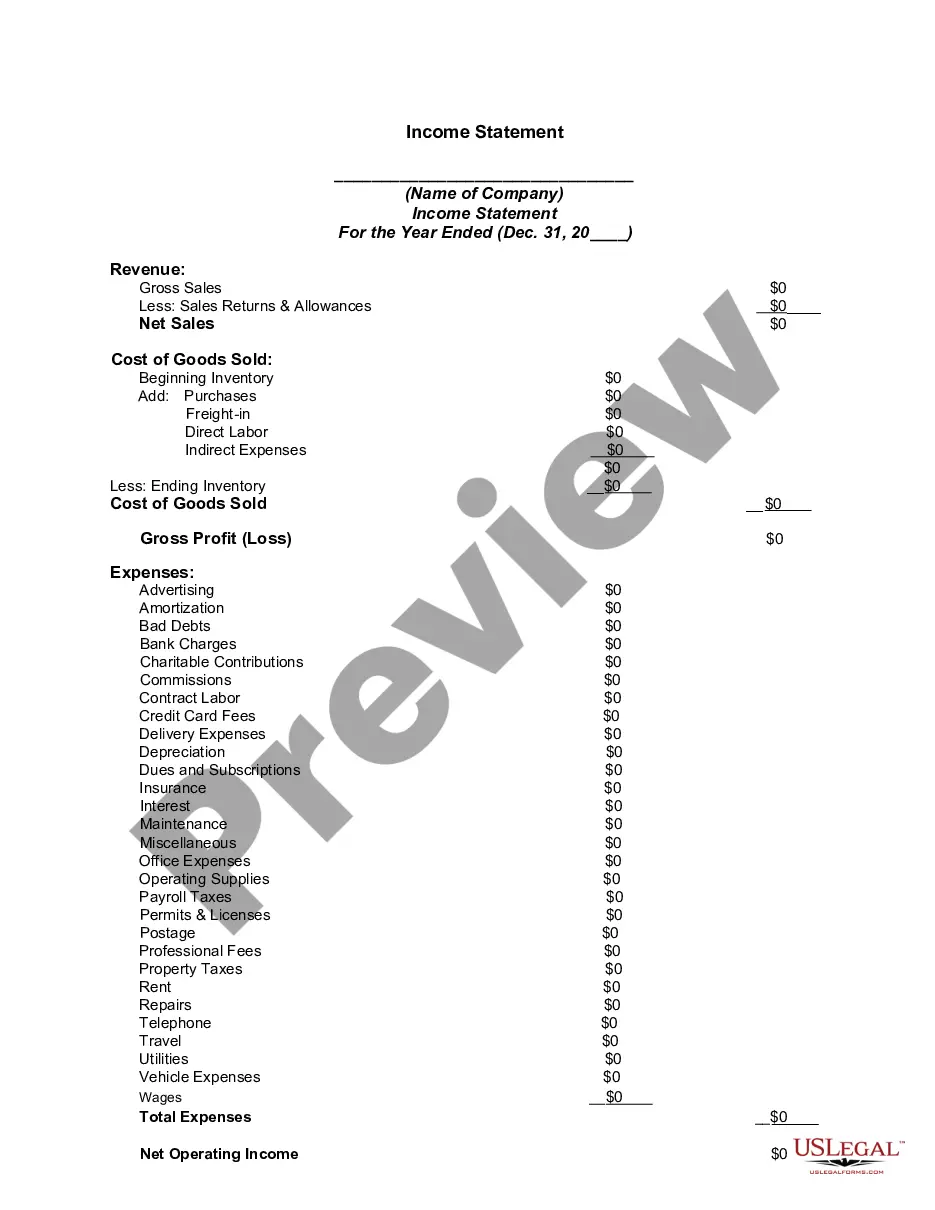

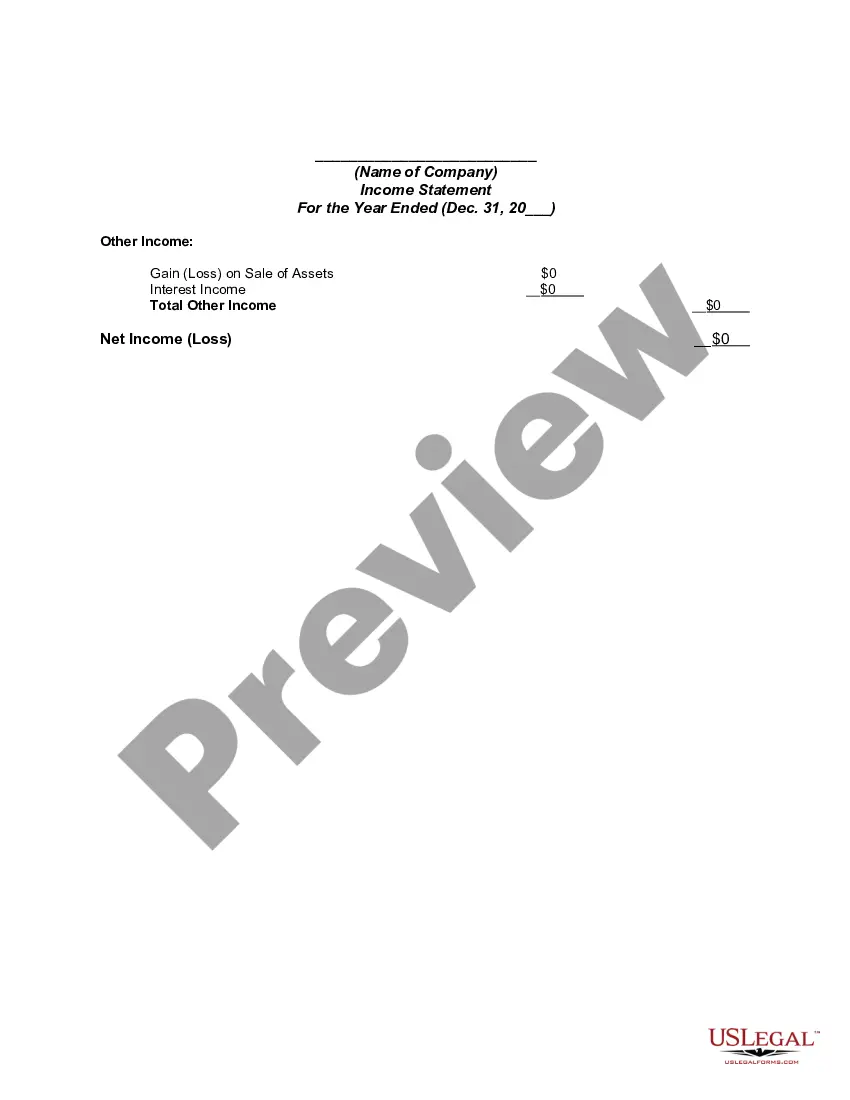

An income statement (sometimes called a profit and loss statement) lists your revenues and expenses, and tells you the profit or loss of your business for a given period of time. You can use this income statement form as a starting point to create one yourself.

The Franklin Ohio Income Statement provides a comprehensive financial overview of the income and expenses of businesses or individuals in the city of Franklin, Ohio. This document plays a crucial role in understanding a company's financial performance and helps make informed decisions regarding investments, taxation, and future planning. The Franklin Ohio Income Statement consists of various sections, each focusing on specific aspects of the financial operations. The main components commonly found in this financial statement include revenue, cost of goods sold, gross profit, operating expenses, non-operating income/expenses, and net income. 1. Revenue: This section details the total income generated by a business during a specific period, primarily from the sale of goods or services. It encompasses various revenue sources, such as product sales, service fees, rental income, and others. 2. Cost of Goods Sold: This section accounts for the direct costs associated with producing or acquiring the goods or services that generated the revenue. It includes expenses like material costs, direct labor, manufacturing overhead, and inventory adjustments. 3. Gross Profit: Gross profit refers to the difference between revenue and the cost of goods sold. It represents the profitability of a company's core operations before considering other expenses. 4. Operating Expenses: This section encompasses the day-to-day expenses incurred in running a business. It includes expenses like employee salaries, rent/utilities, marketing/advertising costs, insurance, administrative overhead, and depreciation. Operating expenses are deducted from the gross profit to calculate operating income. 5. Non-Operating Income/Expenses: Non-operating income/expenses are revenue or expenses that are not directly related to core business operations. Examples can include interest income, gains/losses from investments or property sales, and other non-core activities of the business. 6. Net Income: Net income is the final figure on the income statement and represents the profit earned after deducting all expenses, both operating and non-operating, from the gross profit. It reflects the overall profitability and financial performance of the business for the given period. It is important to note that while the structure of the income statement remains consistent, the terminology may vary depending on the jurisdiction or industry. For example, some variations may include terms like operating profit, earnings before interest and taxes (EBIT), or earnings before interest, taxes, depreciation, and amortization (EBITDA). In summary, the Franklin Ohio Income Statement provides a detailed breakdown of the financial performance of businesses or individuals in Franklin, Ohio. By examining revenue, expenses, gross profit, operating income, and net income, it offers valuable insights into the financial health and profitability of entities operating within the city.The Franklin Ohio Income Statement provides a comprehensive financial overview of the income and expenses of businesses or individuals in the city of Franklin, Ohio. This document plays a crucial role in understanding a company's financial performance and helps make informed decisions regarding investments, taxation, and future planning. The Franklin Ohio Income Statement consists of various sections, each focusing on specific aspects of the financial operations. The main components commonly found in this financial statement include revenue, cost of goods sold, gross profit, operating expenses, non-operating income/expenses, and net income. 1. Revenue: This section details the total income generated by a business during a specific period, primarily from the sale of goods or services. It encompasses various revenue sources, such as product sales, service fees, rental income, and others. 2. Cost of Goods Sold: This section accounts for the direct costs associated with producing or acquiring the goods or services that generated the revenue. It includes expenses like material costs, direct labor, manufacturing overhead, and inventory adjustments. 3. Gross Profit: Gross profit refers to the difference between revenue and the cost of goods sold. It represents the profitability of a company's core operations before considering other expenses. 4. Operating Expenses: This section encompasses the day-to-day expenses incurred in running a business. It includes expenses like employee salaries, rent/utilities, marketing/advertising costs, insurance, administrative overhead, and depreciation. Operating expenses are deducted from the gross profit to calculate operating income. 5. Non-Operating Income/Expenses: Non-operating income/expenses are revenue or expenses that are not directly related to core business operations. Examples can include interest income, gains/losses from investments or property sales, and other non-core activities of the business. 6. Net Income: Net income is the final figure on the income statement and represents the profit earned after deducting all expenses, both operating and non-operating, from the gross profit. It reflects the overall profitability and financial performance of the business for the given period. It is important to note that while the structure of the income statement remains consistent, the terminology may vary depending on the jurisdiction or industry. For example, some variations may include terms like operating profit, earnings before interest and taxes (EBIT), or earnings before interest, taxes, depreciation, and amortization (EBITDA). In summary, the Franklin Ohio Income Statement provides a detailed breakdown of the financial performance of businesses or individuals in Franklin, Ohio. By examining revenue, expenses, gross profit, operating income, and net income, it offers valuable insights into the financial health and profitability of entities operating within the city.