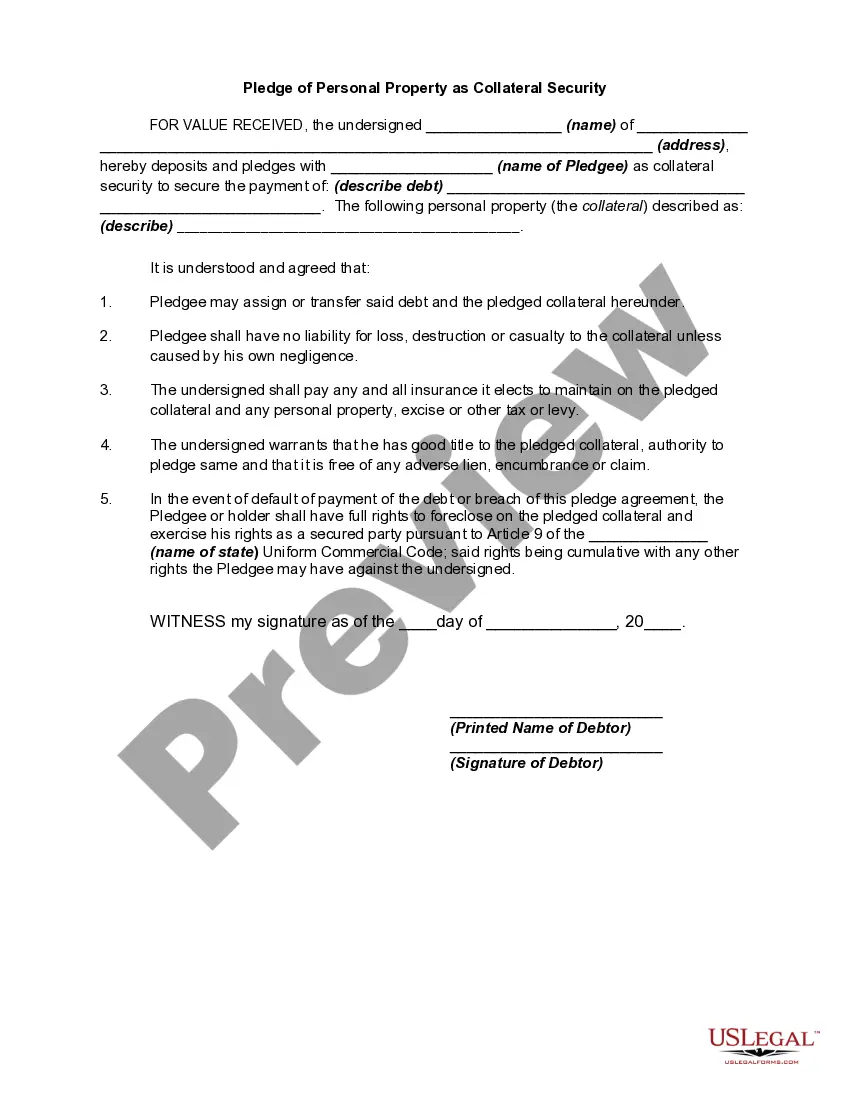

Fulton Georgia Pledge of Personal Property as Collateral Security is a legal arrangement wherein a borrower pledges their personal property as collateral to secure a loan or debt. It serves as a guarantee for the lender that if the borrower fails to repay the loan, the lender can seize and sell the pledged property to recover their losses. This collateral security instrument is commonly used in Fulton County, Georgia, and plays a vital role in protecting the interests of lenders and borrowers. There are different types of Fulton Georgia Pledge of Personal Property as Collateral Security, each having varying characteristics and applications. These types include: 1. Chattel Mortgage: A Chattel Mortgage is a type of pledge where personal property, such as vehicles, equipment, or machinery, is used as collateral for a loan. The borrower retains possession of the pledged property but grants the lender a security interest. 2. Security Agreement: A Security Agreement is a comprehensive contract that encompasses the pledge of various personal property items as collateral. It can include assets like inventory, accounts receivable, equipment, or intellectual property. This type of pledge provides lenders with a wider range of collateral options. 3. UCC-1 Financing Statement: Under the Uniform Commercial Code (UCC), a UCC-1 Financing Statement is filed to publicly record a pledge of collateral for a loan. It serves as notice to potential creditors that the pledged property has a prior security interest attached to it. This type of pledge can cover a broad range of personal property assets. 4. Promissory Note with Collateral Clause: This is a legally binding document that includes a pledge of personal property as collateral. The borrower agrees to repay the loan according to specific terms and conditions, and in case of default, the lender can exercise their rights over the pledged property. The Fulton Georgia Pledge of Personal Property as Collateral Security is a crucial mechanism that ensures the financial stability and credibility of borrowers while granting lenders a level of assurance in their lending practices. It provides a mutually beneficial arrangement that facilitates loan approvals and aids in reducing lending risks.

Fulton Georgia Pledge of Personal Property as Collateral Security

Description

How to fill out Fulton Georgia Pledge Of Personal Property As Collateral Security?

Laws and regulations in every sphere vary around the country. If you're not an attorney, it's easy to get lost in various norms when it comes to drafting legal documentation. To avoid pricey legal assistance when preparing the Fulton Pledge of Personal Property as Collateral Security, you need a verified template valid for your region. That's when using the US Legal Forms platform is so advantageous.

US Legal Forms is a trusted by millions web catalog of more than 85,000 state-specific legal templates. It's a great solution for specialists and individuals searching for do-it-yourself templates for various life and business scenarios. All the documents can be used multiple times: once you obtain a sample, it remains available in your profile for future use. Thus, when you have an account with a valid subscription, you can just log in and re-download the Fulton Pledge of Personal Property as Collateral Security from the My Forms tab.

For new users, it's necessary to make several more steps to obtain the Fulton Pledge of Personal Property as Collateral Security:

- Examine the page content to ensure you found the appropriate sample.

- Utilize the Preview option or read the form description if available.

- Look for another doc if there are inconsistencies with any of your requirements.

- Utilize the Buy Now button to get the document when you find the proper one.

- Opt for one of the subscription plans and log in or create an account.

- Decide how you prefer to pay for your subscription (with a credit card or PayPal).

- Pick the format you want to save the file in and click Download.

- Fill out and sign the document on paper after printing it or do it all electronically.

That's the simplest and most cost-effective way to get up-to-date templates for any legal reasons. Find them all in clicks and keep your paperwork in order with the US Legal Forms!