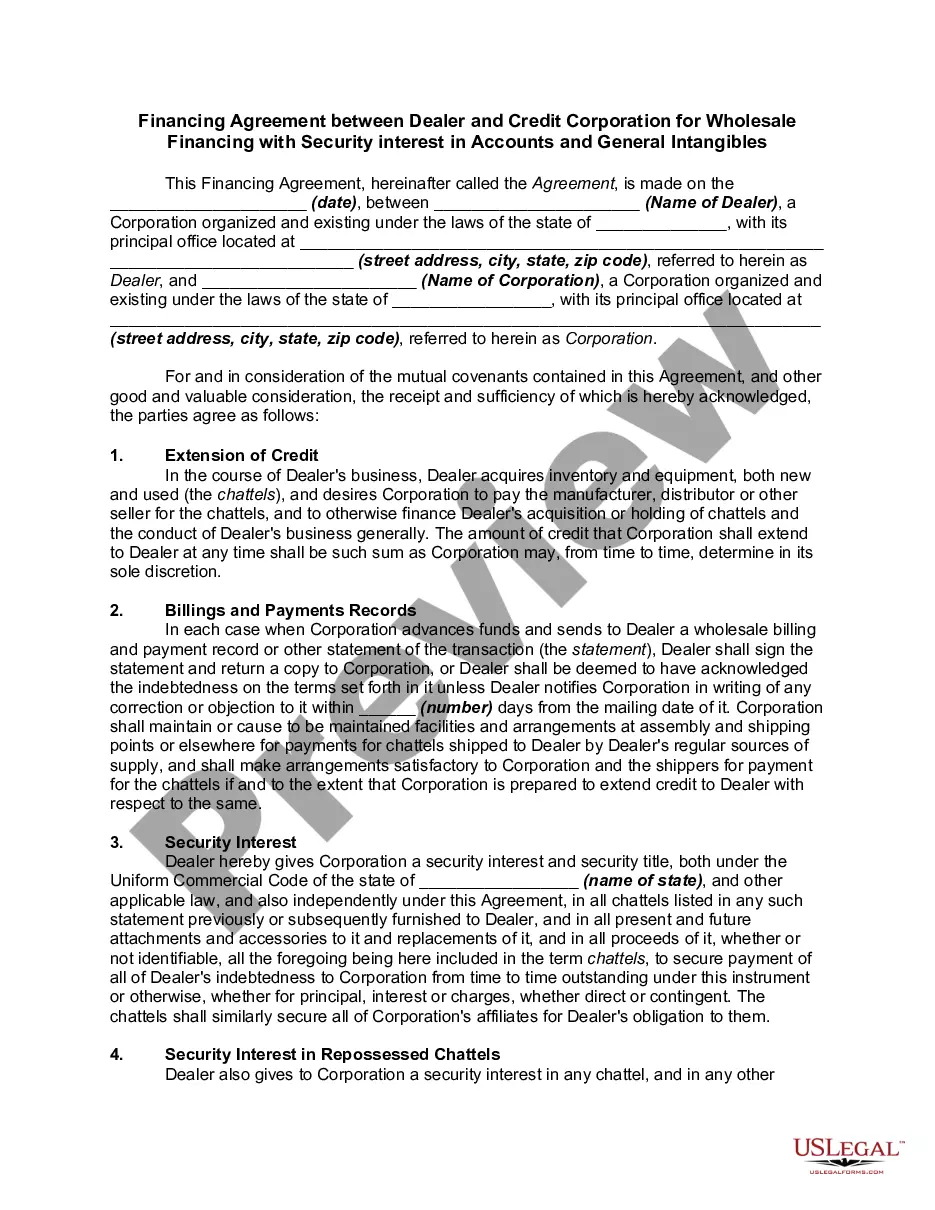

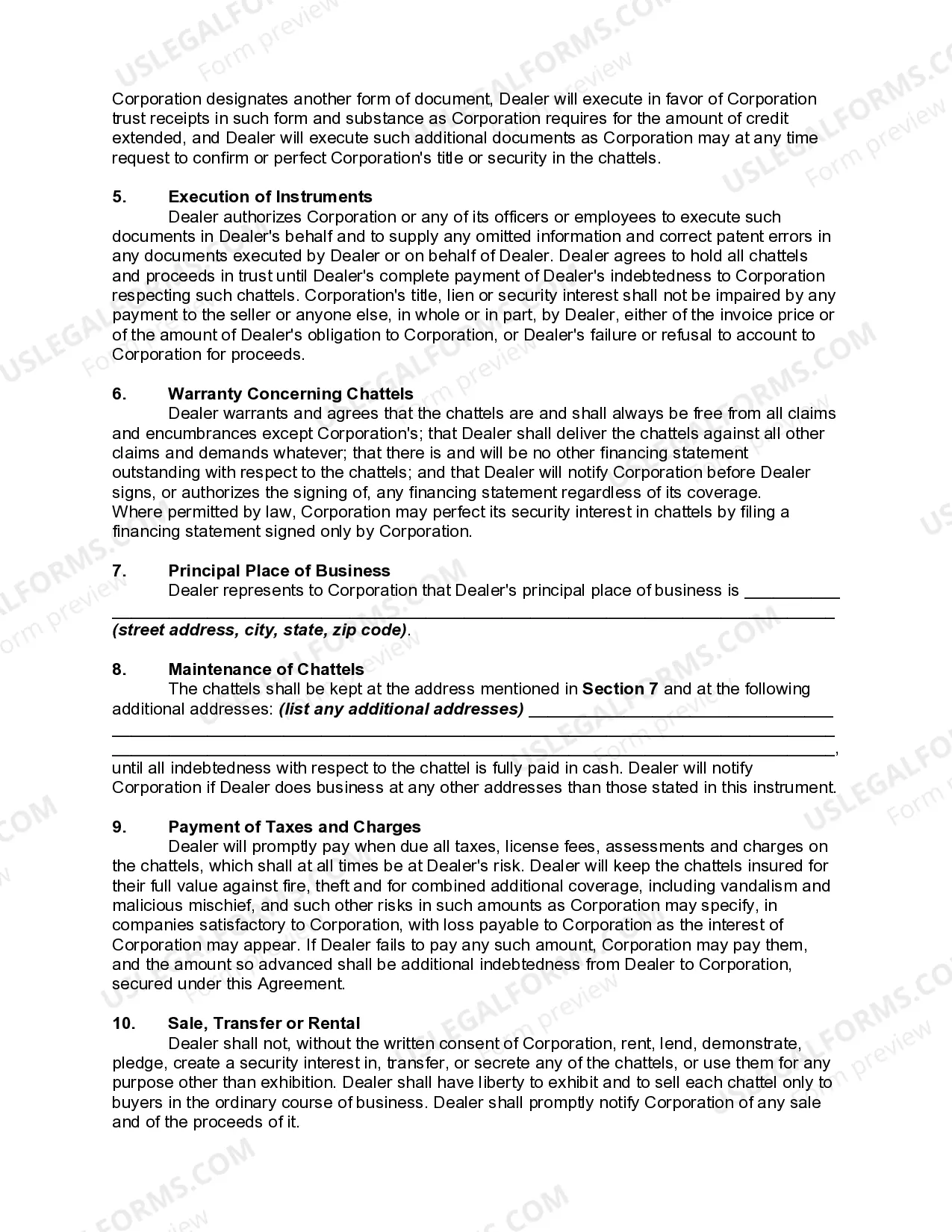

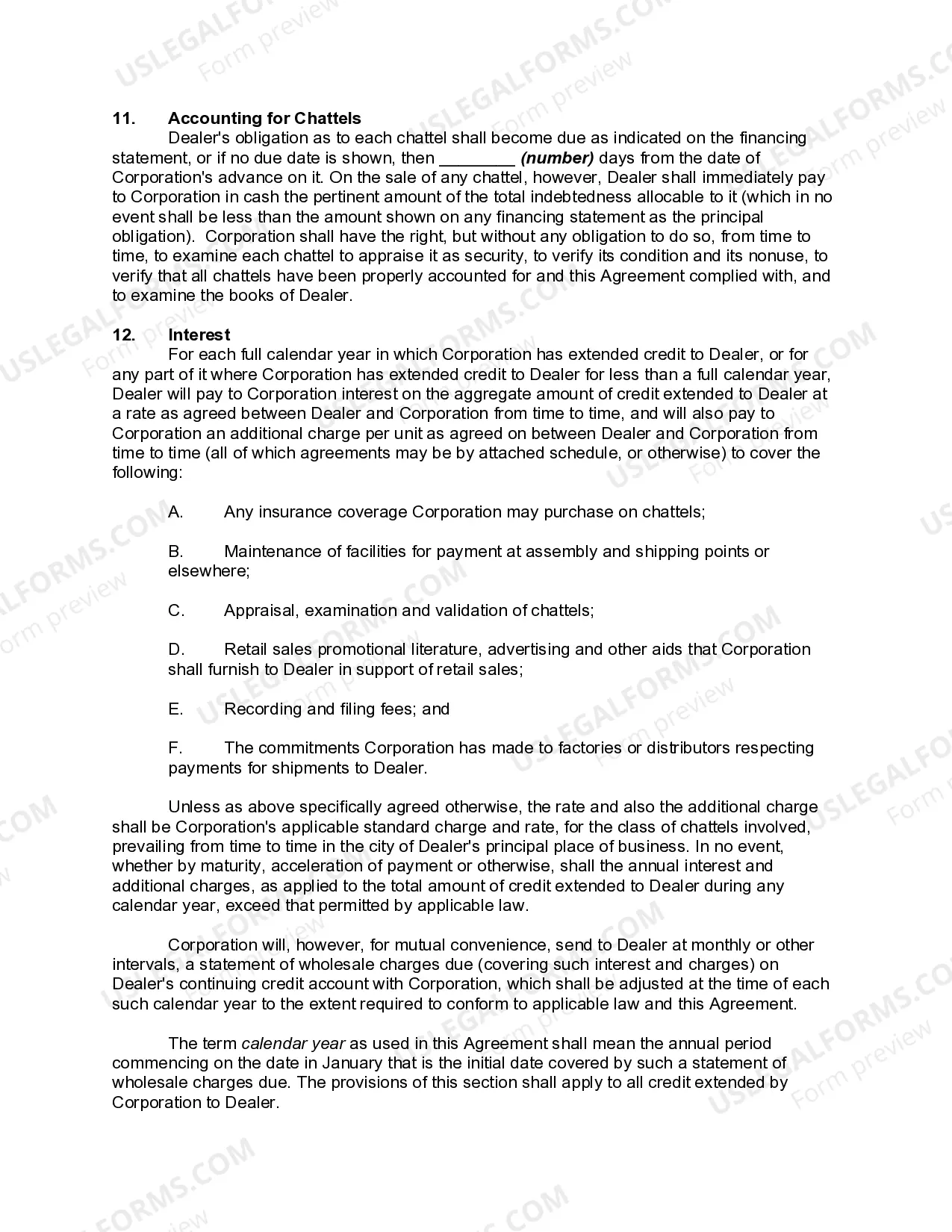

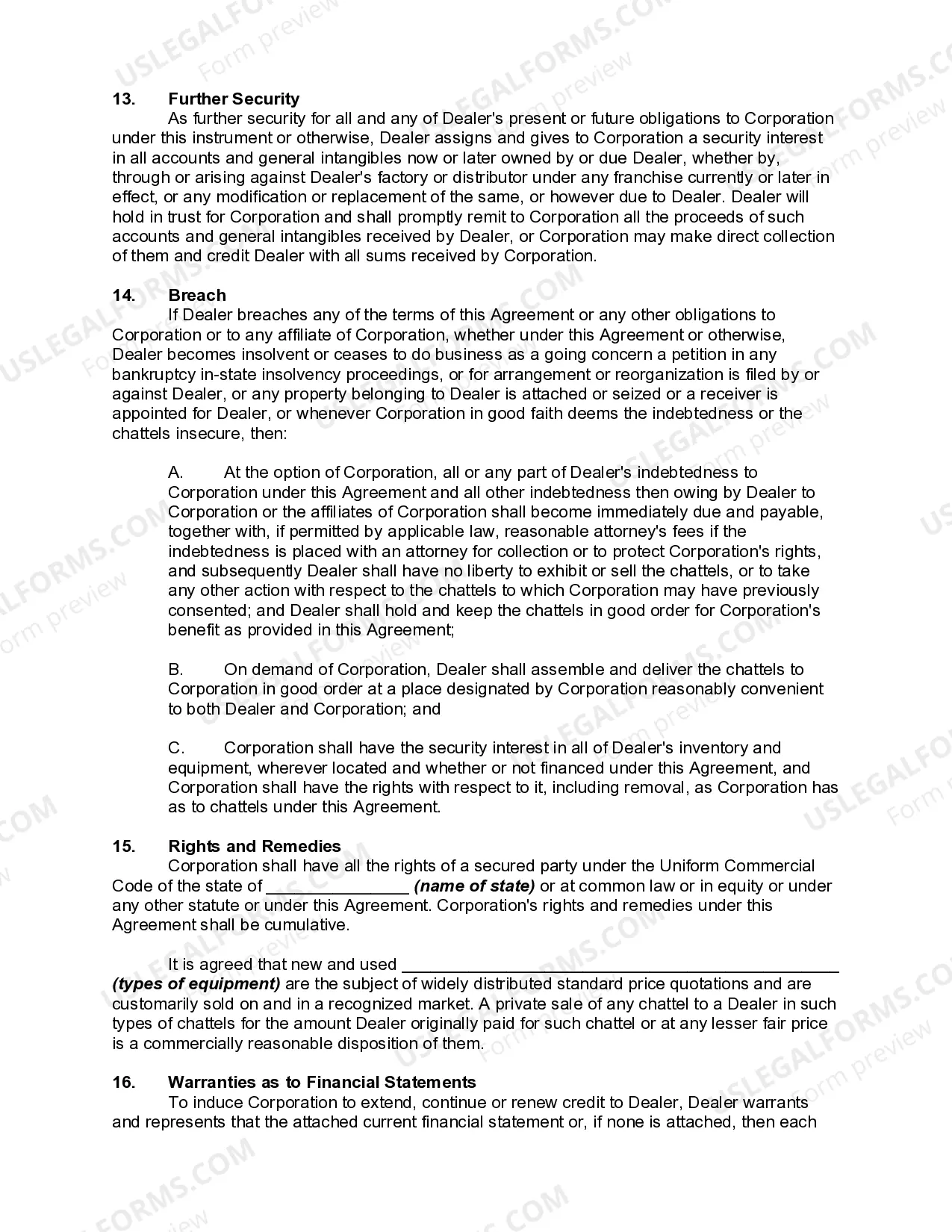

In Harris, Texas, the Financing Agreement between a Dealer and Credit Corporation for Wholesale Financing with Security interest in Accounts and General Intangibles is a crucial contract that ensures a smooth and secure financing process for dealerships. This agreement establishes a legal framework for the credit corporation to provide wholesale financing to the dealer, while simultaneously securing its interest in accounts and general intangibles. The Harris Texas Financing Agreement safeguards both parties' interests and outlines the terms and conditions agreed upon to facilitate wholesale financing. It is essential to understand that there may be variations or additional types of Harris Texas Financing Agreements between Dealers and Credit Corporations for Wholesale Financing with Security interest in Accounts and General Intangibles, based on specific business requirements and circumstances. Some notable types include: 1. Conditional Sales Financing Agreement: This agreement allows the dealer to acquire vehicles from manufacturers or suppliers using financing provided by the credit corporation. The credit corporation holds a security interest in the vehicles until the dealer repays the loan amount. 2. Floor Plan Financing Agreement: This type of agreement is commonly used in the automotive industry, enabling dealers to borrow funds from the credit corporation to purchase inventory, mainly vehicles. The credit corporation retains a security interest in the inventory until it is sold or the loan is repaid. 3. Revolving Credit Facility Agreement: Under this agreement, the dealer obtains a line of credit from the credit corporation to finance various operational expenses, such as purchasing inventory, marketing efforts, or facility maintenance. The credit corporation maintains a security interest in the dealer's accounts receivable and general intangibles. 4. Blanket or Comprehensive Lien Agreement: This agreement establishes a blanket lien on the dealer's assets, including accounts and general intangibles, as collateral for the wholesale financing. It provides the credit corporation with a security interest in all current and future assets owned by the dealer, reducing administrative burden when additional financing is required. Regardless of the specific type of Harris Texas Financing Agreement, the core elements generally include: — Identification of the dealer and credit corporation, including their legal names and addresses. — Detailed description of the financing terms, including interest rates, repayment schedules, and any associated fees or penalties. — Methodology for determining the credit limit (if applicable) and guidelines for the dealer's use of funds. — Clearly defined rights, responsibilities, and obligations for both parties, including default conditions and remedies. — Provisions for the credit corporation's security interest in the dealer's accounts, inventory, general intangibles, and other pledged assets. — Mechanisms for resolving disputes, including mediation or arbitration procedures. — Consideration of relevant federal, state, and local laws and regulations governing wholesale financing agreements in Harris Texas. In conclusion, the Harris Texas Financing Agreement between a Dealer and Credit Corporation for Wholesale Financing with Security interest in Accounts and General Intangibles acts as a vital tool for dealerships to obtain necessary funds while ensuring the credit corporation's financial interests are protected. By naming and understanding the various types, dealerships and credit corporations can select the most appropriate agreement to address their specific needs and form a mutually beneficial partnership.In Harris, Texas, the Financing Agreement between a Dealer and Credit Corporation for Wholesale Financing with Security interest in Accounts and General Intangibles is a crucial contract that ensures a smooth and secure financing process for dealerships. This agreement establishes a legal framework for the credit corporation to provide wholesale financing to the dealer, while simultaneously securing its interest in accounts and general intangibles. The Harris Texas Financing Agreement safeguards both parties' interests and outlines the terms and conditions agreed upon to facilitate wholesale financing. It is essential to understand that there may be variations or additional types of Harris Texas Financing Agreements between Dealers and Credit Corporations for Wholesale Financing with Security interest in Accounts and General Intangibles, based on specific business requirements and circumstances. Some notable types include: 1. Conditional Sales Financing Agreement: This agreement allows the dealer to acquire vehicles from manufacturers or suppliers using financing provided by the credit corporation. The credit corporation holds a security interest in the vehicles until the dealer repays the loan amount. 2. Floor Plan Financing Agreement: This type of agreement is commonly used in the automotive industry, enabling dealers to borrow funds from the credit corporation to purchase inventory, mainly vehicles. The credit corporation retains a security interest in the inventory until it is sold or the loan is repaid. 3. Revolving Credit Facility Agreement: Under this agreement, the dealer obtains a line of credit from the credit corporation to finance various operational expenses, such as purchasing inventory, marketing efforts, or facility maintenance. The credit corporation maintains a security interest in the dealer's accounts receivable and general intangibles. 4. Blanket or Comprehensive Lien Agreement: This agreement establishes a blanket lien on the dealer's assets, including accounts and general intangibles, as collateral for the wholesale financing. It provides the credit corporation with a security interest in all current and future assets owned by the dealer, reducing administrative burden when additional financing is required. Regardless of the specific type of Harris Texas Financing Agreement, the core elements generally include: — Identification of the dealer and credit corporation, including their legal names and addresses. — Detailed description of the financing terms, including interest rates, repayment schedules, and any associated fees or penalties. — Methodology for determining the credit limit (if applicable) and guidelines for the dealer's use of funds. — Clearly defined rights, responsibilities, and obligations for both parties, including default conditions and remedies. — Provisions for the credit corporation's security interest in the dealer's accounts, inventory, general intangibles, and other pledged assets. — Mechanisms for resolving disputes, including mediation or arbitration procedures. — Consideration of relevant federal, state, and local laws and regulations governing wholesale financing agreements in Harris Texas. In conclusion, the Harris Texas Financing Agreement between a Dealer and Credit Corporation for Wholesale Financing with Security interest in Accounts and General Intangibles acts as a vital tool for dealerships to obtain necessary funds while ensuring the credit corporation's financial interests are protected. By naming and understanding the various types, dealerships and credit corporations can select the most appropriate agreement to address their specific needs and form a mutually beneficial partnership.