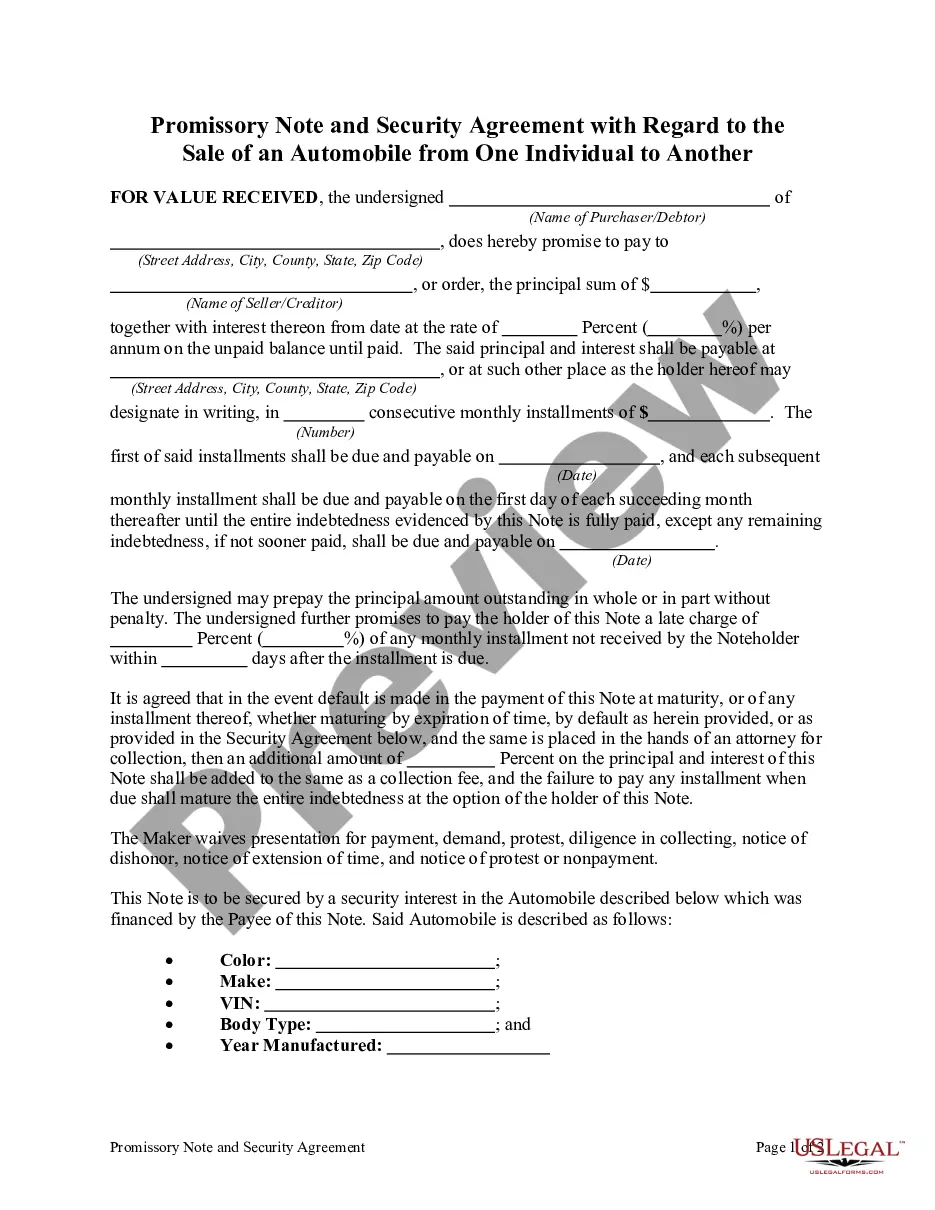

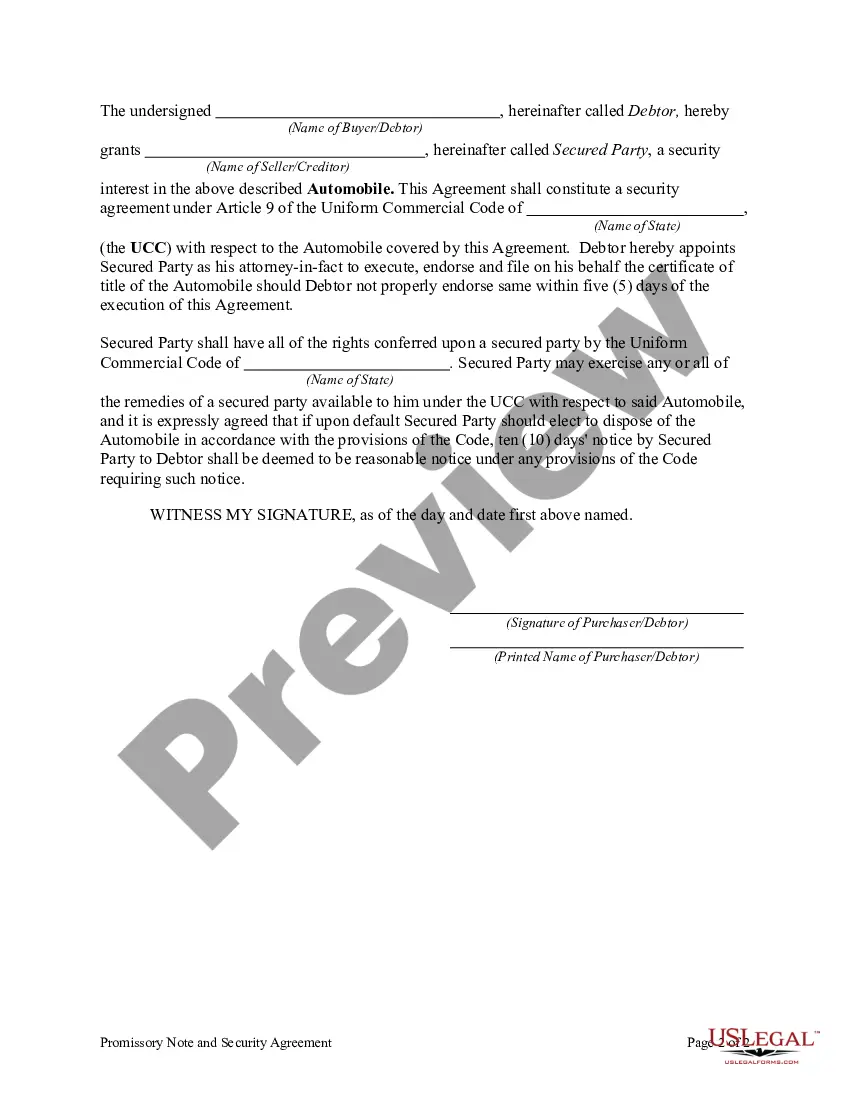

A Fairfax Virginia Promissory Note and Security Agreement with regard to the sale of an automobile from one individual to another is a legal document that outlines the terms and conditions of a transaction involving the purchase and financing of a vehicle. This agreement serves as a binding contract between the buyer and the seller, ensuring that both parties are protected and their rights and responsibilities are clearly defined. The promissory note component of the agreement establishes the buyer's commitment to repay the seller for the agreed-upon purchase price of the vehicle. It includes details such as the total amount owed, interest rate (if applicable), payment schedule, and any penalties for late payments or default. The note is essential for documenting the buyer's promise to repay the seller over a specified period. In addition to the promissory note, the Security Agreement is another important aspect of this transaction. It provides security to the seller by granting a security interest in the vehicle being sold. This means that until the buyer fully repays the amount owed as per the promissory note, the seller holds a legal interest or lien on the vehicle. If the buyer fails to fulfill their financial obligations, the seller has the right to repossess the vehicle. There may be different types of Fairfax Virginia Promissory Note and Security Agreements based on the specific circumstances of the sale or financing arrangement. Here are a few potential variations: 1. Installment Sales Agreement: This type of agreement allows the buyer to make payments in regular installments over a specified period rather than paying the full amount upfront. It outlines the terms of the installments, including payment amount, due dates, and interest rate (if applicable). 2. Balloon Payment Agreement: In this agreement, the buyer makes lower monthly payments throughout the loan term but completes the repayment with a larger "balloon" payment at the end. This type of agreement may be suitable for buyers with a cash flow preference or expecting a lump sum payment in the future. 3. Lease Agreement with Option to Purchase: This agreement combines elements of a lease and a sale. The buyer initially enters into a lease agreement, paying monthly lease payments. However, they also have the option to purchase the vehicle at the end of the lease term for a predetermined price. 4. Subordination Agreement: Sometimes, there may be an existing lien or security interest on the vehicle (for example, an outstanding auto loan). A subordination agreement allows the seller's security interest to be prioritized over the existing one in case of default or repossession. It is important for both the buyer and the seller to carefully review and understand the terms stated in the Fairfax Virginia Promissory Note and Security Agreement before signing. Seeking legal advice or consulting an attorney with experience in these matters can ensure that the agreement is fair and legally binding for both parties involved.

Fairfax Virginia Promissory Note and Security Agreement with Regard to the Sale of an Automobile from One Individual to Another

Description

How to fill out Fairfax Virginia Promissory Note And Security Agreement With Regard To The Sale Of An Automobile From One Individual To Another?

If you need to get a trustworthy legal form supplier to get the Fairfax Promissory Note and Security Agreement with Regard to the Sale of an Automobile from One Individual to Another, look no further than US Legal Forms. Whether you need to launch your LLC business or manage your belongings distribution, we got you covered. You don't need to be well-versed in in law to find and download the appropriate template.

- You can search from more than 85,000 forms arranged by state/county and case.

- The self-explanatory interface, number of learning materials, and dedicated support team make it easy to get and complete various documents.

- US Legal Forms is a trusted service offering legal forms to millions of users since 1997.

Simply type to search or browse Fairfax Promissory Note and Security Agreement with Regard to the Sale of an Automobile from One Individual to Another, either by a keyword or by the state/county the document is intended for. After locating necessary template, you can log in and download it or retain it in the My Forms tab.

Don't have an account? It's effortless to get started! Simply locate the Fairfax Promissory Note and Security Agreement with Regard to the Sale of an Automobile from One Individual to Another template and check the form's preview and description (if available). If you're confident about the template’s terminology, go ahead and hit Buy now. Register an account and choose a subscription plan. The template will be instantly ready for download once the payment is completed. Now you can complete the form.

Taking care of your law-related affairs doesn’t have to be expensive or time-consuming. US Legal Forms is here to demonstrate it. Our extensive variety of legal forms makes these tasks less expensive and more reasonably priced. Set up your first business, organize your advance care planning, create a real estate agreement, or execute the Fairfax Promissory Note and Security Agreement with Regard to the Sale of an Automobile from One Individual to Another - all from the comfort of your home.

Join US Legal Forms now!