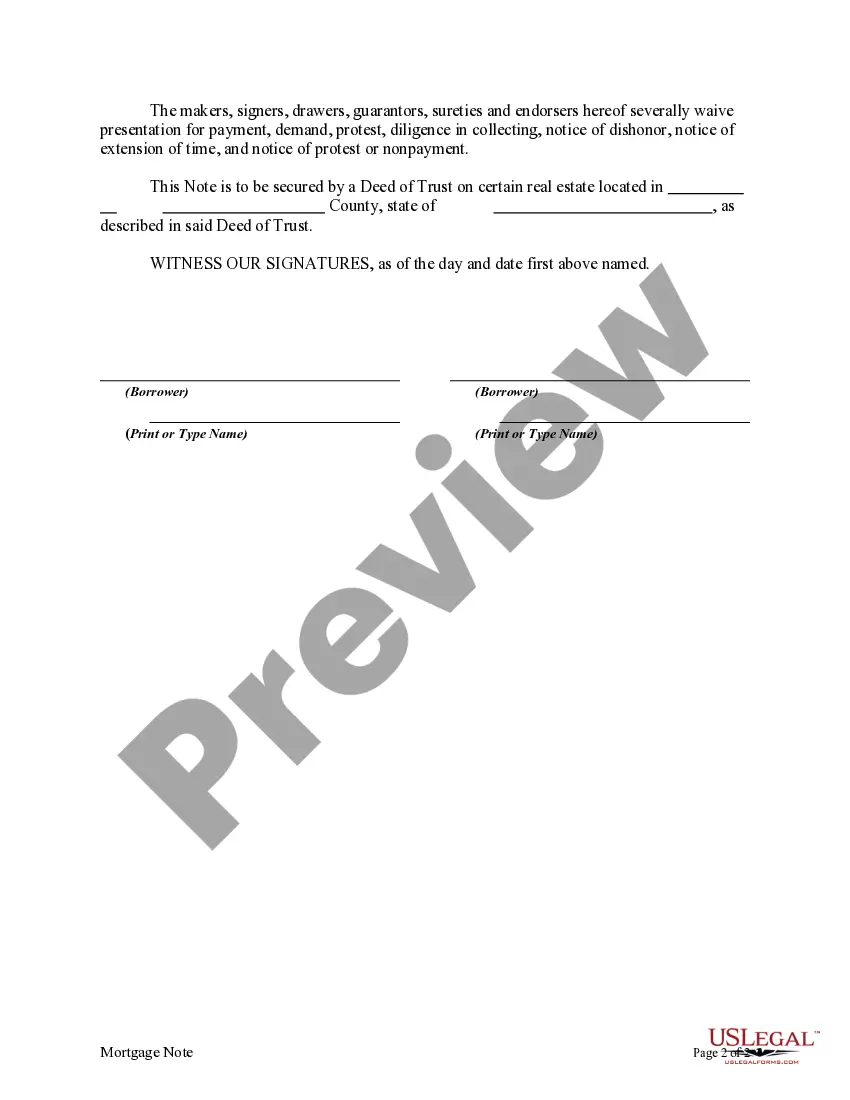

A Riverside California Mortgage Note is a legal document that outlines the terms and conditions of a mortgage loan in Riverside, California. It acts as evidence of the loan agreement between the borrower and the lender, emphasizing the borrower's promise to repay the loan amount along with any applicable interest. There are different types of Riverside California Mortgage Notes, including: 1. Fixed-Rate Mortgage Note: This type of note specifies a fixed interest rate that remains constant throughout the loan term. It provides stability to borrowers as they know exactly how much their monthly payments will be. 2. Adjustable-Rate Mortgage Note: Unlike a fixed-rate mortgage note, an adjustable-rate mortgage note entitles the lender to adjust the interest rate periodically based on market conditions. This type of note allows for potential fluctuations in interest rates and can result in increased or decreased monthly payments. 3. Balloon Mortgage Note: A balloon mortgage note offers lower monthly payments initially, but after a predetermined period, a lump-sum payment, known as a balloon payment, is due. This type of note may be suitable for borrowers who plan to refinance or sell the property before the balloon payment becomes due. 4. Interest-Only Mortgage Note: An interest-only mortgage note allows borrowers to make payments on only the accrued interest for a specified period, typically five to ten years. Afterward, the borrower is required to pay both the principal and interest. This note type provides flexibility in the early stages of homeownership. 5. Reverse Mortgage Note: The reverse mortgage note is designed for senior homeowners aged 62 or older to convert a portion of the equity in their homes into cash. Unlike traditional mortgage notes, the lender makes payments to the borrower in the form of a loan against the home equity. Repayment typically occurs when the homeowner sells the property or passes away. Having a clear understanding of the type of Riverside California Mortgage Note you have is crucial for both the borrower and the lender. It ensures that all terms and conditions associated with the loan are spelled out, including repayment schedule, interest rates, penalties for defaulting, and any applicable fees.

Riverside California Mortgage Note

Description

How to fill out Riverside California Mortgage Note?

Laws and regulations in every area differ around the country. If you're not a lawyer, it's easy to get lost in countless norms when it comes to drafting legal documents. To avoid pricey legal assistance when preparing the Riverside Mortgage Note, you need a verified template legitimate for your region. That's when using the US Legal Forms platform is so advantageous.

US Legal Forms is a trusted by millions online catalog of more than 85,000 state-specific legal templates. It's an excellent solution for professionals and individuals searching for do-it-yourself templates for various life and business occasions. All the documents can be used many times: once you purchase a sample, it remains available in your profile for future use. Therefore, when you have an account with a valid subscription, you can simply log in and re-download the Riverside Mortgage Note from the My Forms tab.

For new users, it's necessary to make several more steps to obtain the Riverside Mortgage Note:

- Examine the page content to make sure you found the right sample.

- Take advantage of the Preview option or read the form description if available.

- Look for another doc if there are inconsistencies with any of your criteria.

- Click on the Buy Now button to obtain the template when you find the proper one.

- Opt for one of the subscription plans and log in or sign up for an account.

- Choose how you prefer to pay for your subscription (with a credit card or PayPal).

- Pick the format you want to save the document in and click Download.

- Fill out and sign the template in writing after printing it or do it all electronically.

That's the simplest and most affordable way to get up-to-date templates for any legal reasons. Find them all in clicks and keep your documentation in order with the US Legal Forms!