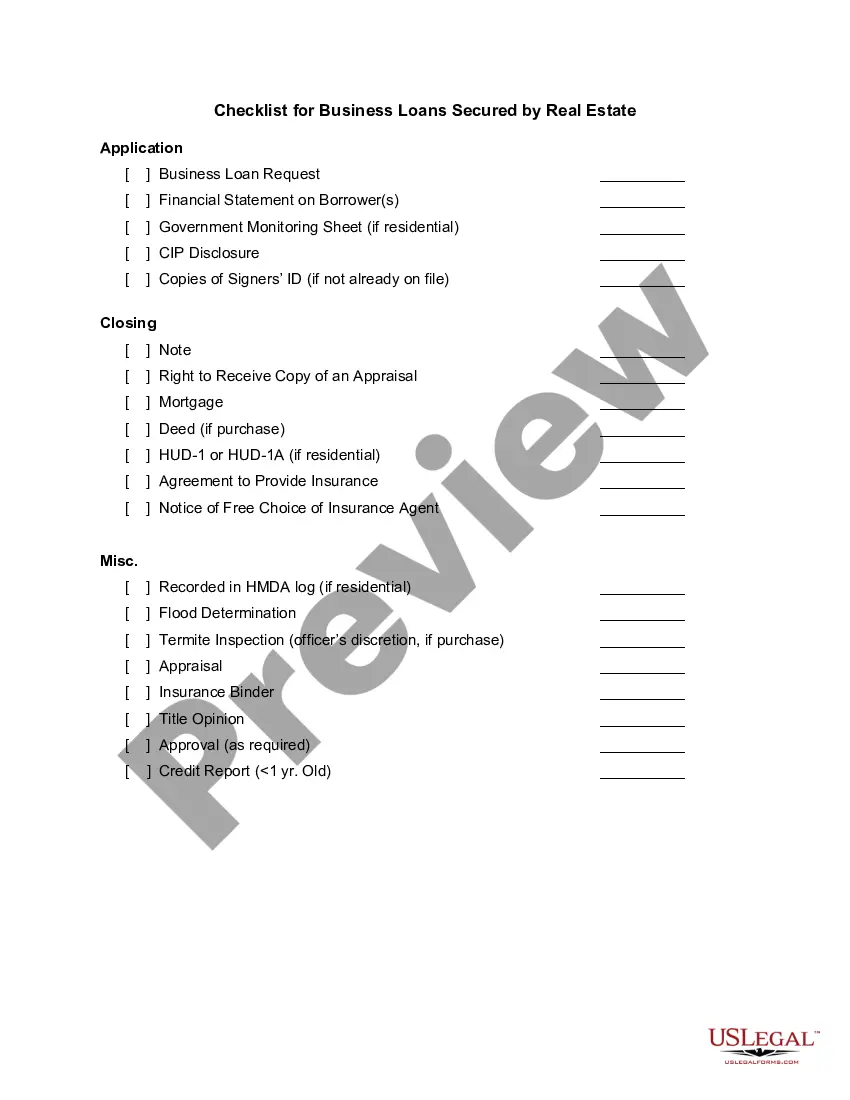

Mecklenburg North Carolina is a county located in the southwestern part of the state, with Charlotte being its largest city and county seat. For businesses looking to secure loans that are specifically backed by real estate, there are several essential items to consider on the checklist. These checklist items are aimed at assisting businesses in obtaining secured loans while minimizing risk for both the lenders and borrowers. 1. Detailed business plan: Lenders often require a comprehensive business plan outlining the company's goals, financial projections, and management structure. This plan helps lenders assess the feasibility of the loan and the potential for repayment. 2. Property documentation: Any real estate offered as collateral should have proper documentation, including ownership proof, title deeds, and parcel numbers. Additionally, property appraisals may be necessary to determine the value and ensure it aligns with the loan amount. 3. Financial records: Businesses must provide accurate financial statements, including income statements, balance sheets, and cash flow statements. These records demonstrate the company's ability to generate revenue, manage expenses, and repay the loan. 4. Personal and business credit history: Lenders thoroughly evaluate the credit history of both the business and its owners. A solid credit score increases the likelihood of loan approval and may help secure better interest rates. 5. Legal documentation: Businesses need to submit legal documents such as licenses, permits, registrations, leases, contracts, and any other relevant agreements. These documents validate the legitimacy of the business and its operations. 6. Loan purpose and repayment plan: Clearly defining the purpose of the loan, whether for expansion, equipment purchase, or debt consolidation, is crucial. Businesses must also present a solid repayment plan, including proposed terms, interest rates, and collateral valuation. 7. Insurance proof: Lenders often require adequate insurance coverage, including property insurance, liability insurance, and, if applicable, any specialized coverage required for the business's industry. Types of Mecklenburg North Carolina Checklist for Business Loans Secured by Real Estate: 1. Commercial real estate loans: These loans are specifically designed for businesses seeking financing for purchasing, refinancing, or developing commercial properties, such as office buildings, retail spaces, or industrial facilities. 2. Equipment loans: Businesses looking to secure loans for purchasing or leasing equipment can offer real estate as collateral, strengthening their loan application. 3. Construction loans: Construction companies or businesses involved in real estate development may require loans specifically for funding construction projects. These loans typically consider the future value of the real estate as collateral. 4. Business acquisition loans: When acquiring an existing business along with its real estate assets, a secured loan can be utilized to finance the purchase. The real estate serves as collateral, providing security to lenders. By following a comprehensive checklist and considering the different types of secured loans, businesses in Mecklenburg North Carolina can increase their chances of obtaining the necessary financing for growth, expansion, or various operational needs, while leveraging the value of their real estate assets.

Mecklenburg North Carolina Checklist for Business Loans Secured by Real Estate

Description

How to fill out Mecklenburg North Carolina Checklist For Business Loans Secured By Real Estate?

Are you looking to quickly create a legally-binding Mecklenburg Checklist for Business Loans Secured by Real Estate or maybe any other form to manage your own or corporate affairs? You can go with two options: hire a legal advisor to draft a legal document for you or draft it entirely on your own. Luckily, there's a third solution - US Legal Forms. It will help you get professionally written legal paperwork without paying sky-high prices for legal services.

US Legal Forms provides a rich collection of over 85,000 state-specific form templates, including Mecklenburg Checklist for Business Loans Secured by Real Estate and form packages. We provide documents for a myriad of use cases: from divorce papers to real estate document templates. We've been on the market for more than 25 years and gained a rock-solid reputation among our customers. Here's how you can become one of them and get the necessary template without extra hassles.

- First and foremost, carefully verify if the Mecklenburg Checklist for Business Loans Secured by Real Estate is adapted to your state's or county's regulations.

- In case the document has a desciption, make sure to check what it's intended for.

- Start the searching process over if the form isn’t what you were looking for by utilizing the search box in the header.

- Select the plan that best suits your needs and move forward to the payment.

- Choose the format you would like to get your document in and download it.

- Print it out, complete it, and sign on the dotted line.

If you've already registered an account, you can simply log in to it, find the Mecklenburg Checklist for Business Loans Secured by Real Estate template, and download it. To re-download the form, simply go to the My Forms tab.

It's effortless to buy and download legal forms if you use our catalog. Additionally, the paperwork we provide are updated by law professionals, which gives you greater confidence when dealing with legal matters. Try US Legal Forms now and see for yourself!